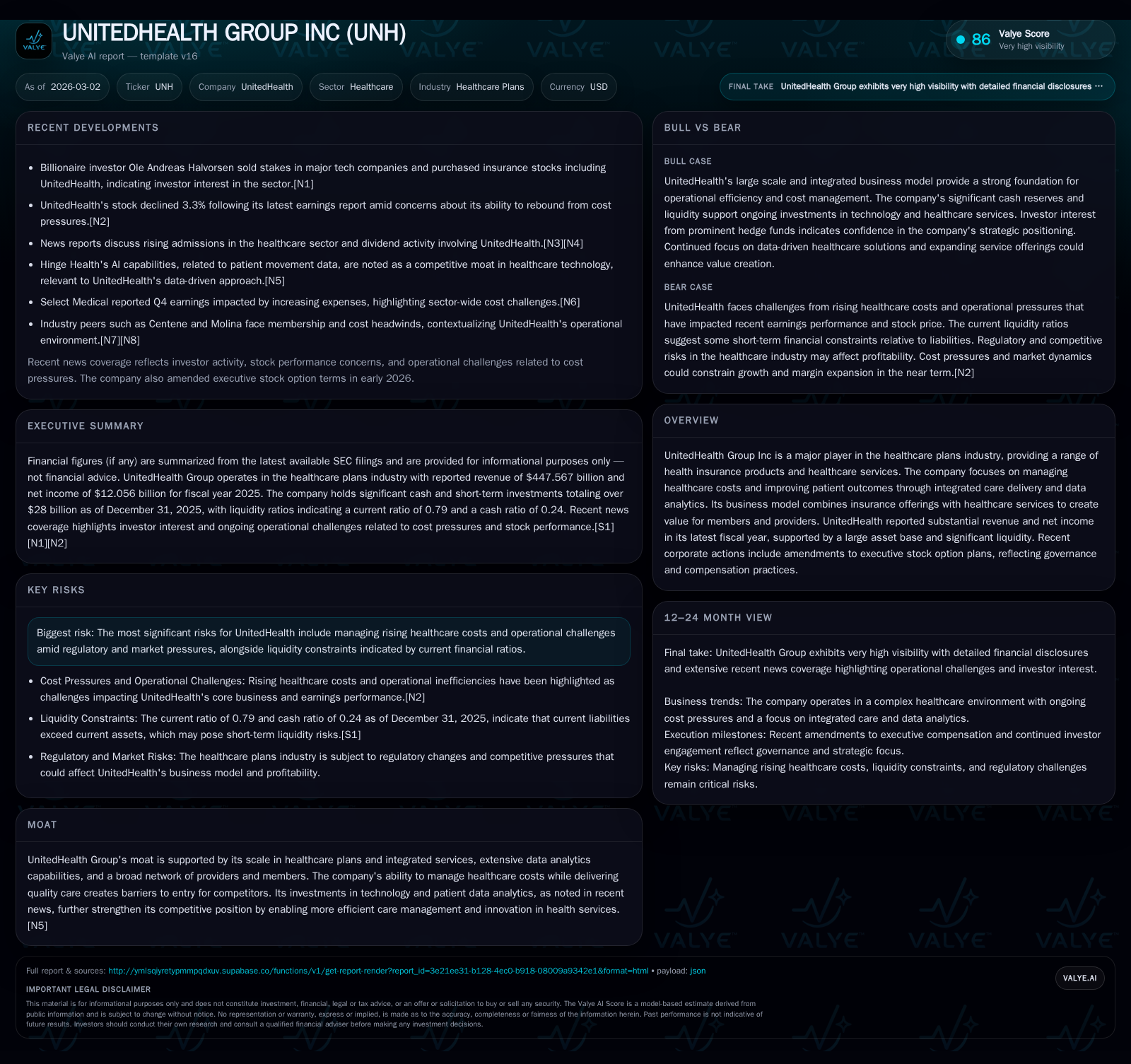

UnitedHealth Group's Earnings Volatility Reflects Shifting Healthcare Dynamics

UnitedHealth Group reported robust revenue growth in 2025 but faced notable profit and cash flow compressions amid rising medical costs and regulatory challenges.

In fiscal 2025, UnitedHealth Group solidified its position as a healthcare titan with top-line growth nearing 12%, yet confronted a pronounced decline in operating and net income driven by escalating healthcare expenses. The company's integrated care delivery model, powered by advanced data analytics and extensive provider networks, remains a durable competitive advantage, though emerging operational headwinds have pressured margins. Capital allocation balances shareholder returns with cautious cash flow management amid cost volatility. Looking ahead, the company's ability to leverage technology and refine care coordination will be critical to offset regulatory and inflationary pressures that cloud near-term profitability.

Historic Momentum: Revenue Growth and Profit Compression

UnitedHealth Group’s fiscal year 2025 results illustrate a compelling dichotomy between scale-driven revenue gains and acute margin pressures. The company posted a robust top-line increase of 11.8% year-over-year, reaching approximately $447.6 billion in revenues [F1]. This growth trajectory continued the firm’s historical pattern of expanding market share within healthcare plans and services.

However, this top-line momentum did not translate into proportional bottom-line gains. Operating income sharply contracted by over 41%, landing at approximately $18.96 billion [F1]. Net income also declined by over 16% to about $12.06 billion [F1]. Such profit compression reflects intensifying cost burdens largely attributable to rising medical claims expenses, a common challenge for healthcare insurers contending with inflationary dynamics in clinical services and pharmaceuticals.

The compression of earnings amid surging revenue underscores the impact of adverse medical loss ratios (MLR), revealing the tight balancing act UnitedHealth must maintain between pricing policies, risk assumption, and claims management effectiveness.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 447.6 | 12.1 | 19.7 | 19.0 | +11.8% | -16.3% |

| 2024 | 400.3 | 14.4 | 24.2 | 32.3 | +7.7% | -35.6% |

| 2023 | 371.6 | 22.4 | 29.1 | 32.4 | +14.6% | +11.2% |

| 2022 | 324.2 | 20.1 | 26.2 | 28.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) |

|---|---|---|

| 2025 | 5.5 | 16.1 |

| 2024 | 9.0 | 20.7 |

| 2023 | 8.0 | 25.7 |

| 2022 | 7.0 | 23.4 |

Source: SEC companyfacts cache [F1].

Revenue, income, cash flow, and capex figures are billions USD; percentage changes are year-over-year where available [F1].

Integrated Care and Data Analytics as Strategic Differentiators

UnitedHealth’s competitive advantage is anchored in its integrated healthcare plans combined with vertically coordinated care services supported by advanced data frameworks [N5]. This approach enables risk-adjusted care management strategies optimizing resource utilization across its broad member base.

Sophisticated claims analytics provide predictive insights on patient populations facilitating proactive interventions that help moderate cost escalation rather than merely reacting post hoc to claims inflation—a significant edge in managing medical cost ratios.

The company leverages an expansive provider network facilitating scale economies in negotiated reimbursements while deploying platform-enabled care models that improve clinical outcomes through coordinated efforts among practitioners, patients, and payers.

These capabilities create high entry barriers around data aggregation methodologies and risk modeling frameworks essential for sustaining favorable underwriting economics.

Recent Earnings Performance and Cost Management Challenges

Q4 fiscal reports delivered mixed signals about UnitedHealth’s ability to manage expense volatility [N6][N7][N10]. While some analysts highlighted earnings beats driven by persistent top-line growth, others noted surges in operating expenses linked to claims inflation and investments in technology infrastructure.

Shares experienced significant price swings post-earnings announcements reflecting investor uncertainty around ongoing medical cost pressures undermining margin recovery prospects [N1][N14]. Industry peers similarly face escalating medical loss ratios across Medicaid and Medicare segments due to demographic shifts and healthcare inflation [N4][N5].

This operational expense volatility highlights challenges navigating cost headwinds alongside evolving regulatory mandates that impose compliance costs.

Regulatory Environment and Litigation Risks Shaping Outlook

As detailed in the latest annual filing [S4][S5], UnitedHealth faces ongoing compliance headwinds from dynamic insurance regulatory environments marked by intensified oversight of pricing practices within public programs.

Continuing litigation matters underscore operational risks with potential contingencies related to claims processing accuracy, reimbursement policies, or contractual disputes with providers and government entities [S4].

Such regulatory dynamics contribute directly to margin variability given constraints on rate adjustments requiring strategic recalibrations by management.

Capital Deployment: Shareholder Returns Amid Cash Flow Decline

UnitedHealth sustained capital return programs despite lower free cash flow generation caused by reduced operating cash flow alongside steady capex increases [F1][S7]. Dividends remain stable supporting payout ratio consistency while share repurchases moderated from $9 billion in FY24 to roughly $5.55 billion in FY25 indicating buyback tapering amid liquidity caution.

Governance updates introduced a two-year post-vesting holding requirement for executive stock options granted last year, effective February 2026—reflecting an emphasis on aligning leadership incentives with long-term shareholder value creation [S7].

Free cash flow for FY25 approximated $16 billion (operating cash flow minus capex), indicating robust positive cash generation enabling ongoing distributions alongside reinvestment activities [F1].

Growth Levers Ahead: Opportunities in Technology and Care Delivery

To counterbalance margin pressure, UnitedHealth emphasizes advancing platform-enabled care models empowered by AI-enhanced patient data analytics as outlined in recent disclosures [N5].

Integration of machine learning into clinical decision support tools promotes personalized treatment protocols aligned with evolving value-based payment frameworks prevalent across U.S healthcare landscapes.

Expanding these technological frontiers can deepen risk adjustment precision while streamlining administrative workflows pivotal for scaling sustainable growth beyond conventional membership expansions.

While these initiatives offer potential catalysts for future growth stabilization or acceleration, they operate amid regulatory scrutiny and heightened medical cost inflation limiting near-term upside.

What To Watch: Metrics and Milestones for the Coming Years

Key indicators include membership retention rates especially within Medicare Advantage plans impacting risk pool quality metrics critical for underwriting results.

Monitoring medical cost ratio trends provides insight into claims management efficacy amid inflation; structural improvements would indicate margin resilience.

Regulatory developments affecting reimbursement rules or compliance requirements bear direct influence on operational flexibility.

Quarterly earnings surprises relative to consensus will signal UnitedHealth's agility in navigating volatile expenses.

Adoption rates and effectiveness outcomes from AI-driven care coordination platforms represent forward-looking markers for innovation success translating into financial returns.

This analysis is based solely on publicly available filings as of early March 2026 without investment recommendations or forecasts beyond disclosed facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments