VisitIQ Corp. Advances AI-Driven Marketing Amid Privacy and Platform Consolidation Challenges

VisitIQ’s latest 10-K outlines ambitious AI roadmap and international expansion to capitalize on evolving digital marketing ecosystem constraints.

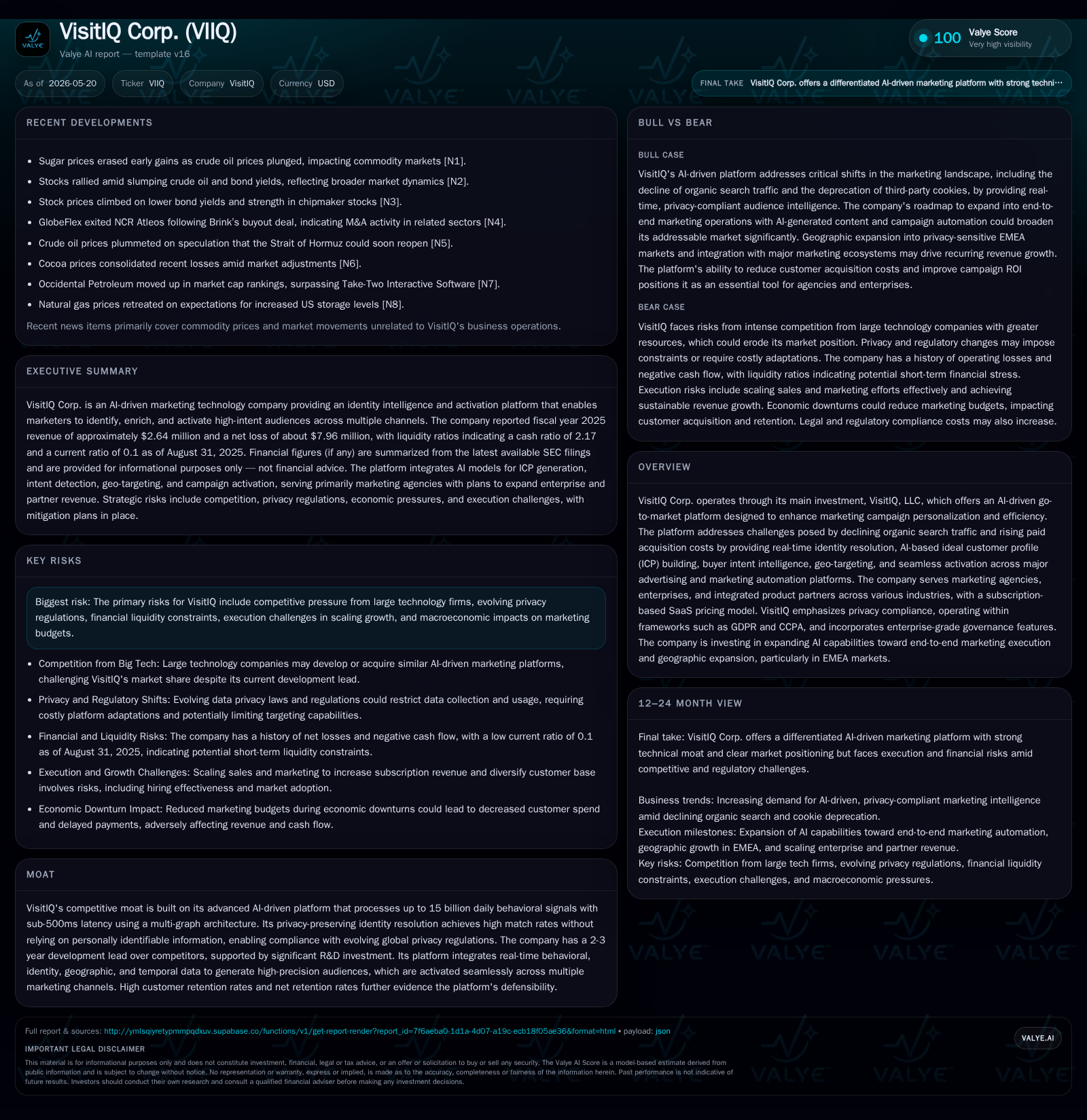

VisitIQ Corp.’s 2026 annual filing emphasizes its AI-first go-to-market platform designed to counteract the collapse of organic search traffic and rising paid ad costs. The company’s competitive edge stems from real-time, privacy-compliant identity resolution and a proprietary AI engine processing billions of behavioral signals daily. Growth will be propelled by enterprise adoption, agency expansion, integrated product partnerships, and geographic diversification into EMEA while enhancing the platform toward autonomous campaign execution. Key risks include funding needs, big-tech competition, regulatory changes, and customer retention.

Recent Operating Update

VisitIQ Corp.'s latest annual report (Form 10-K filed May 20, 2026) anchors the current business narrative around the transformation of its core AI-driven go-to-market (GTM) platform during seismic shifts in digital marketing [S1]. The filing highlights how rapidly declining organic search traffic—accelerated by AI-powered zero-click experiences—and increasing paid media costs across consolidated platforms have upended traditional demand generation models

The company invests heavily in addressing these challenges by delivering real-time identity resolution combined with behavioral intent signals that marketers can activate seamlessly across varied channels. VisitIQ underscores continued commitment to scale its platform internationally with a focus on privacy-compliant deployments in Europe that cater to increasingly stringent regulatory environments like GDPR [S3].

R&D priorities over the next 18 months include expanding signal ingestion from approximately 15 billion to over 20 billion daily data points, enriching taxonomy granularity via machine learning, embedding predictive propensity scoring AI layers, enabling enterprise-grade multi-tenant management APIs, and integrating tightly with leading Customer Data Platforms (CDPs) and Demand Side Platforms (DSPs) such as Segment and The Trade Desk [S6]. These advancements are expected to substantially increase visitIQ's Total Addressable Market (TAM), moving beyond targeting intelligence into full-funnel autonomous marketing orchestration.

Business Model

VisitIQ operates primarily through VisitIQ LLC which offers a subscription-based Software-as-a-Service (SaaS) platform tiered into Starter, Basic, Advanced and Professional levels. Pricing scales according to resolution volumes, lookalike audience generation complexity, real-time activation capabilities across multiple channels (including paid media, CRM systems, email marketing automation), and access to conversational AI interfaces for campaign strategy support [S12]

Marketing teams — both agencies managing multiple client campaigns and direct enterprise clients — pay for continuous audience enrichment that includes identity stitching without personal identifiable information (PII), real-time intent detection, geo-targeting based on movement data near physical locations like dealerships or retail outlets, and automated campaign activation through existing tools. VisitIQ’s integrated partners incorporate the platform APIs into ecommerce platforms, media players, CRMs or content management systems for white-labeled intelligence layering enhancing their value proposition [S14][S26].

The revenue mechanics rest on increasing monthly active usage measured as resolution volumes alongside seat licenses issued within agencies or enterprises. While acquisition is tiered by feature complexity, margin improvement arises from scaling fixed-cost infrastructure processing billions of signals rapidly using proprietary graph technology versus lower-margin data brokerage models.

AI proficiency enables VisitIQ to dynamically refine Ideal Customer Profiles (ICPs) based on live behaviors rather than static personas—empowering clients to reduce wastage of marketing spend by precisely matching surplus anonymous website visitors to conversion-ready audience segments [S17][S19].

Industry Structure and Competitive Position

VisitIQ competes in a fragmented market space bordering B2B intent data providers (e.g., Bombora), identity resolution platforms (e.g., LiveRamp), Customer Data Platforms (CDPs), traditional data brokers, and emerging autonomous marketing toolsets within the martech ecosystem [S22]. These competitors often specialize in singular capabilities but lack holistic real-time integration across identity resolution, behavioral intelligence, geo-targeting and channel activation combined with privacy-first architectures.

The company’s technical moat derives from a multi-graph database capable of querying petabyte-scale behavior & identity data within sub-500 millisecond latency—an operation infeasible for legacy relational databases or batch-processing competitors. VisitIQ’s innovative streaming pipeline ingests user signals within an hour versus the 24–72 hour lag typical of legacy intent vendors [S21].

Their privacy-sensitive identity resolution eschews reliance on cookies or PII identifiers achieving upwards of 85% deterministic match rates compliant with regulations such as GDPR and CCPA. This positions VisitIQ advantageously given global tightening of digital privacy standards threatening cookie-based ecosystems [S21][S18].

Customer reference points include exceptionally high annualized gross retention (~95%) and net retention exceeding 109%, signaling strong product stickiness amid competitive pressures. This also reflects trust in the data governance model crucial in regulated jurisdictions.

Growth Drivers

Agency Penetration Expansion

Currently over 90% of revenue derives from marketing agencies leveraging VisitIQ to enhance client campaign performance without operational overhead growth. As these agencies standardize platform use across their rosters, monthly usage scales naturally driving volume increases plus additional seat licensing fees. This network effect bolsters flywheel effects.

Enterprise Adoption Acceleration

Enterprises adopt VisitIQ often phased — starting with foundational identity resolution moving toward layered ICP modeling, intent attribution, geo-intelligence enrichment and ultimately cross-channel activation powered by AI automation [S14][S15]. This progression boosts contract sizes from base subscriptions toward $10K-$50K+ monthly engagements flagged in the roadmap.[S6]

Integrated Product Partnerships

Embedding VisitIQ intelligence within ecommerce systems, content delivery networks or CRM providers grants scalable distribution channels bypassing linear sales efforts while generating recurring margins. These partnerships heighten stickiness through ecosystem lock-in.

Geographic Expansion into Privacy-Conscious Markets

Scaled focus on EMEA reflects opportunity driven by heightened regulatory demands constraining incumbent advertising intelligence platforms geographically limited by legacy data restrictions [S3]. Localization efforts include regional datasets tailored taxonomies plus multilanguage AI interfaces accelerating adoption.

End-to-End Marketing Automation Evolution

Roadmap visions encompass transitioning from purely audience targeting layers into fully autonomous campaign ideation including creative generation (text/image/video), asset production workflows, budget allocation research views via AI-driven strategy modules culminating in seamless execution across all programmatic endpoints including emerging retail media networks [S15]. This ambition aligns TAM expansion projections growing from current ~$115B addressable spend upward toward $270B-$340B multi-phase forecasts.

Risks / Watchpoints / Growth Constraints

Capital Requirements & Liquidity Constraints

Despite technology achievements revenue remains modest at $2.6 million (FY2025) while net losses near $8 million stem from aggressive R&D investment [F1]. Working capital is constrained with current ratio extraordinarily low (~0.1) highlighting short-term liquidity pressure compounded by need for additional capital raises before late 2026 [F1][S9][S11]. Any failure to secure financing risks hampering growth plans.

Competition From Established Technology Giants

Wall Street marquee advertising technology incumbents like Salesforce/Adobe/Oracle are closing technological gaps aggressively towards integrated solutions. VisitIQ currently enjoys a roughly two-to-three-year lead based on proprietary graph tech but this window requires fast execution lest vulnerabilities emerge [S6][S15].

Regulatory & Compliance Complexity

Evolving digital privacy laws present continuous compliance challenges forcing investments into platform architecture adaptations plus potential market access constraints if rules tighten further or diverge globally.[S18][S23]

Execution Complexity Scaling Sales & Operations

Moving beyond early adopters toward large-scale enterprise contracts mandates significant hiring of sales talent (~10–15 Account Executives planned) plus tighter channel partnerships; missing execution targets here could hamper ARR growth trajectories reflected in internal guidance expanding from $3.2M to $6.5M ARR during scale-up phase [S13][S15]

Customer Retention & Payment Risk Exposure

Dependence on agency client models subject to sequential liability causes exposure if downstream clients default or delay payments potentially impacting cash flow stability especially during macroeconomic slowdowns affecting marketing budgets [S1][S7]

What To Watch Next

- Progress against roadmap milestones focused on signal volume growth beyond 20 billion daily events and deployment of predictive propensity scoring layers incorporating natural language query capabilities.

- Measured traction expanding international client wins particularly within GDPR-sensitive EMEA regions validating localization and compliance strategies.

- Expanding tier mix contribution emphasizing enterprise ARR scaling beyond agency dependency toward targeted $10K-$50K monthly contracts benchmarked internally.[S6][S14]

- Operational ramp-up effectiveness including hiring success for sales AEs alongside onboarding strategic partners such as Arena Investors supporting capital needs.[S9][S11]

- Regulatory developments impacting data collection mechanisms; any shifts compelling material alterations may present headwinds requiring accelerated engineering responses.[S18]

- Resolution progress on legal disputes historically tied to DrivenIQ foreclosure assets settled in May ’26 minimizing litigation risk.[S7]

Financial Profile Summary

Historical performance (annual)

Capital returns and efficiency (annual)

VisitIQ reported FY2025 revenues of approximately $2.6 million while incurring a net loss nearing $8 million reflective of ongoing heavy reinvestment in R&D capabilities supporting long-term differentiation [F1]. Operating cash flow remained negative at approximately -$2.6 million compounded by capex outlays near $1 million totaling a free cash flow deficit exceeding $3.5 million [F1]. As of August 31, 2025 balance sheet metrics show severely constrained liquidity highlighted by a current ratio near 0.1 indicating short-term liabilities substantially exceeding available current assets [F1]. Additionally net debt position exceeds $2 million evidencing financing reliance albeit partially offset by committed strategic shareholder funding expected through December 2026 [S11]. These financial signals mark near-term capital raising as critical enabler for executing outlined growth initiatives without which operational continuity could be imperiled.

This analysis synthesizes publicly filed disclosures without offering investment advice or recommending actions related to VisitIQ Corp.'s securities or operations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments