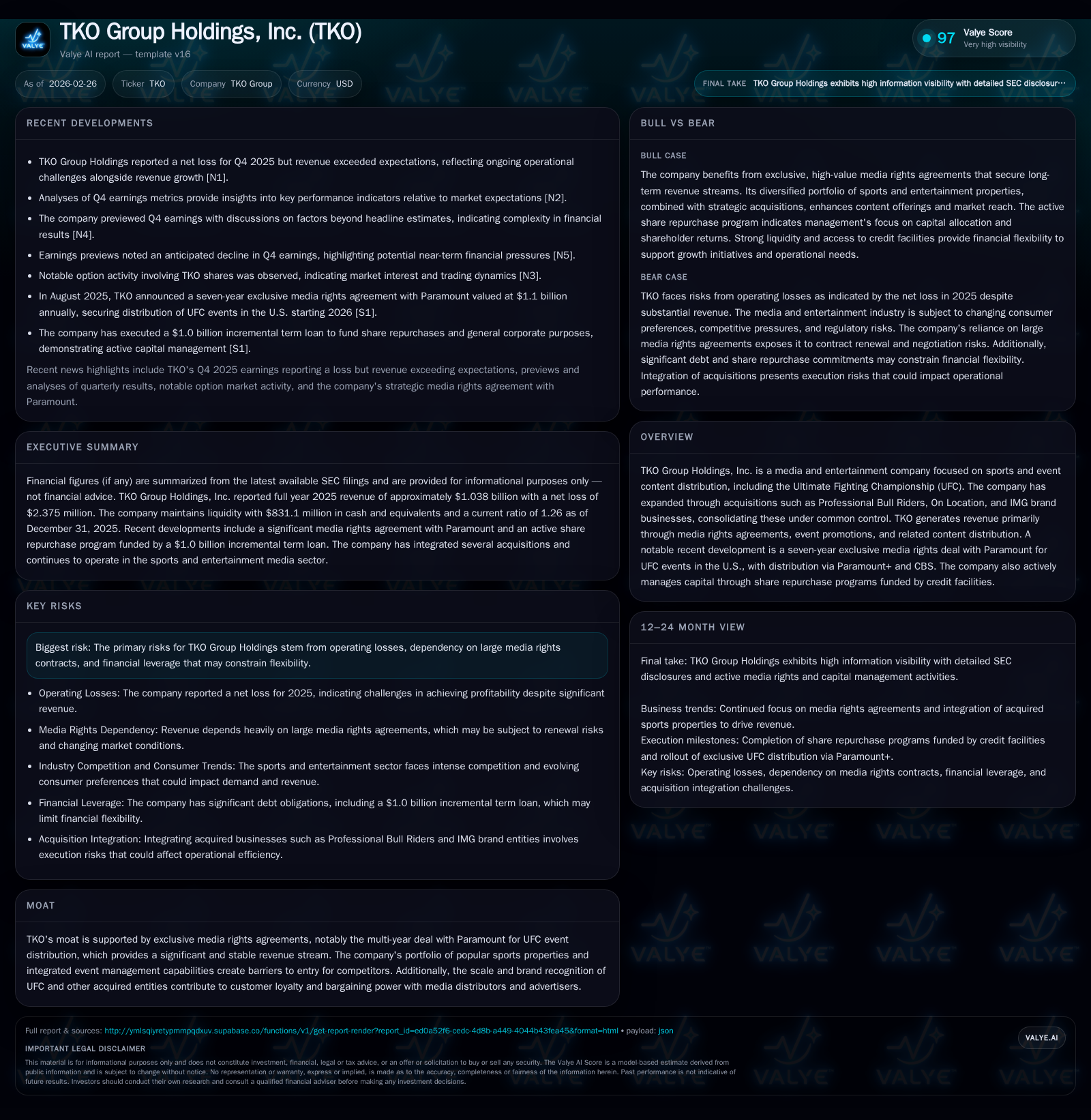

TKO Group Holdings Confronts Revenue Volatility and Leverages Media Rights for Growth

TKO's premium sports assets and exclusive media rights underpin its revenue base despite profitability challenges and leverage pressures.

TKO Group Holdings experienced a dramatic 63% revenue decline in fiscal 2025, primarily reflecting the timing and profile of media rights monetization. However, operating cash flow more than doubled, signaling effective working capital management and non-cash adjustments balancing top-line contraction. The firm's portfolio growth via acquisitions and a landmark seven-year UFC media rights deal with Paramount enhances its recurring revenue visibility. Meanwhile, operating income fell sharply, reflecting margin pressures from elevated content and promotional investments. TKO’s capital strategy centers on refinancing to extend debt maturities and aggressive debt-funded share repurchases totaling $867 million in FY25. Forward growth hinges on sustained media rights renewals and leveraging integrated sports franchises, with key risks tied to contract dependency and financial flexibility constraints.

Fiscal 2025 Overview: Sharp Revenue Retraction Versus Growing Cash Flows

The fiscal year ending December 31, 2025 presented a stark dichotomy for TKO Group Holdings between top-line contraction and cash flow expansion. Total revenue plummeted by approximately 63%, falling from $2.8 billion in FY24 to just over $1 billion in FY25 [F1]. This precipitous decline contrasts markedly with operating cash flow (CFO), which more than doubled – surging from $583 million to nearly $1.29 billion year-over-year [F1]. The divergence underscores effective management of working capital or significant non-cash adjustments that offset the softness in revenue recognition.

Operating income suffered a severe compression of almost 80%, narrowing to $57 million from $283 million the prior year, indicative of margin pressures likely arising from elevated content acquisition or event promotion costs characteristic of sports media monetization cycles [F1]. Net income swung back into a modest loss territory at approximately -$2.4 million after a small profit in FY24 but showing improvement over the substantial loss seen in FY23 [F1].

This financial pattern creates tension: while headline revenue is volatile—driven by the nature of contracting cycles in media rights monetization—the underlying operations generated robust cash flows signaling resilient business fundamentals when adjusting for accounting timing effects.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1.0 | -2 | 1286 | 57 | -63.0% | -125.2% |

| 2024 | 2.8 | 9 | 583 | 283 | +67.4% | +126.7% |

| 2023 | 1.7 | -35 | 468 | 447 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 867 | -0.1 | |

| 2024 | 165 | 571 | 0.2 |

| 2023 | 100 | 446 | -0.9 |

Source: SEC companyfacts cache [F1].

Revenue and income figures are millions USD; capex is approximated if available; YoY based on reported values.

Revenue Drivers and Portfolio Evolution: Impact of Acquisitions and Media Deals

TKO’s historical revenue growth has been underpinned by an expanding portfolio anchored by marquee sports properties such as the Ultimate Fighting Championship (UFC), augmented via strategic acquisitions including Professional Bull Riders (PBR), On Location experiential events, and segments of the IMG brand businesses consolidated under one domain of common control [S9][N1].

Central to long-term revenue visibility is the multi-year exclusive media rights agreement signed with Paramount in mid-2025 covering UFC events across the U.S., featuring an average annual value around $1.1 billion over seven years. This deal positions Paramount+ as the primary direct-to-consumer platform with CBS simulcasts providing supplemental distribution breadth beginning in calendar year 2026 [S16][S22].

This arrangement exemplifies classic 'media rights monetization' dynamics prevalent in premium sports sectors where substantial upfront licensing revenues provide recurring streams subject to stipulated escalators but also front- or back-weighted payment profiles that influence reported revenue volatility on a fiscal basis.

The integration of these diversified franchises delivers not only scaling synergies but also reinforces cross-promotional opportunities between live event promotions, content licensing, international distribution, and brand licensing—important pillars supporting future growth prospects.

Operating Profit Volatility and Profitability Challenges

While TKO maintains a premium bouquet of sports assets commanding notable pricing power in media rights markets, its operating results reveal pronounced earnings volatility reflective of the inherently lumpy content spend cycles characteristic of live sporting event enterprises.

Specifically, operating income fell nearly four-fifths year-over-year to approximately $57 million in FY25 from $283 million in FY24 despite stable underlying demand signals for premium content [F1]. EBIT margin compression highlights increased fixed or promotional expenses during periods of investment into customer acquisition or event staging costs designed to sustain competitive positioning amid escalating industry costs.

Net losses narrowed marginally compared with prior years albeit remaining negative (-$2.4 million), pointing toward ongoing operational leverage challenges where incremental revenues must significantly outpace increasing direct costs to restore robust profitability margins [F1].

These dynamics underscore challenges faced by media-centric sports operators who must continually balance premium content acquisition pricing pressures alongside subscriber engagement initiatives within competitive subscription ecosystem frameworks.

Capital Structure, Leverage Profile, and Credit Facility Amendments

TKO took prudent steps during FY25 to refine its capital structure amid persistent leverage headwinds typical for highly acquisitive media companies with substantial rights amortization schedules.

Notably, an amendment executed on September 15, 2025 refinanced existing first lien secured term loans while adding an incremental $1 billion first lien term loan tranche bearing variable interest linked to Term SOFR plus margins ranging around +2%, with sovereign floors ensuring minimum interest rates [S6][S10][S25]. The amended revolving credit facility maturity extended to September 2030 offering longer runway liquidity [S6].

Such refinancings align with best practices among leveraged sports media operators who rely on covenant-light-ish credit facilities structured around key ratio overlays including first lien leverage ratios that influence borrowing cost spreads and amortization schedules typically spanning six years or more.

While this financial engineering introduces certain interest rate variability exposure given floating rate debt instruments under SOFR/ABR benchmarks it provides critical mid-term maturity extension relieving near-term refinancing risk.

Share Repurchase Program as a Tool for Capital Allocation

Despite operating challenges and elevated leverage levels, TKO deployed an aggressive capital return strategy in FY25 through sizable share repurchases aggregating $867 million—a marked acceleration versus previous years ($165 million in FY24) [F1][S11][S12][S14].

This included an Accelerated Share Repurchase (ASR) agreement executed alongside Morgan Stanley for $800 million funded explicitly via proceeds from the incremental term loan raised concurrently with refinance activities, supplemented by further purchases under a Rule 10b5-1 trading plan targeting roughly $174 million more [S11][S12].

This reflects sophisticated buyback execution balancing balance sheet utilization: converting debt capacity into stock buybacks rather than dividends amid ongoing profitability uncertainties whilst maintaining investor-aligned capital return discipline.

Such deployment represents calculated leveraging tradeoffs wherein share count reduction potentially enhances per-share metrics offsetting short-term debt service cost increases—common practice among large-scale media asset holders optimizing returns when organic free cash flow generation is nascent or reinvestment-intensive.

Assessing Forward Growth Catalysts Anchored in Premium Sports Properties

Looking ahead, TKO's growth outlook hinges critically on renewing and extending key exclusive media rights contracts underpinning its flagship properties such as UFC under the multi-year Paramount deal carrying high visibility through at least early next decade [N3].

Furthermore, integration benefits across acquired entities like PBR events and On Location's experiential platforms could drive enhanced cross-sell marketing potency creating new monetization avenues beyond traditional broadcasting licenses—a trend echoing broader shifts toward hybrid digital-live event ecosystems embraced by premium sports franchises globally.

Stable 'media rights renewal visibility,' supported by incremental escalators typical within contractual terms—including single-digit annual uplifts aligning with industry standards—may gradually re-anchor top-line stability after recent episodic volatility resulting from contract timing disparities [S22].

Also notable is potential expansion into ancillary content distribution channels leveraging parametric data analytics innovations aiming at fan engagement optimization—a frontier gaining currency among sports entertainment conglomerates seeking sustainable differentiation.

Identifying Key Risks: Dependency on Media Deals and Financial Flexibility Constraints

Per SEC filings detailing risk disclosures [S4][S5][S7], TKO faces several structural risks worthy of close attention:

- High dependency on a handful of large-scale media rights deals renders revenues vulnerable should contract renegotiations falter or market conditions deteriorate unexpectedly ('contract dependency risk').

- Persistent operating losses alongside high leverage position constrain financial flexibility limiting maneuverability especially if economic headwinds impact advertising or subscription growth.

- Regulatory scrutiny coupled with ongoing litigation exposures inherent to public entertainment enterprises add layers of legal risk potentially impacting earnings trajectories.

- Covenants embedded within credit agreements restrict dividend payments beyond nominal amounts without lender consent potentially limiting future capital return strategies under adverse scenarios. These factors necessitate vigilant monitoring among stakeholders given their material impact potential on both operational execution capacity and strategic financial decision making.

Outlook Indicators: What Investors Should Track Next

While explicit forward guidance remains absent post-FY25 release ([N3],[N4]), key performance indicators should be evaluated closely including:

- Renewal cadence and terms of substantial UFC/Paramount media rights contracts affecting near-to-midterm revenue forecasts ('content renewal cadence').

- EBIT margin trajectory reflecting management’s ability to contain escalating content production/promotion expenses balanced against subscription growth gains ('EBIT margin contraction/recovery').

- Sustainability metrics surrounding free cash flow generation considering recent CFO uptick juxtaposed against ongoing capex requirements ('free cash flow generation surveillance').

- Progress on deleveraging initiatives or further capital allocation decisions encompassing potential additional share repurchases impacting leverage multiples. Effective tracking of these indicators will illuminate evolving fundamentals underlying TKO’s complex interplay between growth ambitions versus profitability/leverage realities customary within premium sports media operators.

Disclaimer: This analysis is provided solely for informational purposes without any investment recommendation or advice intended.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments