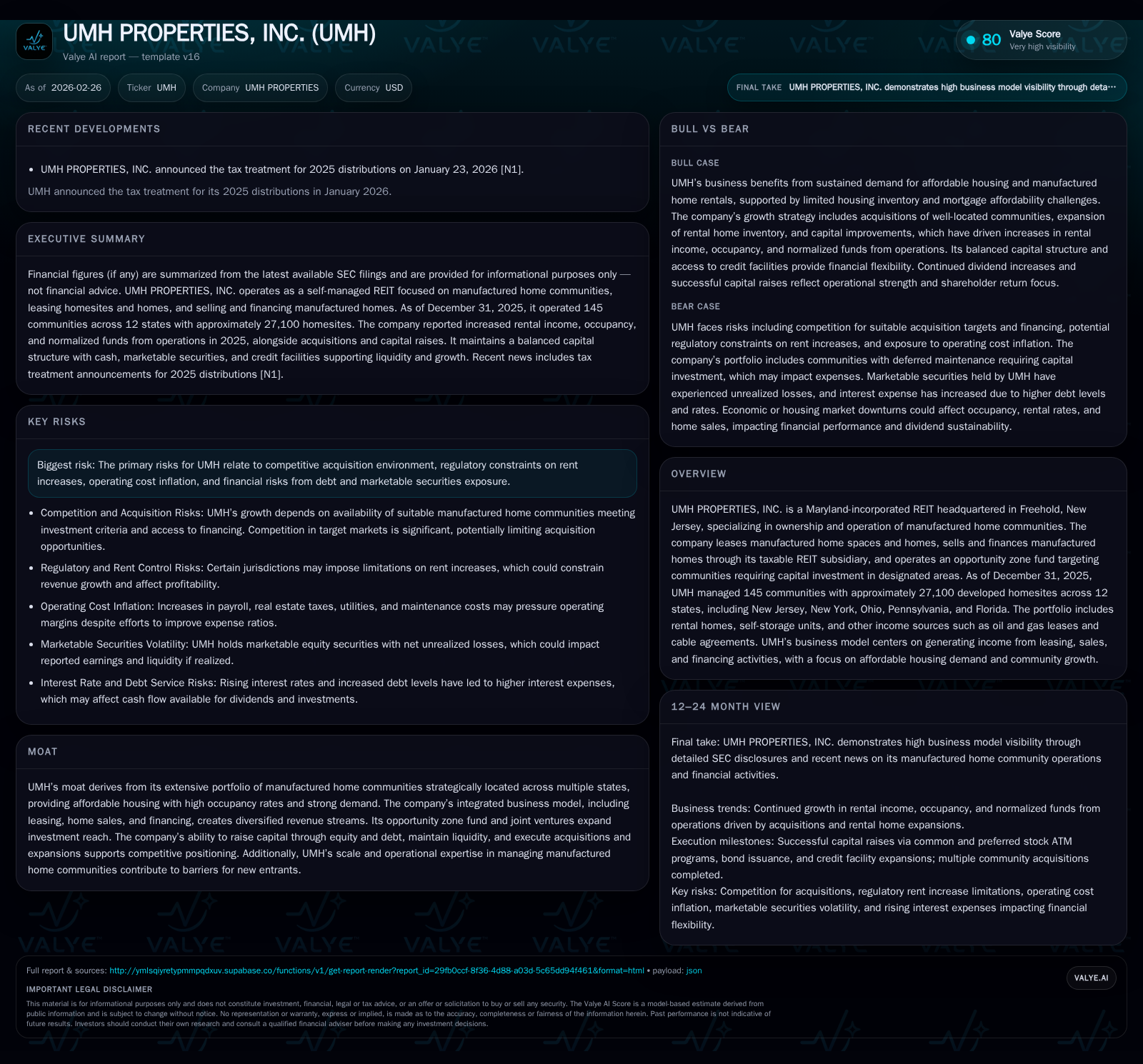

UMH Properties Drives 2025 Performance with Diversified Manufactured Housing Assets

UMH Properties achieved solid 2025 growth through integrated leasing, sales, and financing within an expanding manufactured housing portfolio supported by active capital market engagement.

In 2025, UMH Properties leveraged its diversified manufactured home community assets to deliver revenue growth, improved operating margins, and robust cash flow generation. Strategic acquisitions and expansions increased portfolio scale while disciplined capital raising enhanced liquidity and financial flexibility. Cost-efficiency gains combined with strong occupancy rates bolstered net operating income, supporting incremental normalized funds from operations per share. The company maintained a balanced approach to dividends and share repurchases aligned with cash flow, navigating regulatory and inflationary challenges while accessing multiple capital channels for growth.

From Incremental Gains to Momentum: UMH’s Historical Growth Journey

UMH Properties steadily built momentum heading into its latest fiscal year, reflecting strategic execution within the affordable housing niche of manufactured home communities. Revenue climbed by nearly 9% in 2025 to reach $261.75 million from $240.55 million in 2024 [F1], fueled primarily by rental rate increases and higher occupancy levels across its sprawling portfolio. These gains were further underpinned by a meaningful uptick in sales of manufactured homes.

Net Operating Income (NOI) from the community segment rose by approximately 9%, mirroring similar same property NOI growth as UMH optimized operational efficiencies amidst rising demand [S1]. Occupancy improvements were notable as well — same property occupancy rose by 80 basis points to 88.3%. Concurrently, the company trimmed its same property expense ratio modestly from 39.7% to 39.3%, reflecting prudent cost controls even as payroll and utility expenses showed moderate inflationary pressure [S1].

Normalized Funds From Operations (FFO), a key REIT performance metric excluding certain non-cash charges and unusual items, increased a robust 15% during the year while FFO per diluted share gained 2%, reaching $0.95 per share — signaling effective operational leverage translating into shareholder returns without excessive dilution [S1].

Historical performance (annual)

| FY | Rev ($mm) | CFO ($mm) | Rev YoY |

|---|---|---|---|

| 2025 | 262 | 82 | +8.8% |

| 2024 | 241 | 82 | +8.9% |

| 2023 | 221 | 120 | +12.8% |

| 2022 | 196 | -8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) |

|---|---|

| 2025 | 5 |

| 2024 | |

| 2023 | |

| 2022 | 0 |

Source: SEC companyfacts cache [F1].

Note: Net income figures for recent years were not consistently available; hence omitted here.

Diverse Revenue Streams: Leasing, Sales, and Financing Synergies

UMH’s integrated business model blends leasing of manufactured home sites and homes with direct home sales and financing through its taxable REIT subsidiary, creating a resilient mix that cushions against sector cyclicality.

Leasing delivers foundational recurring revenue buoyed by sustained occupancy gains and rental rate adjustments where regulatory frameworks permit incremental rent escalations within periodic limits [S1]. This rental yield enhancement is critical given the annual or monthly lease terms prevalent in site leases.

Home sales revenue grew modestly by about 4%, reflecting healthy demand for affordable home ownership facilitated by favorable financing terms proprietary to UMH’s platform [S16]. Gross margin on sold homes improved slightly due to better cost control despite flattening conventional housing prices nationally.

Financing activities generate spread income on notes receivable that grew alongside higher loan balances paralleling additional home sales; UMH’s average note receivable balance was reported around $83.9 million in prior years with weighted average loan yields near 7% [S20].

Ancillary income streams including self-storage leases within communities, cable service agreements, and oil & gas leases diversify earnings but remain smaller contributors relative to core manufactured housing operations.

Capital Market Engagement and Liquidity Positioning in 2025

UMH advanced a multifaceted capital strategy across debt and equity markets to underpin growth while preserving financial flexibility for opportunistic acquisitions and expansions.

The year featured two additions totaling seventeen communities added to its Fannie Mae credit facility—loans aggregating nearly $193 million with fixed interest rates between approximately 5.46% and 5.855%, structured as interest-only over nine- to ten-year terms before principal maturity dates extending into the early-to-mid-2030s [S9][S26][S27]. These long-dated fixed-rate loans support predictable financing costs conducive to steady cash flow coverage.

Equity issuance through at-the-market (ATM) sale programs contributed over $44 million in gross proceeds from common stock offerings priced on average near $17.59 per share along with roughly $2 million raised via preferred stock ATM issuances [S4][S8][S9]. This continuous-access equity approach complements internally generated funds such as those accrued through a Dividend Reinvestment Plan (DRIP), which brought in nearly $9.3 million including reinvested dividends.

Additionally, UMH issued approximately $80 million aggregate principal amount of Series B bonds carrying a coupon rate of 5.85%, maturing in five years — marking diversification beyond domestic financing sources [S4].

At year-end, cash plus marketable securities stood near $95 million supported by revolving credit availability exceeding $260 million on multiple lines designed for inventory financing and operational liquidity—providing ample cushion amid acquisition integration cycles or unforeseen fluctuations [S10][S11].

Cost Efficiency and Occupancy: Drivers Behind Improved Operating Margins

Despite inflationary pressures evident in rising labor costs, insurance premiums, property tax assessments, and utility fees typical across real estate operations nationwide, UMH managed further compression of its expense ratio at the community level from roughly 39.7% at end-2024 down to about 39.3% as of December 31, 2025 excluding one-time legal expenses [S16][S17]. This reflects effective fixed-cost absorption through higher occupancy plus targeted administrative expense control.

Occupancy improvements played a dual role: elevating revenues directly via increased leased sites while enhancing operational efficiency since many overheads do not scale linearly with occupied units—incremental occupied lots translate disproportionately into NOI gains.

Rental home occupancy remained resilient at roughly 93.8%, significantly above overall site occupancy (~88%), underscoring strong tenant demand for turnkey affordable housing options embedded within UMH’s portfolio [S19].

Portfolio Expansion: Acquisitions, Community Developments, and Opportunity Zones

UMH completed five community acquisitions adding approximately 587 developed homesites primarily located in key states such as New Jersey, Maryland, Georgia—acquired for aggregate consideration around $41.8 million [S1][S28][S29]. Several properties required planned renovations funded out of capital improvement budgets.

Capital expenditures approached $49 million focused on improvements including land development expansion plus purchasing new manufactured homes targeted for rental deployment intended to add recurring revenue streams over time [S16][S28].

The Opportunity Zone Fund continued deployment targeting lower-income communities requiring material capital infusion; this fund holds majority interests in select newly acquired or under-development assets providing preferential tax incentives while contributing to long-term portfolio value uplift [S13][S28].

Risks on the Horizon: Regulatory Constraints, Inflation, and Competitive Acquisition Landscape

Regulatory challenges involve jurisdictional rent controls or caps limiting annual rent escalations which could temper revenue upside amid rising operating cost environments—though stable portfolio occupancy mitigates near-term downside if tenant retention remains steady [S2][S1].

Inflation remains a headwind particularly impacting utilities (water/sewer), payroll due to wage pressures post-pandemic labor shortages—and insurance premiums heightened by climate events—all contributing upward toward community operating expenses despite offsetting rental revenue growth.

Competition intensifies for manufactured home community acquisitions as institutional investors increasingly recognize sector fundamentals anchored by affordable housing demand—making sourcing accretive deals more challenging without premium pricing or extensive due diligence capable of mitigating deferred maintenance risks associated with older parks.

Financial risk includes marked-to-market volatility related to UMH’s REIT securities portfolio which though small (~1%) registered unrealized losses nearing $40 million during the period reflecting broader market swings impacting dividend income stability [S19].

Capital Allocation Strategy: Dividends, Buybacks, and Debt Management

Consistent with REIT tax requirements mandating distribution of taxable income majority portions annually, UMH increased quarterly dividends by one cent representing a near-4.7% hike raising per-share payouts while maintaining manageable payout ratios consistent with normalized FFO coverage metrics [N5][S7][N4]. Tax treatment clarity was announced early in the year reinforcing shareholder understanding.

Share repurchase activity accelerated slightly within an expanded authorization capped at $100 million resulting in approximately $4.8 million bought back during calendar year under review at an average price around $15 per share—serving as both return-of-capital mechanism and balance sheet optimization when market prices presented attractive entry points [F1][S7].

Refinancing efforts replaced short-term debt with longer-duration instruments offering fixed-rate stability helping contain borrowing costs despite rising interest rates; total debt increased aligned with acquisition funding but managed prudently within net leverage ratios (~27%-28% net debt/market cap) sustaining ready credit access when needed [F1][S4][S9].

Estimated free cash flow (operating cash flow less capital expenditures) near $69 million underscores internal funding capability cushioning external financing reliance amid unpredictable cycles.

What Investors Should Watch in UMH’s Forward Path

Key indicators include utilization rates under credit facilities such as Fannie Mae loans integrating seventeen communities—gauging financing agility versus acquisition pipeline robustness amid competitive pressures or valuation shifts beyond yield thresholds acceptable for accretive growth targets [N3][N6].[N4]

Capital deployment efficiency remains paramount—measured both by acquisition cap rates exceeding cost-of-capital thresholds and execution of value-add initiatives within opportunity zones or renovation projects elevating asset economics beyond scale advantages historically observed.

Operational metrics like occupancy trends hold significant weight given direct correlation with cash flow visibility amid uncertain macroeconomic pressures including mortgage interest rate shifts influencing lease versus buy decisions among targeted residents.

Regulatory developments affecting allowable rent increases merit close attention given capacity to constrain upside even as underlying demand drivers persist; evolving legislation or ordinances may impose limits or require enhanced tenant protections necessitating adaptive management responses or strategy recalibrations.

Liquidity anchored by diversified capital sources—from ATM equity sales enabling opportunistic needs through DRIP participation driving shareholder base stability—supports balanced growth versus risk tradeoffs integral within manufactured home REIT operations today.

This analysis synthesizes UMH PROPERTIES’ latest financial disclosures augmented by relevant industry context without offering investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments