Asset Sales and Strategic Uncertainty Define Seritage's Current Trajectory

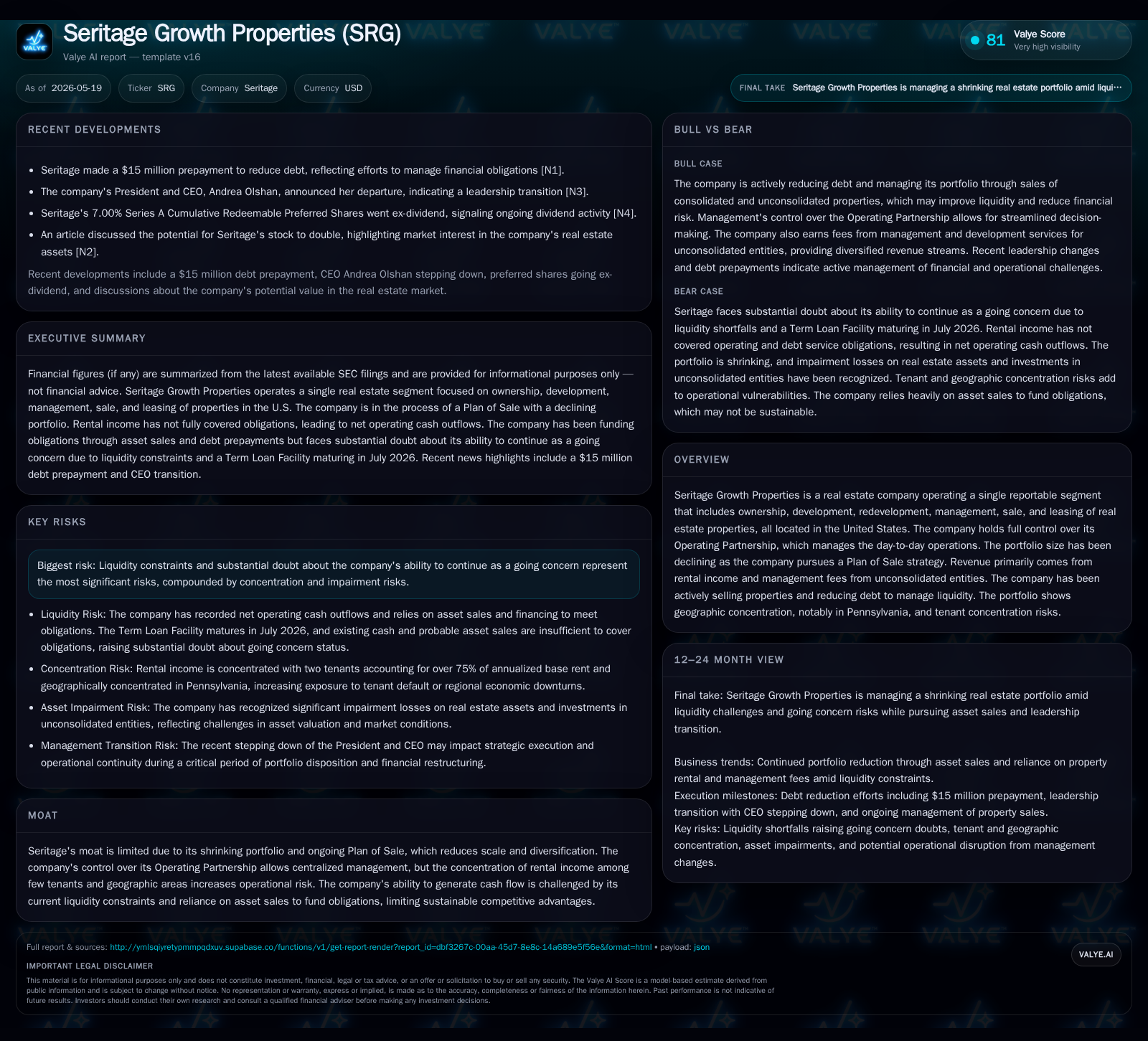

Seritage Growth Properties continues shrinking its portfolio under a Plan of Sale while confronting acute liquidity risks and strategic ambiguity.

In its latest quarterly filing, Seritage Growth Properties reported ongoing operating cash flow deficits and no scheduled paydowns on its near-term debt, underscoring pressing liquidity challenges ahead of a July 2026 Term Loan maturity. The company pursues a Plan of Sale strategy, steadily divesting consolidated and unconsolidated properties to raise capital, though its diminishing portfolio heightens concentration risks and reduces operational scale. Its business model relies primarily on rental income and management fees from its real estate holdings in the United States, notably concentrated in Pennsylvania. Strategic alternatives remain under review by the Board amid significant going concern doubts tied to funding obligations beyond asset liquidation proceeds. Key near-term indicators include successful asset dispositions to improve liquidity and progress on alternative financing or transaction pathways.

Recent Quarterly Operating Update: Critical Liquidity Snapshot

Seritage Growth Properties’ latest 10-Q filing for Q1 2026 reveals continuing operating cash flow deficits, with net operating cash outflows of $5.7 million for the quarter [S2]. Though modest investing cash inflows of $3.4 million arose primarily from distributions related to unconsolidated entities, these were offset by ongoing development expenditures and investments in those entities. Notably, no scheduled principal payments were made on the Term Loan Facility during this period.

The company’s Term Loan Facility, extended to mature on July 31, 2026 after multiple amendments with Berkshire Hathaway as lender and administrative agent [S6], still carries an unpaid principal balance of $50 million as of March 31, 2026 [S2]. Critically, Seritage reports that the proceeds expected from assets under contract—$11 million from a consolidated property—combined with existing cash on hand ($44.5 million as of March 31, 2026) will not suffice to meet its Obligations including debt maturity payments [S2][S8]. No additional assets had contracts deemed probable at quarter-end.

Management acknowledges substantial doubt remains about Seritage's ability to continue as a going concern given this imbalance between near-term liabilities and liquidity resources [S2]. The company continues to rely heavily on sales of both consolidated and unconsolidated properties alongside efforts to secure alternative financing arrangements to fund its obligations through maturity and beyond.

Business Model and Revenue Drivers Amid Portfolio Decline

Seritage operates a single reportable segment encompassing ownership, development, redevelopment, management, sale, and leasing activities of real estate properties exclusively in the U.S. [S1][S16]. The company’s revenue stream mainly arises from contractual rents paid by tenants renting retail or mixed-use spaces within its holdings and fees generated through managing unconsolidated joint ventures.

The portfolio has contracted substantially due to the approved Plan of Sale strategy initiated since early 2022 aimed at liquidating assets to maximize shareholder value [S1]. As of end-2025, it consisted of about ten properties totaling approximately 0.8 million square feet (gross leasable/build-to-suit area) spread over roughly 156 acres [S1]. This includes five consolidated properties (about 0.3 million sq ft and 71 acres) plus five unconsolidated joint venture interests (about 0.5 million sq ft and 85 acres). The geographic exposure is notably concentrated in Pennsylvania alongside limited tenant bases.

Tenant lease agreements drive rental income volume; however, significant concentration elevates operational risk should key tenants vacate or renegotiate terms unfavorably. With portfolio downsizing ongoing via asset sales—five consolidated properties were sold in calendar year 2025 alone generating gross proceeds exceeding $220 million—the base for recurring rental income shrinks commensurately [S1]. Thus revenue volumes trend downward structurally over time absent new developments or acquisitions.

Industry Positioning and Competitive Dynamics of a Shrinking Asset Base

Within the broader U.S. real estate sector—particularly retail-focused REITs or growth property firms specializing in redevelopments—scale provides negotiating leverage over tenants and service providers as well as economies in operations such as centralized property management through an Operating Partnership arrangement [S12]. Seritage retains full control over its Operating Partnership which administers daily operations across its portfolio [S12], facilitating operational consistency despite asset dispersion.

However, shrinking portfolio size undermines differential advantages tied to scale; reduced diversification heightens revenue volatility due to dependency on fewer tenants and geographies while simultaneously limiting bargaining power for leasing renewals or expansions. Unlike larger diversified peers who can offset slippage in one market with gains elsewhere, Seritage faces increased sensitivity to local economic conditions affecting key markets such as Pennsylvania.

Additionally, capital recycling pressures manifest acutely when large asset disposals necessary for liquidity reduce invested bases faster than feasible reinvestment opportunities emerge given prevailing market conditions or strategic focus on winding down operations under the Plan of Sale [S1]. This dynamic constrains pricing power besides raising impairment risks acknowledged explicitly via recent recorded charges stemming from sales below carrying values

Key Growth Drivers and Potential Strategic Alternatives

Realistic value creation drivers presently hinge primarily upon disciplined execution of the Plan of Sale: securing transactions at favorable prices relative to book value to generate liquidity capable of fulfilling debt maturities while minimizing impairment losses [S1][S2]. Progress can be measured via KPIs such as contracts signed for asset sales considered probable, actual closings completed generating proceeds for debt repayment or reinvestment needs.

In parallel, Seritage’s Board continues oversight through a special committee evaluating broader strategic alternatives that could include a complete sale of the Company or exploring structured partnerships potentially unlocking shareholder value beyond piecemeal asset monetization alone [S1]. Given notable uncertainty around these alternatives materializing successfully within required timeframes [S2], they remain contingent on capital market receptivity and negotiation outcomes.

Alternative financing arrangements represent another lever that could alleviate near-term liquidity constraint if successfully secured before the Term Loan maturity date—a critical milestone looming shortly [S2]. Such financings might involve bridge loans, equity injections if feasible despite prevailing investor wariness along with potential amendments/extensions negotiated with Berkshire Hathaway under covenant frameworks detailed in loan agreements [S4][S5][S6].

Risks Focus: Liquidity, Concentration, and Going Concern Implications

Seritage discloses significant risks linked directly to its deteriorating liquidity profile: rental income falls short of covering operational expenses plus debt service requirements leading to recurrent negative operating cash flows ($34.9 million net outflow during full year 2025; $5.7 million net outflow in Q1 2026) that must be bridged with asset sales or financing infusions [S1][S2][S7]. Concentration risks also amplify overall vulnerability: geographic clustering particularly in Pennsylvania reduces sectoral diversification hence raising susceptibility to local macroeconomic shifts or tenant turnover impacts; tenant concentration exacerbates variability in rental revenues if major occupants vacate prematurely or request concessions [S1]. Recent impairment charges totaling tens of millions dollars underscore valuation pressures due predominantly to accepted offers below carrying value during sales plus loss recognition on investments in unconsolidated joint ventures held jointly but outside full control [S1].

Together these challenges drive substantial doubt regarding continuing operations within one year following financial statement issuance dates under ASC guidance; management currently admits plans do not alleviate this substantial doubt fully but continue preparing financials on going concern basis pending resolution outcomes [S2][S8]. Legal exposures compounded by shareholders’ securities class actions alleging misstatements related primarily to impairment assessments add further complexity albeit without presently material impact quantified [S17].

Investor Watchpoints: Upcoming Milestones and Strategic Decisions

Key events investors should monitor revolve mostly around execution reliability amid financial strain:

- Term Loan Facility Maturity (July 31, 2026): The imminent debt payoff deadline demands either sufficient accumulated liquidity from assets sold plus available cash or success in refinancing/extending facility terms; failure here triggers elevated default risk.

- Asset Disposition Developments: Announcements or filings evidencing new sales contracts judged probable closing soon would indicate tangible progression toward deleveraging objectives; absence thereof signals slower realization means tighter short-term funding gaps.

- Strategic Alternatives Process: Updates regarding Board Special Committee deliberations including engagement outcomes with third parties concerning possible Company sale or other transformative transactions could materially alter strategic outlook.

- Financing Transactions: Disclosure on emerging credit facilities or amendments providing breathing room before maturity underpin potential resilience against liquidity crunch.

- Operational Metrics: Monitoring tenant retention rates within remaining portfolio plus quarterly leasing spreads would help assess stability prospects for residual income streams post-sale phases.

Supplementary Financial Commentary

As per companyfacts data cut-off March 31, 2026 augmented by SEC disclosures:

- Cash & equivalents balance stood near $44.5 million providing immediate but limited liquidity cushion amidst obligations largely exceeding rental-derived operating cash flows [F1][S2].

- Total reported debt figures have historically approximated above $1 billion but outstanding senior secured Term Loan principal was reduced substantially by prepayments over prior years down to current $50 million level reflecting aggressive deleveraging efforts [F1][S21].

- Despite progress reducing absolute leverage exposure via sizable property sales yielding over $230 million gross proceeds in calendar year 2025 alone along with partial repayments against term loans [S1], negative net operating cash flow trends persist requiring continued dependence on capital markets or asset monetization strategies moving forward [S7].

- Company recorded impairments aggregating about $18.8 million for consolidated assets alongside roughly $8.5 million other-than-temporary impairments impacting unconsolidated holdings during fiscal year ended December 31, 2025 adding pressure on book value metrics relevant for investor assessment [S1].

This analysis focuses solely on factual disclosures from SEC filings combined with sector-contextual interpretation. It contains no investment advice nor forward-looking investment research views.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments