STERIS plc's Q3 2026 Growth and Innovation Amid Industry Challenges

STERIS's latest quarterly results reveal robust volume and pricing growth, supported by operational efficiencies that offset inflationary and regulatory pressures.

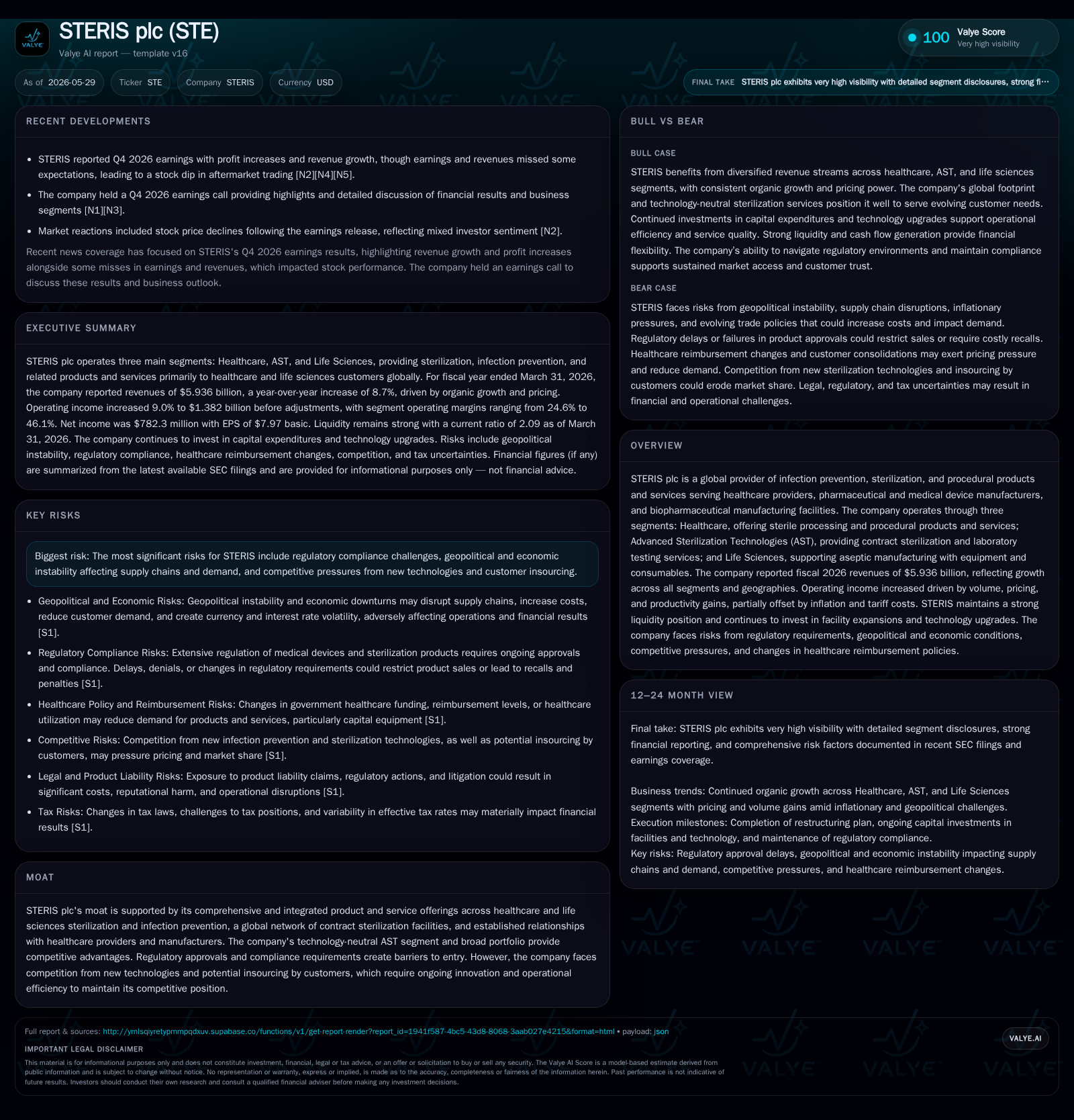

STERIS plc’s fiscal Q3 2026 results demonstrate sustained momentum across its Healthcare, Advanced Sterilization Technologies (AST), and Life Sciences segments. Revenue growth was driven by volume increases and pricing strength, while operational productivity improvements helped mitigate inflation and tariff headwinds. The company’s integrated business model leverages recurring service revenues alongside capital equipment sales, maintaining competitive positioning despite emerging technology threats and regulatory complexity. Going forward, industry dynamics such as evolving EO sterilization regulations and geopolitical risks remain watchpoints alongside innovation pipeline execution.

Recent Quarterly Operating Performance Highlights

STERIS plc reported Q3 fiscal year 2026 revenues of approximately $5.94 billion, marking an 8.7% increase compared to the prior year period—a reflection of solid organic growth driven by both higher volumes and incremental pricing across its three core segments: Healthcare, AST, and Life Sciences [S2], [S1]. Service revenues grew at a double-digit rate (11.1%), primarily fueled by recurring sterile processing contracts and contract sterilization services within AST, while consumables and capital equipment revenues also expanded moderately during market demand recovery and new product introductions [S1].

Gross profit for the quarter reached about $2.63 billion with a slight improvement in gross margin to 44.2% from 44.0% a year earlier. This improvement owed largely to enhanced operational productivity and favorable pricing effects which contributed approximately +120 basis points to margins, although these were partially offset by higher inflationary pressures (+70 basis points), tariff impact (+80 basis points), raw material costs (+30 basis points), currency translation (-10 basis points), and product mix shifts (-30 basis points) [S1]. The company's focus on lean operating models and restructuring initiatives helped reduce restructuring expenses dramatically compared to previous periods, further supporting profitability.

The current ratio stands at a comfortable 2.09x demonstrating short-term solvency [F1]

Comprehensive Business Model and Segment Analysis

STERIS operates through three primary reporting segments that collectively address infection prevention, sterilization services, and aseptic manufacturing needs for healthcare providers and life sciences manufacturers globally:

Healthcare: This segment centers on sterile processing solutions including capital equipment for sterilizers along with related consumables (e.g., disinfectants) plus procedural products used during surgeries or endoscopic procedures. Revenue here is driven by a mix of recurring service contracts tied to maintenance/support alongside instrument sales. The business benefits from significant switching costs due to rigorous validation requirements for sterility assurance in clinical settings.

Advanced Sterilization Technologies (AST): AST provides contract sterilization services using multiple technologies—ethylene oxide (EO), vaporized hydrogen peroxide (VHP), gamma radiation among others—via an extensive global network encompassing over 60 specialized facilities offering laboratory testing as well. This segment is notable for its technology-neutral approach enabling flexible service offerings tailored to client device specifications or regulatory frameworks. Contract sterilization generates recurring revenue streams with degree of pricing power underpinned by limited alternatives for complex devices where outsourcing expertise is critical.

Life Sciences: Focused on supporting aseptic manufacturing processes for biopharmaceutical production through advanced consumables and specialized equipment tailored for contamination control environments. This segment ties into growing pharmaceutical R&D activity worldwide particularly biologics requiring stringent sterile conditions.

The integrated model spanning equipment sales balanced with consumable supplies plus contract sterilization services creates layered revenue streams combining stickiness from established customer relationships with exposure to capital expansion cycles in healthcare infrastructure. Product quality standards are high given stringent FDA/EMA approvals required across medical device sterilizers reflecting significant barriers for new entrants. STERIS emphasizes innovation governance with targeted R&D investments aimed at sterile processing enhancements plus procedural accessories supporting minimally invasive surgeries or endoscopy—a growing sub-niche within Healthcare segment proximal to high-margin consumable sales growth potential [S1], [S15], [S13].

Competitive Position and Industry Dynamics

STERIS's competitive moat stems from several interrelated factors: extensive scale in contract sterilization with a global footprint offering redundancy/reliability essential for medical device manufacturers; adherence to complex international regulations governing biocompatibility and sterility; diversified portfolio reducing dependence on any single modality or geography; ongoing innovation in both capital equipment design as well as consumable enhancements; deep customer integration featuring long-term service contracts; plus strong intellectual property protecting proprietary process improvements.

However, emerging threats include evolving regulations especially those affecting EO sterilization which comprises a portion of the AST segment’s activities—EO usage faces tightening emissions limits due to carcinogenic classification by EPA increasing operational complexities and potential liabilities associated with facility emissions litigation risk (as seen in prior adverse judgments notably in Illinois). Additionally, competitor innovations such as alternative non-EO sterilization technologies or internal insourcing by large medical device manufacturers aiming to reduce dependence on external providers could pressure pricing or volumes over time [S9], [S14], [S20].

Supply chain disruptions resultant from geopolitical uncertainty also pose intermittent challenges given reliance on sourcing key materials globally; tariffs introduce added input cost volatility constraining margin expansion even as pricing adjustments seek partial offsetting effect. Notably though, regulatory approvals required for any new sterilization modality or capital equipment act as natural entry deterrents limiting peer encroachment yet simultaneously compel continuous operational excellence from STERIS to retain market leadership [S9], [N9].

Growth Drivers: Innovation, Market Expansion, and Productivity

Several structural tailwinds underpin STERIS's path to growth:

Global healthcare infrastructure investment: Aging populations combined with rising surgical procedure volumes support ongoing demand for sterile processing technologies across mature markets like the US but also significant expansion opportunities within developing regions where infection control standards are upgrading.

Life Sciences backlog expansion: The company reported an increase in Life Sciences backlog from around $83.7 million to $98.7 million year-over-year indicating tightened project pipelines aligned with accelerated biotech manufacturing build-outs requiring advanced aseptic solutions.

R&D investments: Fiscal 2026 saw increased expenditure dedicated to sterile processing capabilities enhancement plus endoscopy procedural products signaling focused pipeline progression towards differentiated accessories aimed at improving clinical outcomes.

Pricing resilience supported by product mix: The ability to incrementally raise prices amid inflationary environments while shifting towards higher-margin consumables demonstrates adaptability in revenue mechanics.

Productivity initiatives: Continued lean manufacturing adoption coupled with facility expansion efforts especially within Healthcare/AST segments optimize capacity utilization helping counterbalance input cost inflation effects highlighted in operating expense discussions.

These factors combine cyclical capital equipment spending influenced by hospital budgets with structurally recurring revenue streams from consumables and long-term service contracts emphasizing predictability alongside growth scalability potential driven by geographic diversification and technological evolution in procedural products/services [S1], [S13], [N1].

Risks and Constraints: Regulation, Inflation, and Competitive Pressures

While STERIS has demonstrated solid execution recently, it faces several notable risks:

Regulatory environment: EO sterilization operations encounter legal exposure from emissions lawsuits creating uncertain future costs or constraints that could significantly impact AST segment profitability if facility closures or costly upgrades become mandated without viable alternatives readily deployable.

Inflationary pressure: Input cost increases ranging from raw materials to energy tariffs erode margin gains despite managed price increases; labor inflation also contributes more than modestly raising SG&A expenses.

Customer insourcing: Key clients may seek vertical integration reducing outsourced contract sterilization reliance thereby pressuring volume growth trajectory.

Geopolitical instability: Trade policy shifts add complexity/costs including currency fluctuations undermining foreign revenue conversion margin impacts.

Healthcare reimbursement changes: Variations in government payor systems or funding cuts can depress hospital purchasing patterns affecting capital product sales more acutely.

Given these constraints the company must sustain disciplined operating leverage management accompanied by ongoing innovation acceleration ensuring competitive differentiation remains intact amidst mounting external challenges documented extensively in risk disclosures across fiscal filings [S9], [S11], [S14], [N9].

Key Milestones to Monitor Next

Key indicators deserving attention as STERIS progresses through fiscal 2027 include:

- Upcoming quarterly earnings releases detailing continued volumetric/price trends especially within AST contract wins or announced capacity expansions which would signal ability to capture structural demand drivers;

- Life Sciences backlog updates providing early visibility into multi-quarter project flows reflecting robustness of the pharmaceutical manufacturing investment cycle;

- Pricing power sustainability amid broader inflation adjustments impacting margins;

- Regulatory developments around EO sterilization emission limits or new modalities adoption affecting AST operations;

- R&D innovation outcomes translating into new product launches particularly within procedural accessories enhancing addressable markets;

- Cash flow generation trends confirming capital flexibility aligning with announced multi-year technology upgrades supporting Healthcare/Life Sciences segments workflow optimization initiatives outlined in latest annual report projections.[S3], [N2]

Stakeholders should track these milestones closely to assess if strategic investments translate effectively into operational scale gains amidst the challenging macro-regulatory landscape.

Financial Profile Summary

Reflecting operating progress noted above, STERIS ended Q3 FY26 with revenues near $5.94 billion complemented by operating income exceeding $1.10 billion generating net income around $782 million reflecting steady margin profiles after adjusting for inflation/tariffs effects recorded during the period [F1],[S2]. Liquidity appears prudent given cash & equivalents approximating $424 million paired against total debt near $1.81 billion producing moderate leverage levels supported by consistent free cash flow conversion noted in recent annual figures facilitating ongoing capital expenditures ($369 million FY26) targeting strategic facility expansions and technology upgrades crucial for sustaining long-term competitive positioning within Healthcare/AST/Life Sciences operations.[F1],[S4],[S6]

This analysis is based solely on publicly available filings through May 2026 without investment advice or research views.

Financial position in context

As of 2026-03-31, companyfacts shows $424mm in cash and equivalents and $1.81bn of total debt [F1]. The same snapshot implies net debt of roughly $1.39bn, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $2.39bn and current liabilities of $1.15bn imply a current ratio near 2.09x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments