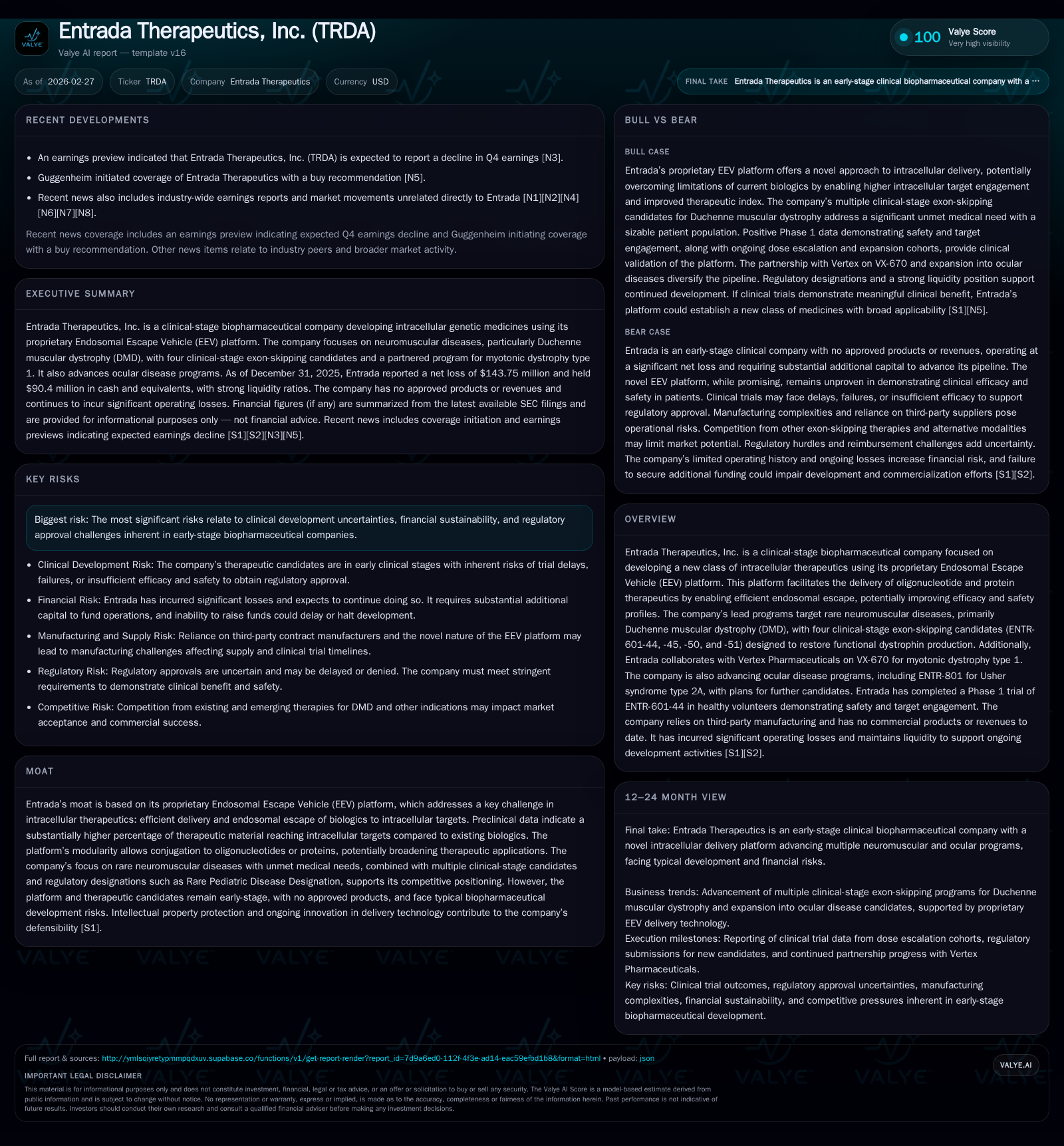

Entrada Therapeutics’ Operating Loss Deepens Amid Clinical Development Progress and Regulatory Advances

Clinical-stage biopharma Entrada Therapeutics advances Duchenne muscular dystrophy pipeline with active trials but faces widening operating deficits and typical industry risks.

Entrada Therapeutics, Inc. (TRDA) is progressing multiple clinical programs targeting rare neuromuscular diseases through its proprietary Endosomal Escape Vehicle platform enabling intracellular delivery of oligonucleotide therapeutics. The lead DMD exon-skipping candidates are in Phase 1/2 trials with expected mid-2026 data readouts. Collaborations with Vertex advance development in myotonic dystrophy. Despite regulatory milestones including FDA Rare Pediatric Disease Designation, Entrada reported a steep decline in operating and net income for FY2025, continuing its pattern of operating losses typical for clinical-stage biotech firms without approved products or revenue. Cash runway and clinical outcomes remain key near-term value drivers.

Historical Performance

Since its founding in 2016, Entrada Therapeutics has focused on developing its Endosomal Escape Vehicle (EEV) platform and advancing therapeutic candidates into clinical trials. The company’s financial results over the past four fiscal years illustrate significant volatility typical of early-stage biopharma firms investing heavily in R&D without product revenues. Operating income swung from losses exceeding $97 million in FY2022 to a positive $47 million in FY2024 before plunging back to an operating loss of approximately $158 million in FY2025 [F1]. Net income followed a similar trajectory with a positive result only in FY2024.

Operating cash flow deteriorated markedly from a positive $140 million in FY2023 to a negative free cash flow estimated at -$129.5 million in FY2025 (operating cash flow minus capital expenditures) [F1]. Capital expenditures remained modest relative to overall expenses.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -144 | -129 | -158 | 1 | -319.0% |

| 2024 | 66 | -42 | 47 | 3 | +1081.7% |

| 2023 | -7 | 140 | -3 | 6 | +92.9% |

| 2022 | -95 | -94 | -97 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -130 | -47.0 |

| 2024 | -45 | 15.3 |

| 2023 | 134 | -2.8 |

| 2022 | -97 | -44.5 |

Source: SEC companyfacts cache [F1].

Fiscal years end December 31; financials rounded.

Business Overview and Platform

Entrada’s EEV platform aims to overcome challenges associated with intracellular delivery by facilitating escape of therapeutic molecules from late endosomes within cells. This mechanism addresses a critical bottleneck limiting the effectiveness of RNA- and protein-based therapies. The company’s modular EEV conjugates are designed to enhance payload delivery efficiency potentially improving potency and reducing off-target effects [S1].

The primary focus is on rare neuromuscular disorders with unmet medical needs and genetically defined patient populations.

Current Pipeline and Clinical Development

Duchenne Muscular Dystrophy (DMD) Franchise

The company is developing four exon-skipping candidates—ENTR-601-44,-45,-50,-51—targeting mutations amenable to restoration of dystrophin protein across about 11,500 patients in the U.S. and Europe [S1]. The ELEVATE-44-201 Phase 1/2 trial for ENTR-601-44 completed dosing Cohort 1 at 6 mg/kg with safety data supporting dose escalation cohorts at up to 18 mg/kg. Data readouts are anticipated throughout 2026 including dystrophin production metrics where initial double-digit percentage increases are expected with projected multi-fold gains at higher doses. Expansion cohorts are planned to support potential accelerated approval pathways following the FDA’s Rare Pediatric Disease Designation awarded in December 2025 [S1].

Other trials include ENTR-601-45 dosing ongoing cohorts with similar data timelines; ENTR-601-50 is progressing through EU trial filing preparations while regulatory submissions for ENTR-601-51 are underway [S1].

Partnership with Vertex Pharmaceuticals (VX-670)

In collaboration with Vertex Pharmaceuticals, Entrada is advancing VX-670 targeting myotonic dystrophy type 1. Dosing completion is expected by mid-2026 [S1]. Given all candidates utilize the EEV platform for endosomal escape mechanisms across oligonucleotide therapies, early clinical data may provide insights applicable across the pipeline.

Ocular Disease Programs

Additional programs target ophthalmologic genetic diseases such as Usher syndrome type 2A via candidate ENTR-801 with earlier stage development compared to neuromuscular assets [S1].

Financial Position and Capital Allocation

As of December 31, 2025 Entrada held approximately $90 million in cash and equivalents against current liabilities near $24 million yielding a robust current ratio exceeding 12x indicative of strong liquidity [F1][S15][S8]. However, steep net losses (-$144 million) alongside negative operating cash flows underscore ongoing reliance on equity financing or partnerships for funding future operations [F1].

No revenues have been generated as no products have received regulatory approval or commercialization; all expenditures relate to research operations including clinical trials execution, personnel costs supporting scientific teams focused on EEV platform development plus administrative overheads [F1].

No dividends or share repurchases were reported indicating full retention of capital for reinvestment into R&D efforts.

Regulatory Environment and Risks

The FDA’s Rare Pediatric Disease Designation positions ENTR-601-44 favorably for potential expedited approval but does not eliminate risks tied to clinical efficacy outcomes or market access post-commercialization [S1][S4]. Compliance risks include navigating complex healthcare laws around anti-kickback statutes as well as pricing pressures from government payors which could impact reimbursement levels [S4][S5][S20]. Intellectual property protection remains critical given the novel platform status requiring vigilance against infringement claims common in the industry [S16][S25].

Operational risks extend beyond clinical setbacks including compliance with evolving privacy regulations such as EU GDPR/UK GDPR plus U.S. healthcare fraud statutes necessitating robust governance practices [S9][S13][S21]. Employee or contractor misconduct poses reputational hazards especially during sensitive trial phases [S23]. Environmental regulations add incremental cost layers related to hazardous materials handling though workers’ compensation insurance partially mitigates exposure [S7][S12].

Forward-Looking Considerations

With multiple Phase 1/2 studies underway and data readouts scheduled through calendar year 2026—including efficacy biomarkers like dystrophin quantification—clinical results will be pivotal inflection points shaping longer-term viability assessments of the EEV-enabled exon-skipping approach.

Capital sufficiency depends on ability to raise funds under prevailing biotech financing conditions combined with successful demonstration of meaningful target engagement alongside tolerability given prior losses requiring sustained investor confidence.

Expanding indications within rare disease niches leveraging platform modularity could broaden growth potential albeit paced by regulatory hurdles plus payer acceptance complexities common among orphan drug commercializations.

Partnerships such as that with Vertex represent risk mitigation avenues yet introduce dependency dynamics on intellectual property value sharing frameworks.

Investors should monitor upcoming quarterly earnings releases alongside disclosed progress on cohort expansions providing tangible indicators beyond forward guidance absent specific financial forecasts from the company thus far [N3][S3].

Conclusion Overview

Entrada Therapeutics exemplifies an emerging biopharma investing heavily into novel intracellular delivery technologies addressing genetically defined rare diseases like Duchenne muscular dystrophy. While their proprietary EEV system demonstrates promise overcoming longstanding drug delivery barriers supported by regulatory designations—the company remains entrenched within a high-risk developmental phase marked by sizable recurring operating deficits.

Near-term developments center on clinical efficacy signals from multiple exon-skipping candidates with capital strategy crucial amid persistent negative cash flows. The complex regulatory landscape combined with commercial viability considerations underscore challenges common yet critical along this segment's path toward eventual product approval and market penetration.

Investors should weigh Entrada's innovative technological approach against traditional developmental uncertainties inherent in biopharmaceutical innovation pipelines without approved products or revenues established.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments