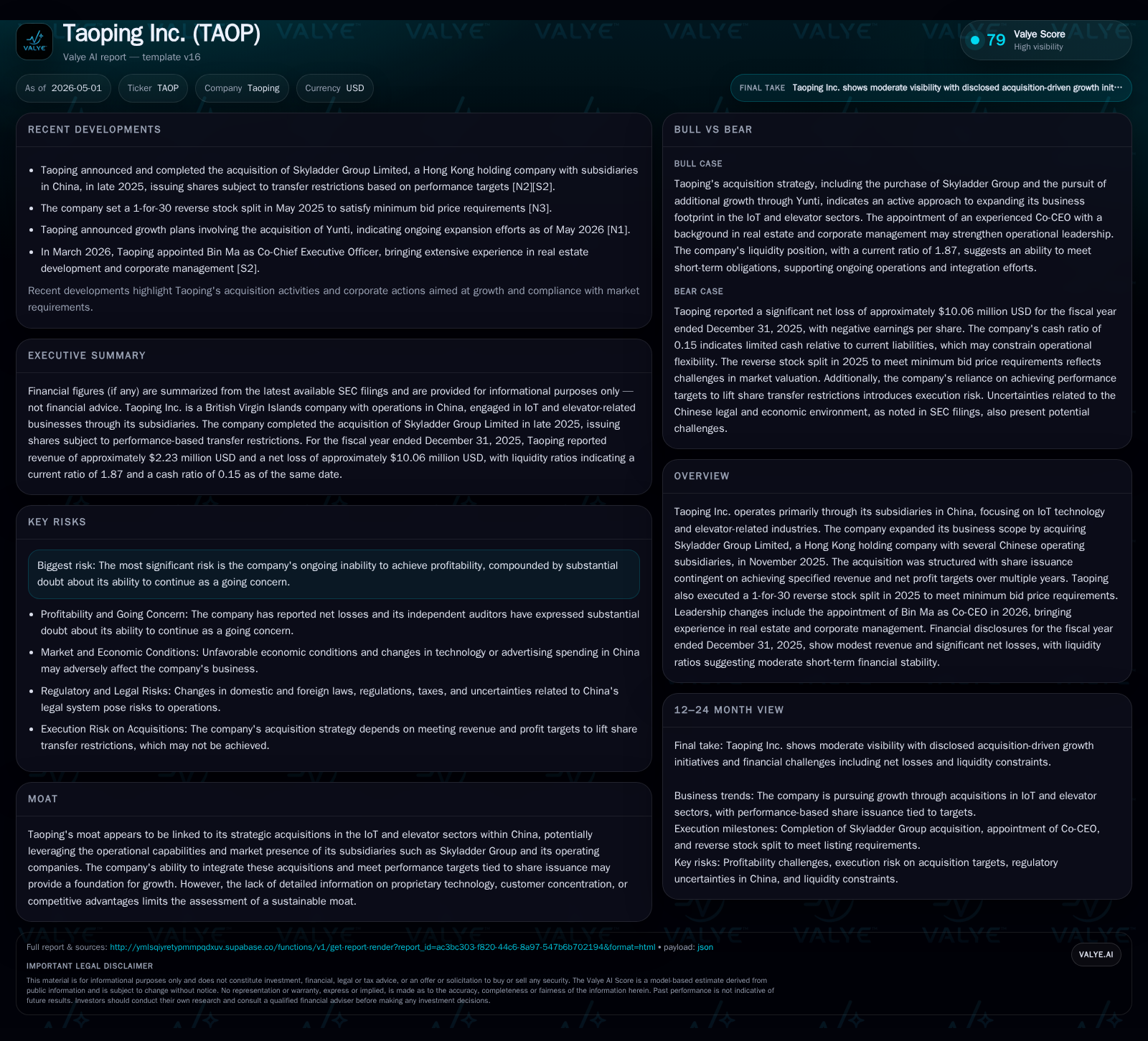

Taoping Inc. Accelerates IoT and Elevator Sector Expansion with Skyladder Acquisition and Leadership Shift

Recent quarterly filings spotlight Taoping’s strategic acquisition of Skyladder Group, leadership enhancement, and ongoing profitability challenges.

Taoping Inc. has deepened its foothold in China’s IoT and elevator sectors through the November 2025 acquisition of Skyladder Group, a move structured around conditional share issuances tied to long-term revenue and profit targets. The April 2026 quarterly disclosures reveal the integration of multiple subsidiaries under Skyladder and mark leadership changes with Bin Ma’s appointment as Co-CEO. Despite these strategic initiatives, Taoping continues to grapple with significant net losses and substantial doubt over going concern status. The company’s growth hinges on hitting operational milestones from Skyladder while scaling its broader smart city IoT solutions amid competitive pressures and regulatory uncertainties.

Recent Operating Update

Taoping Inc.'s latest operational landscape is dominated by its November 26, 2025 acquisition of Skyladder Group Limited through its wholly owned subsidiary Taoping Holdings Limited [S3]. This move brought under Taoping's umbrella several Chinese operating entities: Shenzhen Smart Skyladder IoT Co., Ltd., Tianjin Zeyuan Elevator Co., Ltd., Tianjin Weida Elevator Co., Ltd., among others [S3], [S20]. Post-acquisition consolidation was finalized after June 30, 2025, notably with the formation of Skyladder Tianjin Technology Development Co., Ltd. in late July 2025 as an intermediate holding company [S20].

The acquisition consideration was approximately RMB152 million ($21.36 million), payable via issuance of about 7.88 million ordinary shares with transfer restrictions conditioned on achieving specific audited revenue and net profit targets spanning from Q4 2025 through 2029 [S9], [S18]. These performance benchmarks are stringent—for instance, the target for 2026 alone requires revenues of RMB74.14 million ($10.4 million) and net income of RMB3.80 million (~$0.53 million) [S9]. Failure to meet such targets could delay or cancel share issuance tranches.

Additionally, April 2026 filings document leadership changes with Mr. Bin Ma appointed as Co-CEO alongside Jianghuai Lin [S21]. Mr. Ma's background includes chairmanship at Skyladder Group since 2023 and significant real estate development experience relevant for overseeing integration and growth strategies within elevator-related verticals [S21].

Business Model

Taoping Inc.'s core operating framework revolves around providing IoT-enabled smart city platforms coupled with digital advertising network solutions primarily targeted at Chinese governmental bodies, urban residential complexes, education sectors, media companies, transportation authorities, and private enterprises [S1]. Its product portfolio spans hardware—such as intelligent display terminals tailored for out-of-home advertising—and software offerings including cloud-based SaaS that delivers ongoing recurring revenues from platform subscriptions [S1].

The integration of Skyladder extends Taoping’s scope materially into elevator equipment manufacturing and service provisions via its acquired subsidiaries like Tianjin Weida Elevator Co., known players within China's local urban infrastructure markets [S3], [S16]. Revenue mechanics rely on upfront hardware sales complemented by system integration contracts plus recurring SaaS fees from clients adopting Taoping’s cloud platforms [S1]. The hybrid nature—combining tangible elevator systems with digital IoT monitoring solutions—could differentiate Taoping if effectively leveraged.

Revenue growth is expected to be driven via cross-selling Skyladder's established elevator clientele enhanced by Taoping’s IoT capabilities plus expansion within municipal smart city projects delivering environmental governance solutions such as autonomous street sweeping and wastewater treatment stations introduced recently [S1]. However, the company still generates limited revenue relative to costs indicating an early developmental stage business model struggling with scale economies.

Industry Structure and Competitive Position

Taoping occupies an intersection of several convergent industries: smart city IoT infrastructure, digital out-of-home advertising technology, elevator manufacturing/service, and environmental technology solutions focused on low-carbon governance in urban/rural China [S1]. Each sector features strong incumbents with well-established distribution networks, sizable R&D budgets, or entrenched government contracts.

Within China's massive elevator market dominated by giants like Otis China (UTC), KONE China, and domestic leader Canny Elevator Corporation (CEC), Taoping’s Skyline subsidiaries currently hold a niche but not dominant position—primarily serving regional or mid-tier clients rather than national-scale projects [S3], [S16]. In IoT platforms for smart cities and environmental solutions, competitors range from Alibaba Cloud-backed providers to local state-owned firms benefiting from government procurement preferences.

Taoping's relative competitive advantage potentially stems from its ability to bundle elevator hardware/services with integrated IoT monitoring systems and emerging AI-powered smart terminals unveiled in May 2024 that blend content delivery with intelligent control capabilities [S1]. However, no evidence suggests proprietary patents or breakthrough innovations narrow enough to constitute a robust moat; market differentiation leans more toward integration efficacy across acquired units.

Growth Drivers

Skyladder Integration & Expansion: Meeting the rigorous financial targets set in the acquisition agreements unlocks incremental share-based equity incentives while signaling operational momentum. Successful integration enables cross-selling/up-selling within elevators combined with IoT sensor deployments to smart building management clients.

Smart City Initiatives: Leveraging existing contractual relationships in cities like Zhaoyuan (Shandong) and Wuxuan (Guangxi) provides stable revenue foundations through municipal projects focusing on autonomous street cleaning systems, off-grid wastewater treatment units leveraging cloud telemetry platforms [S1].

Cloud-based SaaS Upscaling: While early-stage currently generating modest monthly recurring revenues (MRR), continued rollout of smart digital media terminals integrated with AI capabilities can gradually shift revenue mix towards higher-margin software subscriptions over time.

New Product Innovations: The launch of AI-integrated smart terminals represents a technological upgrade aimed at both commercial advertising ecosystems and urban governance monitoring potentially enhancing user engagement metrics.

Regulatory & Environmental Policies: China’s proactive push towards low-carbon urban renewal may favor suppliers like Taoping offering comprehensive intelligent environmental governance products.

Risks / Constraints

- Profitability Challenges: Historically significant net losses ($10 million in FY25) suggest ongoing cash burn requiring external financing or improved operational leverage to sustain growth plans [F1], [S1].

- Going Concern Doubts: Auditors have flagged substantial doubt about Taoping’s ability to continue as a going concern unless financial performance stabilizes or new capital inflows materialize [S1].

- Acquisition Integration Risks: Combining disparate entities under the Skyladder umbrella entails operational complexities; failure could stall synergy realization or dilute managerial focus adversely impacting results [S1].

- Regulatory Uncertainty: Operating primarily in China exposes Taoping to potential policy shifts around foreign investment law applicability affecting PRC subsidiary structures as well as sector-specific compliance constraints within tech infrastructure provision domains [S1].

- Capital Market Pressure: Maintaining Nasdaq listing standards post-reverse stock split (completed in 2025) is critical; trading volatility can hamper capital raising capabilities limiting runway for growth investments [S1].

- Market Competition: Entrenched competitors in both elevator manufacturing/service industries and cloud-IoT platform spaces exert pricing pressure possibly compressing margins or restricting client acquisition gains.

What to Watch Next

- Milestone fulfillment regarding revenue/profit targets underpinning share issuance from Skyladder acquisition tranches; first tranche unlocking conditionals relate to Q4’25/Q1’26 results [N1], [S8], [S9], [S18].

- Progress updates on integration efficiency including consolidated financial performance indicators for Skyladder subsidiaries in upcoming quarterly filings.

- Adoption curves of AI-powered smart terminals within core customer bases; uptake signals could presage margin improvement should SaaS subscription base grow materially.

- Liquidity events such as capital raises or debt refinancing occurring due to current leverage profiles indicated by ~$3.6M net debt at end FY25 despite $2.13M cash reserves [F1].

- Regulatory developments impacting foreign holding structures or PRC operational authorizations which may affect scalability plans.

- Further executive hires or corporate restructuring indicating strategic reorientation or capability build-out focusing on core verticals.

Financial Profile Summary (FY December 31, 2025)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $2mm | |

| 2025-12-31 | ||

| Total debt | $6mm | |

| 2025-12-31 | ||

| Net debt | $4mm | |

| 2025-12-31 | ||

| Current assets | $26mm | |

| 2025-12-31 | ||

| Current liabilities | $14mm | |

| 2025-12-31 | ||

| Current ratio | 1.87x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

The figures reflect low top-line traction against large operating deficits consistent with early-stage growth investing amid heavy acquisitions-related costs plus R&D outlays for product development initiatives. The current ratio near two suggests manageable short-term liquidity but overall capital structure remains leveraged with net debt approximately $3.6 million after offsetting cash balances [F1]. This profile underscores reliance on successful deal integration plus operational leverage enhancements to transition towards sustainability.

This analysis incorporates publicly available disclosures filed by Taoping Inc., SEC reports and company facts data without conjecture beyond presented evidence. It aims to provide a fact-based industry-focused review anchored in the latest quarterly filings while identifying structural growth potential balanced by prevailing risk factors typical for evolving IoT-elevator sector integrators within Chinese markets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments