Growth Drivers and Capital Allocation Shape United Community Banks’ Outlook in Southeastern Banking

United Community Banks combines regional expansion with prudent capital measures to sustain growth amid regulatory and competitive challenges.

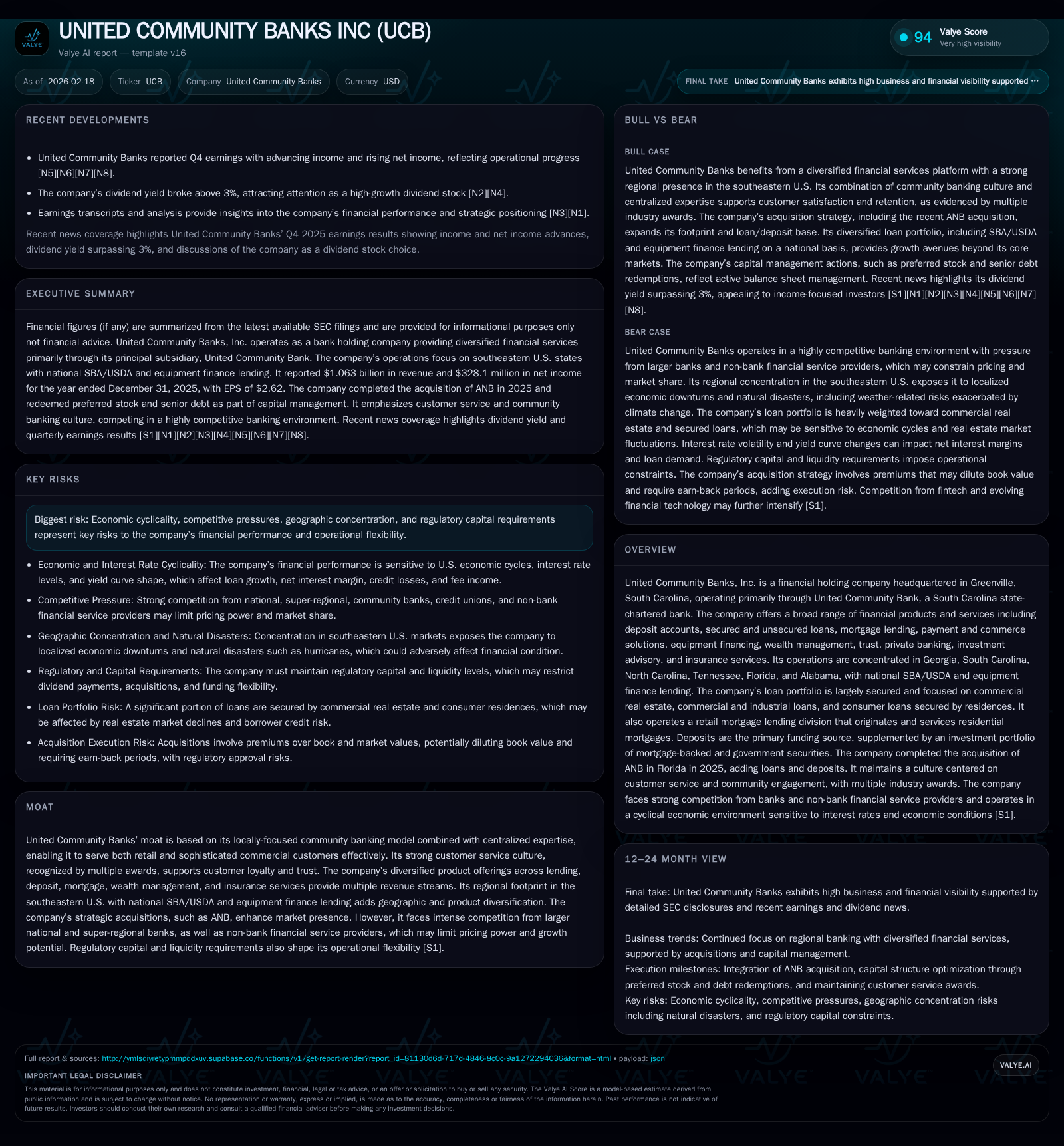

UNITED COMMUNITY BANKS INC (UCB) has driven significant growth through strategic acquisitions, notably the ANB deal in Florida, complemented by solid organic expansion across its Southeastern U.S. footprint. The bank's hybrid community banking model leverages localized customer engagement alongside centralized commercial expertise, supporting a diversified lending portfolio and robust fee income from mortgage, SBA/USDA, and wealth management services. Proactive capital management, including redeeming preferred stock and retiring senior debt during 2025, has enhanced balance sheet flexibility, enabling a rise in dividends and the resumption of share buybacks. However, regulatory constraints and intensifying competition from larger institutions and fintech disruptors continue to shape operational risks and growth capacity.

The Local Banking Model Backed by Centralized Expertise

United Community Banks (UCB) operates a distinctive hybrid business model that marries focused community banking with centralized commercial product expertise [S1][S4][N1]. Rooted deeply in six Southeastern states—Georgia, South Carolina, North Carolina, Tennessee, Florida, and Alabama—the company leverages local market advisory boards to maintain close client relationships while delivering advanced commercial banking solutions through a centralized Commercial Banking Solutions unit. This configuration enables nuanced deposit gathering tailored to local preferences alongside sophisticated middle market CRE lending and treasury product offerings [S4]. Industry terms like "deposit betas" and "market advisory boards" are integral to articulating UCB's ability to balance retail responsiveness with back-office efficiency.

The bank’s cultural emphasis on “The Golden Rule of Banking” underpins its repeated recognition by J.D. Power for customer satisfaction across the Southeast—a crucial moat against intensifying competition [S12]. This model supports diverse clientele from retail customers to complex commercial borrowers requiring SBA or USDA guaranteed loans.

Record Growth in 2025: Drivers and Strategic Acquisition Impact

In FY2025, UCB posted revenue of approximately $1.06 billion—an impressive 18% increase over FY2024's $901 million—with net income rising a robust 30% to $328 million [F1][N2][S4]. This surge reflects both organic loan portfolio expansion and the May 1 acquisition of ANB in Florida contributing $301 million in loans and $374 million in deposits [S1][N2]. The acquired assets represent roughly 2–3% of consolidated assets but have accelerated regional footprint growth in the Fort Lauderdale metropolitan area.

The core loan book remains concentrated on owner-occupied CRE projects and commercial & industrial equipment financing which together accounted for nearly three-quarters of total loans as of year-end [S6][N2]. SBA/USDA lending nationwide remains a critical growth vector due to its partial government guarantees enabling competitive risk-based pricing.

This balanced contribution of acquisition-related volume plus steady organic credit expansion has boosted fee income streams particularly from the mortgage segment where over $1 billion in residential loans were originated in FY2025 [S6][N3]. Loan seasoning quality indicators such as ACL coverage remain stable even amid economic cyclicality concerns.

Evolving Product Mix Fueling Revenue Expansion

UCB’s product breadth extends beyond traditional lending into mortgage origination/sales (with servicing retained for most mortgages sold), equipment financing, wealth management via United Community Private Wealth division, insurance through United Community Insurance Inc., plus payment processing capabilities via its merchant services joint venture UCPS with Clover/Fiserv [S8][N3]. These complementary fee sources stabilize revenues against fluctuating interest rate environments common in banking.

Interest rate sensitivity is partially mitigated by diversified lending mix incorporating adjustable-rate CRE loans alongside fixed-rate mortgages sold into secondary markets without recourse—an important shift minimizing duration risk [S6]. Fee income from SBA/USDA loan guaranties enhances margins via origination fees distinct from pure interest income. Cross-selling opportunities leveraging wealth management products deepen client wallet share while boosting noninterest income streams.

This product evolution positions UCB competitively though it requires continuous technological investments and effective integration of newly acquired businesses’ systems—critical given rapid sector innovation [N3].

Capital Management: Redeeming Preferred Stock and Debt Reduction

In line with its disciplined capital allocation policy, UCB executed redemption of its Series I preferred stock valued at $88.3 million on September 15, 2025 [S1][N3], reducing low-cost capital instruments that carry dividend obligations potentially dilutive over time. Simultaneously during 2025, the bank redeemed all outstanding senior debentures totaling $135 million [S1], effectively lowering interest expense and deleveraging the balance sheet position.

These steps reflect active management within regulatory capital tiers—particularly Common Equity Tier 1 (CET1)—to optimize capital while maintaining well-capitalized status per Basel III standards [S11]. Managing book value dilution through these redemptions aligns with expected earn-back periods supported by increased earnings power post-acquisition.

Such proactive balance sheet optimization supports sustainable credit growth without raising additional external equity or subordinated debt prematurely—a key strategy given volatile regulatory climates restricting dividend payouts or share repurchases if capital thresholds slip [S7].

Dividend Growth and Share Repurchases: Returns to Shareholders

Dividend distributions showed an upward trajectory from $112 million in FY2024 to roughly $118.5 million cash dividends in FY2025—an increase near 11.8% consistent with improving profitability [F1][N6]. Notably, UCB resumed share repurchase activity after a multi-year hiatus with total buybacks amounting to approximately $44.3 million in FY2025—the first since FY2021—signaling restoration of capital flexibility.

Dividend yield expansion accompanied this move, supported by stable payout ratios reflective of earnings retention policies permitting reinvestment for growth while rewarding shareholders [N7]. Timing of repurchases appears opportunistic amid share price valuations attractive relative to tangible book value backing.

These shareholder return programs balance prudent capital retention against investor demands for sustainable returns within regulatory constraints that can arise if capital adequacy weakens [S20].

Managing Regulatory Constraints and Competitive Pressures

UCB operates under a complex matrix of federal and state regulations affecting everything from permissible activities to capital requirements [S1][S5][S13]. Maintaining CET1 ratios above minimums mandated by Basel III along with buffers is critical for unrestricted dividends or buybacks [S10]. Compliance burdens elevate operating costs while limiting rapid scale-up potential—especially when considering mandatory stress testing outcomes required by regulators.

Competition intensifies from national banks with deeper pockets able to extend larger credit lines or offer broader digital platforms unavailable at community levels [S21][S22]. Additionally, fintech entrants capitalize on reduced regulatory oversight presenting cost-efficient alternatives challenging traditional deposit-gathering mechanisms. Such dynamics compress net interest margins (NIM) via pricing pressure.

Regulatory-induced ROE compression remains salient as well; balancing loan loss reserves (ACL) versus earnings quality necessitates stringent credit monitoring frameworks ensuring coverage aligns tightly with evolving economic forecasts without excessive provisioning dampening profits [S19][S13].

Organic Growth Initiatives and Market Expansion Prospects

Looking forward, UCB prioritizes organic expansion strategies focusing on incrementally increasing branch presence within existing Southeastern markets supported by technology-enhanced remote banking options attracting younger demographics [N5][S21]. Expanding national SBA/USDA loan pipelines leverages government guarantees fostering less risky credit extension while addressing small/mid-size business needs beyond immediate geographies.

Enhancement of CRE lending partnerships aims at gaining market share segments resilient amid economic cycles but subject to seasonal variation requiring adept monitoring via market advisory boards tied closely with underwriting expertise [S4][N5]. Talent retention remains essential given scaling complexities—a factor highlighted by management discussions emphasizing recruitment alongside training balanced against evolving technological infrastructure deployments.

Constraints emanate predominantly from competitive pressures limiting pricing power plus heavier regulatory scrutiny potentially delaying new product rollouts or geographic licenses needed for branch expansions [N5][S21]. Thus achieving profitable growth will depend upon effectively leveraging differentiated service cultures combined with scalable operational backbones.

Key Milestones to Watch in Capital Adequacy and Earnings Quality

Stakeholders should track upcoming quarterly disclosures focusing on CET1 ratio trajectories vis-à-vis evolving RWA calculations under stress scenarios per Basel III regimes [N1][N2][S1]. Expense synergies realization post-ANB integration will clarify cost control effectiveness essential for margin improvement amid inflationary salary pressures.

Loan loss provision trends remain an important early indicator of asset quality shifts relevant for both regulator comfort levels and investor confidence given cyclical sensitivities intrinsic to CRE-heavy portfolios [N2][S13]. Monitoring payout ratio adjustments aligned with dividend safety plus evaluating share repurchase pacing relative to market valuation provide insights into capital return sustainability.

Operational execution milestones include advancing payment systems joint ventures like UCPS delivering merchant services—potential incremental drivers of noninterest revenue—and technology platform upgrades supporting cross-selling efficiency enhancements across wealth management channels [N1].

Financial Performance Snapshot: Revenue, Net Income, Cash Flows, Dividends & Buybacks,

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1063 | 328 | 384 | 28 | +18.0% | +30.0% |

| 2024 | 901 | 252 | 350 | 47 | +12.1% | +34.6% |

| 2023 | 804 | 188 | 294 | 72 | -2.7% | -32.4% |

| 2022 | 826 | 277 | 607 | 43 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 119 | 44 | 356 |

| 2024 | 112 | 303 | |

| 2023 | 105 | 0 | 221 |

| 2022 | 87 | 0 | 565 |

Source: SEC companyfacts cache [F1].

- YoY figures calculated excluding missing data years; Buybacks data meaningful only post-2020.

Operating income data is not available from the provided tags; thus it is excluded here. The table highlights strong topline acceleration paired with disciplined cash flow fundamentals despite sharply reduced capex intensity indicating effective cost control. Approximately a ~9% ROE reflects balanced profitability intersecting growth investments with mindful leverage amidst rigorous risk-weighted asset management strategies.

Disclaimer: This report is informational only and does not constitute investment advice or recommendations regarding UNITED COMMUNITY BANKS INC (UCB). All financial data are sourced from SEC filings ([F1], [S#]) and public news outlets ([N#]) cited accordingly. Readers should perform independent due diligence before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments