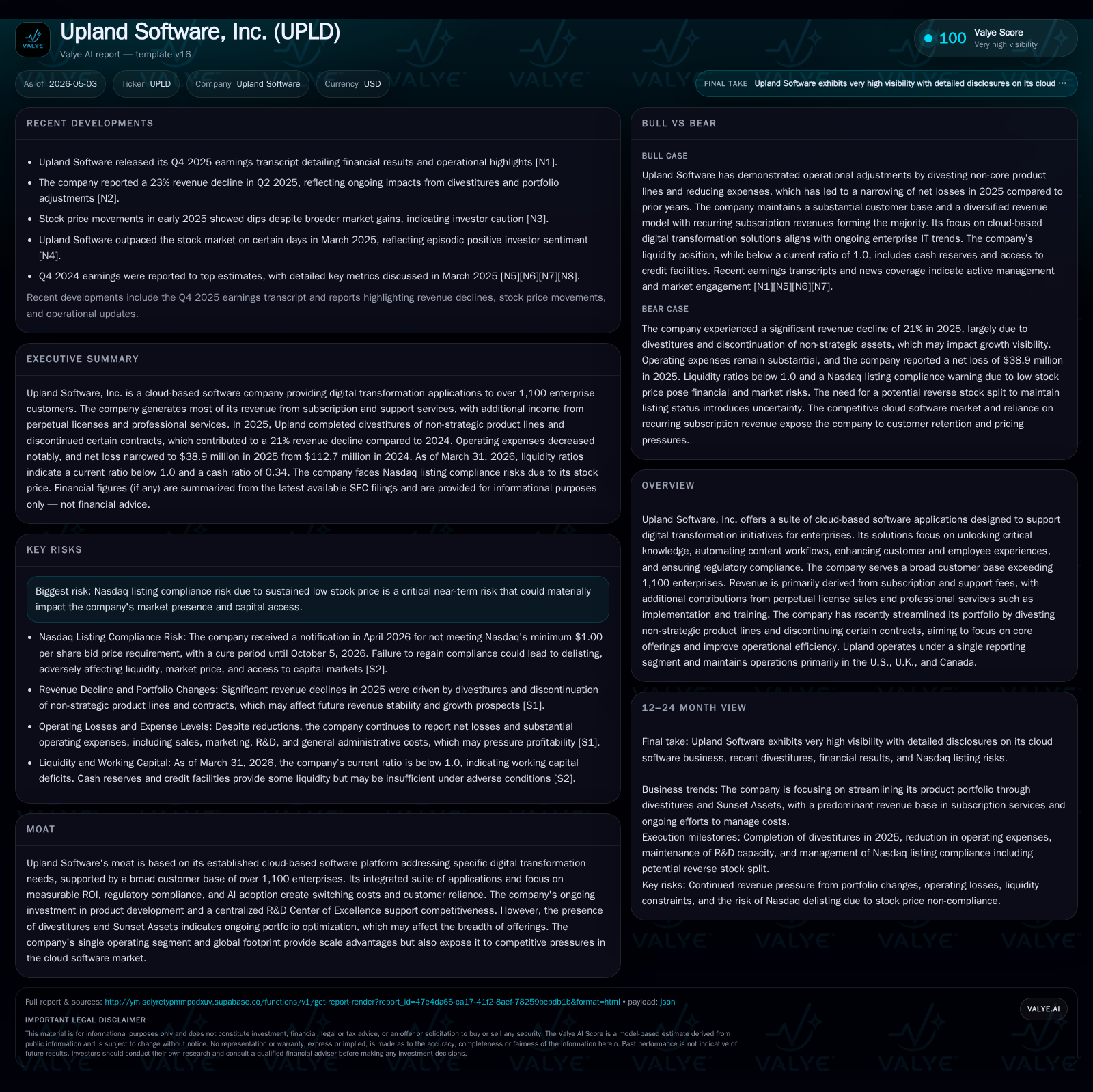

Upland Software Faces Nasdaq Listing Pressure While Refining Cloud SaaS Portfolio

Latest quarterly results reveal strategic portfolio streamlining and intensifying Nasdaq compliance risks amid steady subscription revenue.

Upland Software's most recent quarter underscores its continued focus on digital transformation software for enterprise clients, with subscription revenues maintaining stability despite divestitures of non-core assets. The company is navigating Nasdaq's minimum bid price requirement challenge, creating a critical compliance catalyst near-term. Upland’s business model leverages a cloud SaaS platform addressing knowledge automation, workflow enhancement, and compliance needs, supported by over 1,100 enterprise customers mainly in the U.S., U.K., and Canada. Growth depends on deepening cloud-native adoption, AI-driven solutions, and operational efficiency gains tied to its R&D Center of Excellence. However, its high leverage, working capital deficit, and looming Nasdaq delisting risk weigh on market standing and capital access.

Recent Operating Update: Q1 2026 Results & Nasdaq Listing Challenge

In its May 1, 2026 10-Q filing [S2], Upland Software reported relatively stable subscription and support revenues amidst ongoing portfolio simplification activities that have trimmed both revenues and expenses from non-core product lines. The company continues to recognize subscription fees ratably over contract terms generally spanning one to three years. Notably, the legacy 'Sunset Assets' have been systematically discontinued or divested since 2025 with corresponding expense reductions in sales and marketing tied directly to these products [S1].

However, the most pressing near-term development for Upland came with Nasdaq’s April 7 notice informing the company that its common stock had traded below the required minimum closing bid price of $1.00 for over 30 consecutive business days [S2]. This started a 180-calendar day compliance window through October 5, 2026 to remedy the deficiency with a qualifying ten consecutive trading day price recovery. Should this fail, approval of a reverse stock split proposal currently planned could be necessary to requalify. Failure to regain listing status may lead to delisting which would hamper liquidity, limit analyst coverage and restrict capital raising avenues [S2]. This risk represents a material operational constraint beyond pure product or market execution.

Financially, as of March 31, 2026 (end of Q1), the balance sheet showed $29.8 million in cash and equivalents against current liabilities of $87.2 million resulting in a current ratio below parity at around 0.84 [F1]. The company carried approximately $238.5 million in total debt (best-effort at end-2025), translating into about $209 million net debt after adjusting for cash balances—indicating significant leverage pressures for this SaaS operator largely reliant on subscription cash flows [F1]. Liquidity is further supplemented by an undrawn $30 million revolving credit facility maturing in July 2031 secured alongside $240 million term loan entered into mid-2025 [S4][S11].

Business Model: Focused SaaS Subscription Framework with Integrated Services

Upland operates a cloud-based software platform delivering modular applications designed around enterprise digital transformation themes — primarily knowledge unlocking, workflow automation for content-driven processes, employee/customer experience management, and regulatory compliance facilitation [S1]. Revenue predominantly stems from subscription fees paid by more than 1,100 enterprises globally (mainly U.S., U.K., Canada) recognized evenly over contract periods typically lasting one to three years [S1][F1].

Adding complexity are perpetual license sales granted upfront to certain customers alongside associated maintenance contracts billed as percentages of the license fee; these maintenance agreements offer ongoing support plus unspecified upgrades recognized ratably [S1]. Professional services encompassing implementation assistance, training and integration represent a smaller but meaningful revenue line recognized over time as milestones or service hours complete [S1].

Costs of revenue chiefly include hosting expenses (cloud infrastructure), salaries/bonuses for customer success teams and amortization related to acquired technology intangibles from prior M&A activity [S1]. The company has recently optimized spending by terminating legacy vendor contracts related to outsourced R&D following divestitures — enabling internal concentration within its R&D Center of Excellence that seeks efficient innovation while preserving product competitiveness [S1].

Upland's single operating segment approach consolidates various offerings under one reporting umbrella enabling streamlined resource allocation but also exposing results fully to cloud software market variability without diversification buffer [S9].

Industry Structure & Competitive Position

Operating within the crowded enterprise SaaS space targeting digital transformation workflows places Upland among numerous specialized vendors competing for share in segments such as content lifecycle management, CRM extensions focused on experience enhancement, complex compliance tracking solutions (e.g., GDPR/CCPA adherence), and emerging AI-assisted automation tools.

Upland’s competitive moat primarily derives from:

- Its integrated suite model fostering switching costs through ecosystem lock-in.

- Long-standing customer relationships exceeding 1,100 enterprises.

- Product development elevated by an internal R&D Center emphasizing AI incorporation enhancing ROI realization.

- A geographic footprint focused on mature English-speaking markets where regulatory scrutiny demands compliant-ready products.

However, frequent portfolio pruning via divestitures indicates ongoing reassessment of strategic fit for several offerings potentially narrowing market scope but improving capital allocation effectiveness. Additionally, although scale exists relative to pure-play startups, Upland still competes against major cloud incumbents deploying broad suites with extensive capital – heightening pressure on pricing power especially as enterprise IT budgets face macroeconomic headwinds.

Growth Drivers

The path forward hinges on participation in structurally growing trends linked to enterprise digitization:

- Expansion of Subscription Base: Capitalizing on increased cloud migration plus digital modernization mandates across sectors creates steady demand for solutions that automate complex workflows.

- Upselling AI Capabilities: Embedding artificial intelligence into content automation and compliance monitoring enhances value proposition enabling premium pricing tiers.

- Cross-sell & Integration: Leveraging modular nature of applications allows bundling opportunities within existing installed base improving retention rates.

- Operational Efficiency: Streamlining R&D expenditures post-divestitures supports margin improvement without sacrificing feature delivery pace.

- Geographic Penetration: Opportunity remains to deepen penetration beyond primary regions through channel partnerships or targeted direct sales efforts.

These drivers are measurable through KPIs such as bookings growth in new subscriptions/contracts (not explicitly provided but implied via strategic commentary), deferred revenue trends reflecting advance billings cash inflows, churn rates post-Sunset assets rationalization, and cost per acquisition improvements aligning with reduced sales campaigns on non-core lines.

Risks & Watchpoints

A focal risk point is Nasdaq’s continued listing jeopardy stemming from persistent sub-$1 share price trading invoking delisting threats with material consequences for liquidity and financing options [S2].

Financially:

- Elevated leverage near $209 million net debt pressurizes cash flow coverage metrics especially if organic growth falters or interest rates rise further given floating rate exposure partially capped only starting late 2025 [F1][S17].

- Working capital deficit signals near-term liquidity tightness requiring vigilant collections management and deferred revenue conversion efficiency.

- Potential impacts from macroeconomic uncertainty constraining enterprise IT discretionary spending could delay new customer acquisitions or contract renewals impacting top-line trajectory.

Operationally:

- Execution risks tied to successfully refocusing R&D investment following outsourcing termination — if internal productivity lags competitors might erode product competitiveness.

- Market dynamics in digital transformation remain highly competitive with increasing consolidation possibility challenging Upland’s standalone scale advantages.

What To Watch Next

Crucial milestones include:

- Monitoring Nasdaq listing status updates leading up to October 5, 2026; any board/stockholder decisions concerning proposed reverse stock split implementation will be pivotal.

- Quarterly updates on subscription bookings growth versus churn rates indicating traction or stress in footprint expansion.

- Progress reports on new AI-enabled product features or integration enhancements serving as growth accelerants.

- Changes in deferred revenue balances reflecting new contract wins or cancellations post-Sunset Asset unwind.

- Cash flow generation trends relative to ongoing leverage servicing capacity given forecasted interest burdens averaged near current ~9.7% floating rate floor.

Financial Profile Snapshot (Q1 Ending March 31, 2026) [F1]

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $30mm | |

| 2026-03-31 | ||

| Total debt | $239mm | |

| 2025-12-31 | ||

| Net debt | $209mm | |

| 2025-12-31 | ||

| Current assets | $74mm | |

| 2026-03-31 | ||

| Current liabilities | $87mm | |

| 2026-03-31 | ||

| Current ratio | 0.84x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

*Debt figure best-effort end-of-year per latest available data; no newer official update provided yet.[F1]

In sum, Upland Software presents as a focused enterprise SaaS provider grappling simultaneously with operational streamlining initiatives alongside serious near-term market listing risks that may constrain strategic flexibility. Success hinges on sustained technological relevance driven by cloud-native AI integrations paired with careful financial stewardship amidst competitive industry pressures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments