trivago's Post-Acquisition Recovery Driven by Expedia Partnership and Brand Leverage

Steady revenue growth and modest profitability gains characterize trivago’s current phase as it integrates new assets and navigates governance complexities.

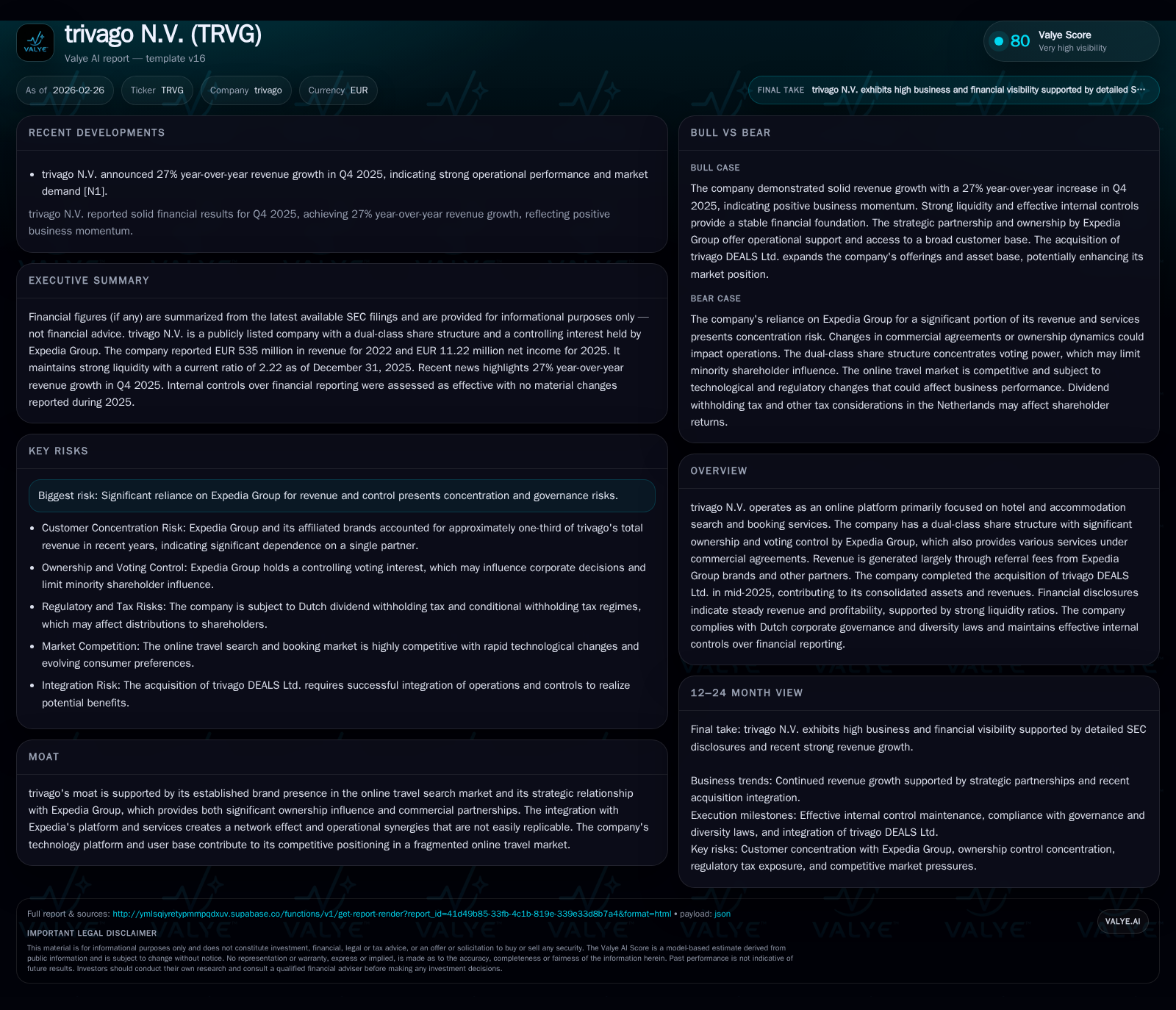

trivago N.V., an established online platform specializing in hotel and accommodation search, has shown marked revenue recovery in recent years following significant losses. The company’s strategic ownership and commercial ties with Expedia Group continue to underpin its market position and operational synergies. Despite modest profitability improvements and positive net income in 2025, challenges remain, including reliance on Expedia and governance risks inherent to its dual-class share structure. Investors should monitor continued integration of acquired assets and management’s capital allocation decisions as key future indicators.

Company Overview

trivago N.V. operates an online discovery platform specializing in hotel and accommodation search services. Its business model centers on generating referral fees primarily from Expedia Group brands alongside other partners. Expedia Group holds a controlling interest with significant voting leverage due to trivago’s dual-class share structure, a relationship that is foundational to trivago's operational model and market positioning [S1][S6][F1].

Historical Financial Performance and Drivers

The historical trajectory of trivago’s financials illustrates marked volatility caused by external shocks such as the pandemic and internal restructuring efforts. Revenue fell substantially from EUR 839 million at the end of FY2019 down to EUR 249 million by FY2020 due to travel industry disruption. However, from FY2020 through FY2022, revenue demonstrated robust recovery, rising almost twofold back up to EUR 535 million—a compound annual growth rate exceeding 40% during the rebound phase [F1].

Despite improving top line trends, operating income remained negative until FY2025. FY2025 marked the first full fiscal year with positive operating income of EUR 1.53 million, reversing prior years’ deep operating losses (e.g., -EUR 156.6 million in FY2023) [F1]. Correspondingly, net income swung from multi-year net losses (peak loss of -EUR 164.5 million in FY2023) to a positive figure of EUR 11.2 million in FY2025.

Operating cash flow exhibited contraction in the latest year—down nearly 62% to EUR 7.7 million—despite profit gains. Capital expenditure remains negligible (zero reported for FY2022 and FY2023), consistent with an asset-light digital platform model where investment primarily targets integrations rather than CAPEX-heavy infrastructure [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex | Net YoY |

|---|---|---|---|---|---|

| 2025 | 11 | 8 | 2 | +147.3% | |

| 2024 | -24 | 20 | -32 | +85.6% | |

| 2023 | -164 | 28 | -157 | 0 | -29.3% |

| 2022 | -127 | 66 | -120 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 5.3 | ||

| 2024 | 0 | -12.0 | |

| 2023 | 0 | 28 | -76.5 |

| 2022 | 20 | 66 | -22.6 |

Source: SEC companyfacts cache [F1].

*Equity figures show significant volatility reflecting balance sheet consolidation effects notably post-acquisition [F1].

Acquisition Impact and Strategic Partnerships

In July 2025, trivago completed the acquisition of trivago DEALS Ltd., adding a significant new component to its consolidated operations—approximately one-fifth of total revenues according to management disclosures [S1]. This expanded portfolio allows trivago to offer more competitive deals possibly enhancing user engagement metrics while leveraging its brand recognition.

The commercial symbiosis with Expedia Group remains central: Expedia's ownership exceeds half the equity (59%) but commands roughly four-fifths of voting power (84%), cementing control over corporate decisions [S6][S13]. This relationship brings both operational synergies—through shared technology, data hosting, and distribution channels—and concentration risks stemming from heavy dependency on a single major partner for referrals and revenues [S18][S28].

Industry Positioning and Moat

trivago's competitive advantage is chiefly anchored in its strong brand presence within a fragmented online travel marketplace alongside integration benefits accrued by collaboration with Expedia Group [S28]. The network effect from combining user traffic with Expedia-backed inventory bolsters pricing power and customer retention.

Technology-wise, trivago employs data-driven search algorithms with continuously enhanced UX design across platforms designed to optimize consumer decision-making efficiency—key in travel commerce where pricing transparency is vital.

However, as market fragmentation persists—with competition from direct booking platforms and OTAs—the moat depends substantially on maintaining these strategic alliances and innovation pace.

Governance & Regulatory Compliance

As a Dutch-incorporated entity listed with U.S reporting obligations via Form-20F filings, trivago adheres to Dutch corporate law frameworks including the Dutch Corporate Governance Code (DCGC), which introduces diversity target mandates for supervisory boards—requiring balanced gender representation—and recommends transparent director compensation disclosure protocols [S3][S4][S10].

The board currently reflects compliance progress but has not fully met gender diversity ratios mandated under the Dutch Diversity Act for management levels, presenting ongoing governance attention points.

Share Structure & Voting Control

'trivago's governance structure features a dual-class share system that confers ten votes per Class B share versus one vote per Class A share; Class B shares are predominantly held by Expedia Group and founders [S13]. This setup concentrates control notwithstanding minority economic ownership percentages.

Such arrangements complicate shareholder oversight particularly given past events where founder rights diminished below key thresholds affecting nomination powers—shifting control dynamics within supervisory board elections [S18].

Capital Structure & Liquidity Position

The company reports no outstanding debt instruments simplifying capital structure risk analysis; liquidity stands robust with current assets exceeding current liabilities by over twice (current ratio ~2.22 as of December 31, 2025) signifying sound short-term financial resilience [F1][S16][S19]. Cash position details note sizeable reserves sufficient for operational needs amid ongoing integration efforts.

Returns Analysis & Capital Allocation Policy

ROE calculated from FY2025 figures is modest at approximately 5.3%, reflecting early-stage profitability turnaround after prolonged loss periods [F1]. Operating cash flow contraction juxtaposed against rising net income may suggest working capital or non-cash adjustments impacting cash conversion.

Historically, trivago has not engaged significantly in share repurchases post-IPO era latest years showing zero buybacks since FY2022 [F1][S7]; no dividends have been declared recently likely preserving liquidity for operational investments including acquisitions like trivago DEALS Ltd.

Future capital allocation is expected to prioritize strategic growth investments aligned with global travel market recovery trajectories while balancing potentially shareholder-friendly returns once stable profit streams consolidate.

Future Outlook Considerations (Analysis)

Explicit future guidance remains limited in public disclosures; however key watchers should include:

- Integration success around acquisition assets impacting revenue retention/growth,

- Continuing evolution of the partnership framework vis-à-vis Expedia including referral fee structures,

- Market share gains amid recovering global travel demand,

- Further cost management impact on margins given platform scalability,

- Potential governance shifts given evolving shareholder structures.

The ongoing COVID-related travel resumption momentum offers tailwinds but also invites competitive intensity escalation requiring vigilance.

Risks Summary from Filings

- Heavy dependence on Expedia Group constrains independence and exposes trivago to counterparty risks if strategic alignment diverges [S12][N1].

- Regulatory compliance complexity due to multinational operations including tax withholding nuances on dividends [S1].

- Governance challenges posed by concentrated voting power raise questions over minority shareholder protections [S20].

- Cybersecurity risks are acknowledged but have been actively managed without material incidents recently [S14][S17].

Conclusion

trivago has transitioned from a value-eroding phase into initial profitability supported by strategic acquisitions and deep partnership ties primarily with Expedia Group that fuel revenue growth and brand leverage amid an emerging post-pandemic travel recovery scenario. Maintaining this trajectory will require measured capital allocation focused on organic innovation blended with selective acquisitions while managing concentration risks embedded within its ownership structure. Investor focus should remain on how integration proceeds along with margin trends over upcoming reporting periods beyond February Q4 earnings announcement reflecting continued fundamental shifts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments