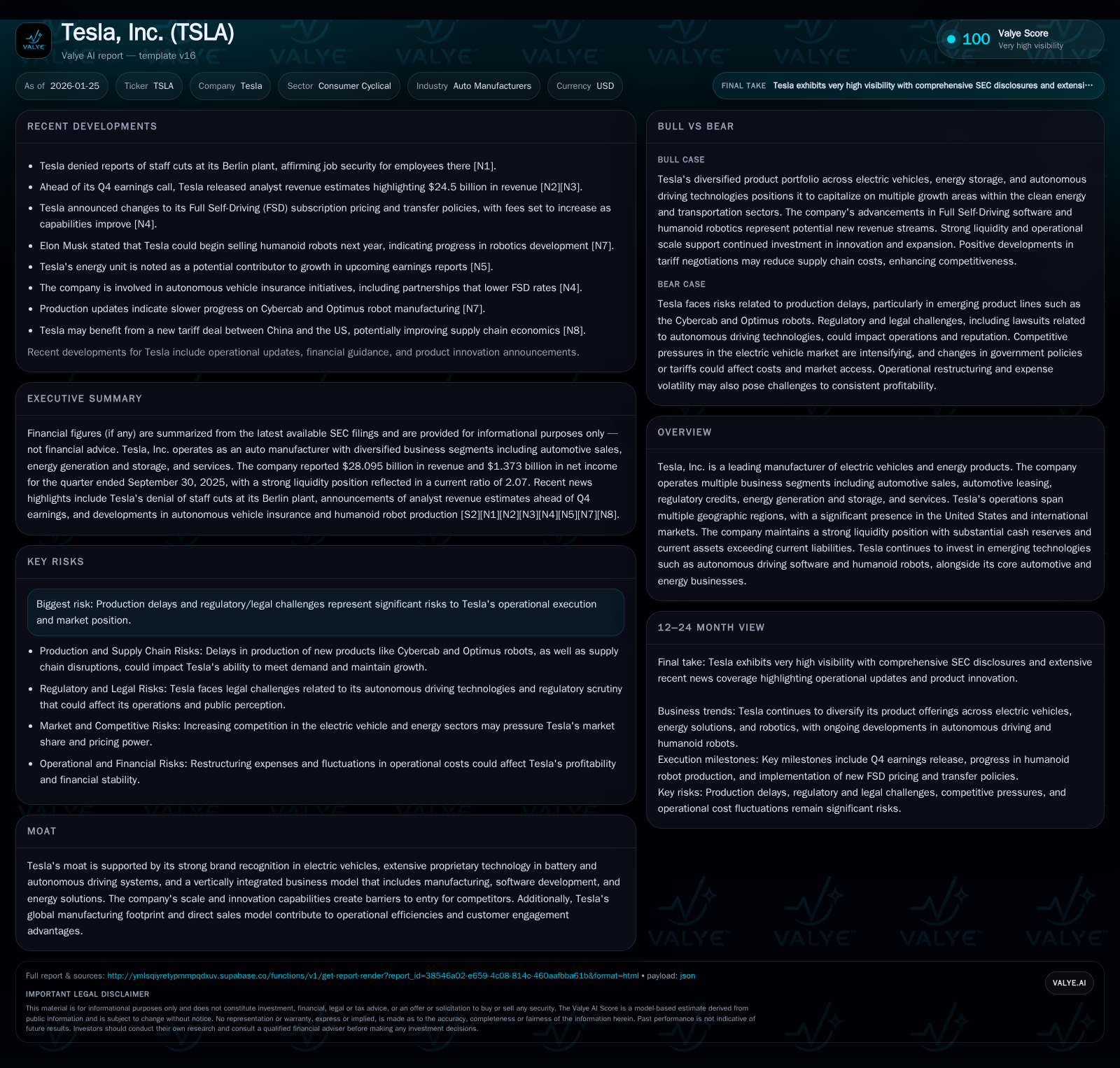

Tesla Inc.: Navigating EV Leadership Amid Operational and Market Complexities in Early 2026

Tesla maintains its leadership in electric vehicles and energy solutions while facing evolving supply chain and competitive challenges.

Tesla continues to leverage its vertically integrated business model and strong brand positioning across automotive and energy segments. Recent analyst estimates highlight robust revenue expectations ahead of Q4 2025 earnings, though concerns persist around profitability pressures and operational execution, notably in its Berlin facility. Tesla’s expansion into autonomous driving and robotics remains a strategic focus, with global manufacturing scale and proprietary technologies underpinning its competitive moat. However, supply chain constraints, regulatory scrutiny, and short-seller activity underscore the complexity of its near-term outlook.

What Changed Recently

In the weeks leading into Tesla’s Q4 2025 earnings release, the company publicly shared analyst estimates projecting revenue around $24.5 billion, signaling continued strong sales momentum [N1][N2]. Despite this upbeat top-line outlook, earnings previews suggested potential declines in profitability, with some market participants expressing caution [N6][N7]. Adding to the complex sentiment, Tesla faced persistent short-seller interest, with put options activity indicating ongoing bearish bets ahead of earnings [N3].

Operationally, Tesla refuted claims of substantial workforce reductions at its Berlin Gigafactory, clarifying that jobs there remain secure despite media reports of a 1,700-person cut [N11]. This episode underscores the challenges Tesla faces in managing ramp-ups at new facilities amid global economic and supply chain fluctuations.

Further, geopolitical developments such as a nascent tariff agreement between China and the U.S. may favor Tesla’s supply chain and cost structure, given its significant manufacturing presence and sales exposure in both markets [N9]. On the supplier side, Tesla’s extension of graphite supply deals with Syrah Resources highlights the company’s proactive approach to securing critical battery raw materials [N10].

Lastly, the company’s broader innovation ambitions in AI and robotics continue to generate market interest, with analyst commentary noting the strategic importance of robotaxi and humanoid robot projects for Tesla’s future growth trajectory [N13].

Business Model as a System

Tesla operates a vertically integrated business combining automotive manufacturing, energy generation and storage, software development, and services. The automotive segment dominates revenues, comprising vehicle sales and leasing operations. Tesla’s direct sales model bypasses traditional dealership networks, enabling closer customer engagement and pricing control [S1][S2].

The energy segment includes solar energy products and energy storage solutions, addressing both residential and commercial customers. Leasing and regulatory credits supplement revenue streams, the latter being a key profitability lever given evolving emissions regulations [S1][S3].

Tesla’s proprietary technology stack spans battery cell chemistry and production, electric drivetrain components, and autonomous driving software. The company’s FSD (Full Self-Driving) software and AI initiatives form an increasingly important part of its service offerings and potential recurring revenue.

Capital intensity is high, with significant ongoing investments in gigafactory construction, R&D for battery and vehicle innovations, and software platform development. Tesla’s balance sheet reflects substantial liquidity, supporting these capital needs while maintaining operational flexibility [S16].

Geographically, Tesla operates globally with major manufacturing hubs in the U.S., China, and Europe, exposing the company to diverse regulatory environments and supply chain complexities [S2][N9].

Industry Map & Competitive Battlefield

The electric vehicle landscape has rapidly evolved from a nascent niche to a fiercely contested mainstream market. Tesla remains a leading player by volume and brand recognition but faces intensifying competition from established automakers (e.g., Volkswagen, GM, Ford) accelerating their EV transitions, and from new entrants focused on affordability and regional markets.

Battery technology and supply chain control are key battlegrounds. Tesla’s investment in proprietary battery cells and vertical integration provides a cost and performance edge, but raw material constraints and supplier negotiations (e.g., graphite and lithium sourcing) remain critical vulnerabilities [N10][S8].

On the software and autonomous driving fronts, Tesla’s approach diverges from traditional OEMs by developing in-house AI systems and leveraging fleet data. This has fueled leadership claims but also regulatory scrutiny and technical challenges, especially around safety and validation of FSD capabilities [Valye overview].

Energy products and storage position Tesla at the intersection of automotive and renewable energy markets, competing with incumbents like Enphase and Sunrun in solar, as well as battery storage providers. This diversification helps mitigate cyclicality inherent in automotive sales but also requires managing different sales channels and customer types.

Tesla’s global manufacturing footprint is both a strength and a complexity driver, requiring deft navigation of geopolitical tensions, tariffs, and local regulations. The recent potential tariff relief between China and the U.S. could alleviate cost pressures and enhance competitive positioning in these critical markets [N9].

Where the Economics Become Real

Tesla’s unit economics are fundamentally tied to battery costs, manufacturing scale, and direct sales margins. Battery pack cost reductions have been a major margin driver historically; however, raw material price volatility can quickly erode these gains [S8][S9]. Securing long-term supply contracts for key materials like graphite is therefore essential to sustain cost advantages [N10].

Manufacturing efficiency improvements at gigafactories aim to increase throughput and lower per-unit fixed costs. However, disruptions or inefficiencies—such as the reported staffing concerns at Berlin—can materially impact margin trajectories [N11].

Revenue from regulatory credits has historically bolstered profitability but is subject to regulatory changes and competitor credit generation. Tesla’s ability to maintain or grow this income stream is uncertain and increasingly competitive.

The software and services segment, including FSD subscriptions and future robotaxi services, represents a high-margin revenue opportunity but requires substantial upfront investment and regulatory approval. The timing and scale of profitability in this area remain unclear.

Tesla’s liquidity position, with over $18 billion in cash and equivalents and a current ratio above 2.0, provides cushion to absorb operational shocks and fund strategic initiatives [S16]. Capital expenditures and R&D spending remain significant, reflecting the company’s growth ambitions and the capital-intensive nature of automotive and energy product development [S14].

Diligence Questions / Disconfirming Signals

- What is the true operational status and ramp efficiency of the Berlin Gigafactory following the recent staffing controversy? How might this impact production volumes and costs?

- How sustainable are Tesla’s regulatory credit sales in the medium term, particularly as competitors increase their zero-emission vehicle output?

- To what extent can Tesla mitigate raw material supply risks and price volatility, especially for battery-critical minerals like graphite and lithium?

- How realistic are near-term revenue and margin contributions from autonomous driving software subscriptions and robotaxi deployments?

- What regulatory or legal hurdles could materially impact Tesla’s product offerings or market access, given ongoing scrutiny in multiple jurisdictions?

- How might intensified competition from legacy automakers with deeper pockets and established dealer networks affect Tesla’s market share and pricing power?

- Is the current level of short-seller interest indicative of structural concerns in Tesla’s growth narrative or just market sentiment volatility?

This analysis incorporates publicly available news coverage and SEC-extracted company disclosures to provide a comprehensive understanding of Tesla’s business dynamics as of early 2026. It is intended for informational purposes and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments