TORM plc’s Strategic Maneuvers Reflect Changing Dynamics in Product Tanker Shipping

An analysis of TORM’s financial shifts, fleet strategy, and capital management reveals its adaptation to evolving tanker market cycles.

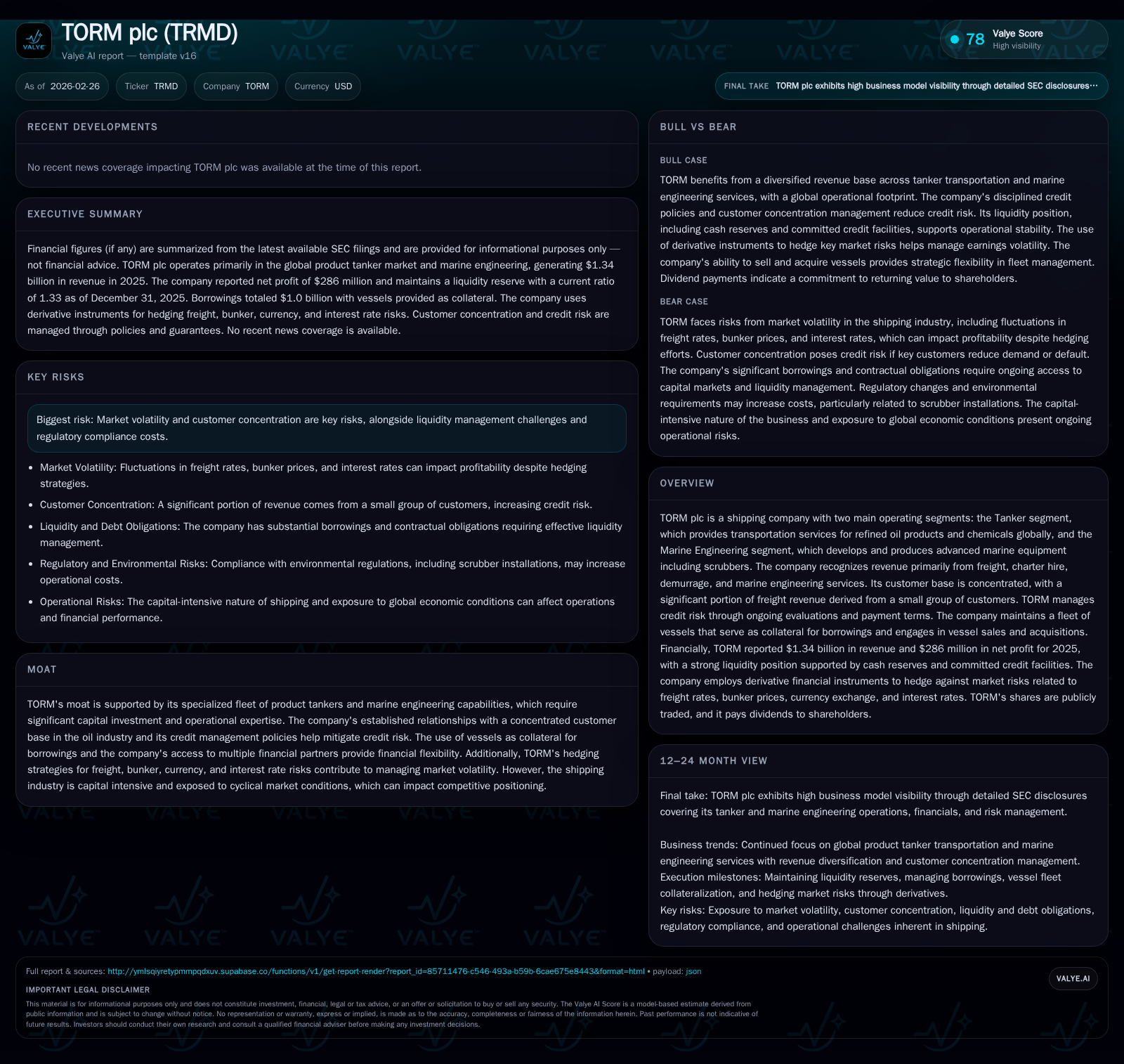

TORM plc reported stable revenue of approximately $1.34 billion in 2025 but experienced a significant 53% decline in net income to $286 million, reflecting challenging market conditions and operational factors. The company maintains a concentrated customer base requiring vigilant credit risk management. Fleet renewal efforts include repurchases and acquisitions of modern vessels alongside ongoing development in marine engineering technologies. TORM sustains robust liquidity with $163.5 million cash reserves and nearly $399 million in undrawn credit facilities, while managing debt reduction and moderating dividends to align with profitability pressures.

Steady Revenue Backdrop Amid Profitability Pressure

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | 286 | -53.2% |

| 2024 | 612 | -5.6% |

| 2023 | 648 | +15.2% |

| 2022 | 563 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 200 | 13.0 |

| 2024 | 553 | 29.5 |

| 2023 | 586 | 38.9 |

| 2022 | 167 | 37.4 |

Source: SEC companyfacts cache [F1].

TORM plc reported revenue of approximately $1.34 billion for the full year 2025, maintaining stability despite a marked decline in net income by roughly 53%, falling from $611.5 million in 2024 to $286 million in 2025 [F1][S3]. This divergence suggests margin compression likely due to softer freight rates and operational costs impacting profitability.

The balance sheet reflects sound short-term liquidity with a current ratio around 1.33 based on current assets of approximately $531.9 million against current liabilities near $401.4 million as of December 31, 2025 [F1].

Concentrated Customer Base Requires Rigorous Credit Management

TORM's revenue concentration remains notable, with one customer accounting for about 8% of freight revenues consistently over recent years [S14][S7]. This concentration necessitates robust credit risk management.

Established customers generally settle payments post cargo discharge, while newer or smaller clients provide upfront payment or bank guarantees. Historically, this approach has limited credit losses significantly [S7]. Demurrage claims represent around 12% of freight revenues but are recognized conservatively due to contractual disputes.

Fleet Renewal and Marine Engineering: Growth Drivers

The company has actively repurchased vessels previously under sale-and-leaseback arrangements during late 2025 and early 2026, including MR and LR2 class ships built in recent years (2018 and 2016) [S4]. This reflects a strategic focus on ownership for operational flexibility.

Marine Engineering continues developing emissions-reduction technologies such as scrubbers, supporting ancillary revenue streams beyond core tanker operations though these remain modest relative to total revenues [S14]. Integration of new vessels is expected through mid-2026.

Capital Structure Management: Debt Reduction and Liquidity Strength

Borrowings declined from about $1.23 billion at the start of 2025 to approximately $1.0 billion by year-end following repayments totaling around $568 million, partially offset by new borrowings of about $338 million [F1][S4][S12].

Vessel assets securing borrowings are valued near $2.79 billion including owned vessels plus those under financing structures treated as debt [S20]. The loan portfolio is diversified across around fourteen banks with no covenant breaches reported recently [S4][S7].

Liquidity includes cash balances of roughly $163.5 million plus nearly $399 million in committed undrawn credit lines providing financial flexibility [F1][S5][S16].

Dividend Policy Reflects Earnings Environment

Dividend payments fell substantially to approximately $199.7 million in fiscal year 2025 from over half a billion dollars paid previously ($553 million in 2024), aligning distributions with profitability trends [F1][S9][S13].

The company also canceled nearly half a million treasury shares due to compliance issues related to UK Companies Act distinctions between market and off-market purchases; this action did not affect shareholder rights or nominal capital value [S9].

Risk Mitigation Through Hedging and Credit Controls

TORM employs hedging strategies covering freight forward agreements (FFAs), bunker fuel price fluctuations, currency exposure consistent with its USD reporting currency, and interest rate risks typical for shipping finance [S1].

Credit evaluations complement tailored payment terms mitigating risks associated with a concentrated customer base where demurrage claims comprise material but uncertain revenue components.

Governance Changes Post-Hafnia Stake Acquisition

Following Hafnia Limited’s acquisition of approximately 14.2 million TORM A-shares representing nearly 14% ownership after the reporting period, special governance rights associated with Class B and C shares were extinguished leading to their redemption early in January 2026 [S4][S19]. This resulted in changes including the departure of the Deputy Chairman from the board.

Outlook: Key Milestones and Market Cycles Ahead

Important upcoming milestones include completion of vessel repurchases scheduled through mid-2026 impacting operational leverage.

Growth prospects depend on effectively scaling Marine Engineering innovations alongside navigating cyclical tanker market dynamics driven by global product demand and freight rate volatility [S3][S15]. Explicit financial guidance remains undisclosed.

This report synthesizes information solely from publicly available regulatory filings without offering investment advice. All cited figures are sourced explicitly from TORM plc disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments