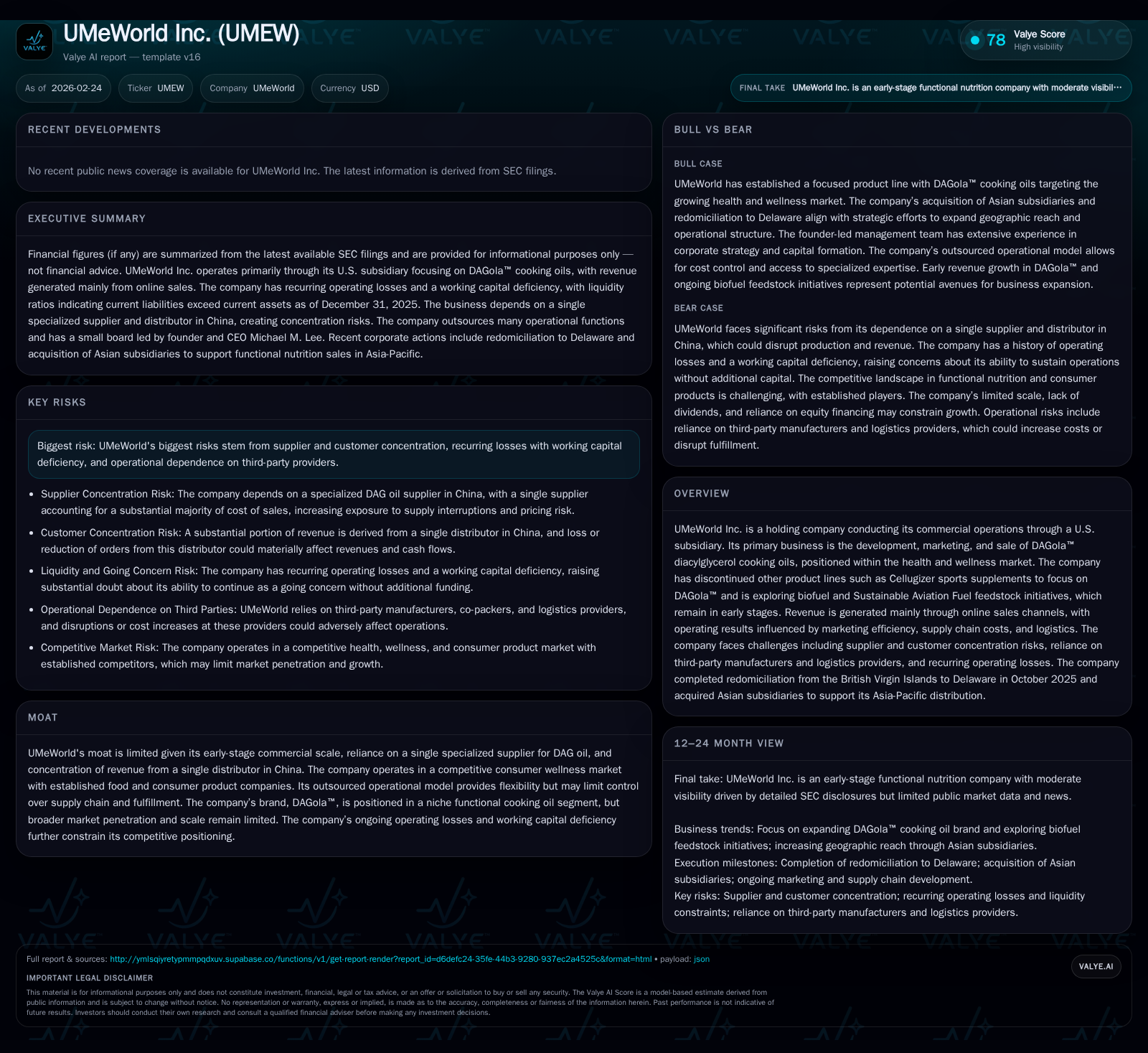

UMeWorld Inc. Expands DAGola™ Brand Amid Supply and Customer Concentration Challenges

The company advances its niche wellness oils business while facing operational and financial constraints tied to concentrated suppliers and customers.

UMeWorld Inc. operates primarily through the U.S. subsidiary that markets the DAGola™ diacylglycerol cooking oil, targeting a health-conscious consumer segment. The company has sharply pivoted away from sports supplements to focus exclusively on DAGola™, achieving revenue growth exceeding 136% in fiscal 2025 though still at an early commercial scale with persistent losses. Its business model heavily depends on a single specialized supplier in China and one major Chinese distributor, exposing it to supply chain and customer concentration risks which pressure margins and operational stability. UMeWorld also explores biofuel and Sustainable Aviation Fuel feedstock initiatives that remain nascent with no revenue contribution. Liquidity challenges persist as working capital deficits continue, necessitating equity raises without dividend or buyback programs. Marketing efficiency and online retail economics remain vital drivers of revenue expansion amid elevated fixed costs.

Evolution of UMeWorld's Revenue Streams: The Rise and Challenges of DAGola™

UMeWorld Inc., operating through a U.S.-based subsidiary, has strategically repositioned its commercial efforts around the DAGola™ brand, a functional diacylglycerol cooking oil designed for the health and wellness market [S1]. This focus intensified after exiting its Cellugizer sports supplements business during fiscal 2025, marked by a full inventory write-off reflecting management’s prioritization of scalable products within functional nutrition.

Financial data reveals a pronounced rebound in revenue generation from this pivot: revenues increased from a modest $941,000 in FY2024 to $2.22 million in FY2025, representing a robust growth rate of approximately 136% year-over-year [F1]. Despite this top-line gain, total revenues remain limited, characteristic of early-stage commercialization where brand awareness and distribution breadth are still developing.

Sales occur predominantly via online retail channels, which require managing digital advertising spend, optimizing customer acquisition cost (CAC), and navigating platform-specific fulfillment charges [S1]. Given these dynamics, revenue volatility is expected as the company scales distribution and refines marketing efficiency.

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2222 | -258176 | -113946 | -258218 | +136.1% | -15.0% |

| 2024 | 941 | -224465 | -30072 | -224465 | -32.8% | +26.7% |

| 2023 | 1401 | -306340 | -66848 | -306340 | ||

| 2021 | 2832 | -107436 | -120144 | -103657 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 79.7 | |

| 2024 | 61.4 | |

| 2023 | -66848 | 81.5 |

| 2021 | -140831 | 52.0 |

Source: SEC companyfacts cache [F1].

Note: Capex values are unavailable for recent years except FY2023 and FY2021 [F1].

Supplier and Customer Concentration: Impact on Margins and Operational Stability

A significant risk factor for UMeWorld lies in its reliance on a single specialized supplier in China for its DAG oleaginous raw material [S2][S5]. This supplier accounted for a substantial majority of the company's cost of sales as of the quarter ended December 31, 2025 [S2]. The technical complexity involved in producing DAG oil restricts alternative sourcing options, increasing exposure to supply disruptions or pricing volatility.

On the customer side, a substantial portion of revenues is derived from one major distributor in China [S2][S5], intensifying concentration risk. While this channel aids market penetration in Asia-Pacific, dependence on a single large buyer introduces potential vulnerability if order volumes or pricing terms change unfavorably.

Additionally, UMeWorld relies on third-party manufacturers, co-packers, and logistics providers whose service interruptions or capacity constraints could elevate costs or disrupt fulfillment [S2][S5].

Strategic Pivot into Sustainable Aviation Fuel Feedstocks: Promise Versus Reality

UMeWorld has initiated exploratory efforts into biofuel and Sustainable Aviation Fuel (SAF) feedstock development as part of a strategic diversification beyond consumer nutrition products [S1]. These projects remain at early planning stages without generating revenue during the fiscal year ended September 30, 2025 [S1]. Their realization involves technological validation and market entry risks over uncertain timelines.

Financial Results Snapshot: Operating Losses and Cash Flow Dynamics

The company reported a net loss of approximately $258K for fiscal year 2025 with an operating loss close to the same amount [F1], reflecting challenges typical for an early-stage consumer brand scaling operations. Operating expenses included marketing outlays, administrative costs related to public company compliance, and a non-cash inventory write-off of $29K associated with discontinuing the Cellugizer product line [S9].

Operating cash flow remained negative at about $114K in FY2025 [F1], signaling ongoing capital requirements to support growth initiatives prior to reaching sustainable profitability.

Capital Structure and Liquidity: Navigating Persistent Working Capital Deficits

As of September 30, 2025, UMeWorld reported a working capital deficit near $324K compared to $366K at the prior fiscal year-end [F1][S4][S6]. Cash balances were approximately $154K following interim periods ending late 2025 [S4], but current liabilities exceeded current assets yielding a current ratio around 0.79.

The company continues to finance operations primarily through equity issuances and shareholder advances with expectations for additional funding needs amid ongoing losses and expansion plans [S4][S6][S13]. Dividend payments or share repurchases have not been made nor planned given the priority on conserving liquidity [S12][S15].

Marketing Efficiency and Online Channel Economics as Drivers of Growth

UMeWorld’s revenue generation hinges largely on online retail channels where marketing spend efficiency critically influences customer acquisition costs (CAC), platform commissions, fulfillment fees, and ultimately gross margins [S1]. Fluctuations in digital advertising effectiveness or e-commerce platform algorithms can materially impact sales volumes given the nascent scale of DAGola™’s market presence.

Governance and Leadership Continuity in an Early-Stage Enterprise

Leadership is anchored by founder Michael M. Lee who has served as Chairman and CEO since inception in 1997 bringing over three decades’ experience across technology development, corporate strategy, marketing innovation, and cross-border finance involving Asian markets [S1][S20].

Winfield Yongbiao Ding serves as CFO with credentials including MBA and Chartered Accountant designation contributing seasoned financial oversight suited to small-cap public companies transitioning regulatory compliance frameworks [S1][S20].

The Board includes long-tenured independent directors providing governance stability despite absence currently of formal nomination or compensation committees typical at larger firms [S15][S19]. An audit firm transition occurred early calendar year 2026 reflecting efforts to strengthen internal controls following identified material weaknesses [S3][S16][S20].

This analysis is based solely on publicly available SEC filings up to February 24, 2026 including detailed financial statement data from XBRL tags [F1] without extrapolation or assumptions beyond disclosed facts. Metrics such as dividends paid or share buybacks were not available from provided data sources. Readers should consider inherent risks associated with early-stage commercialization reliant on concentrated suppliers/customers within competitive wellness markets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments