Valero Energy’s Shift from Scale to Stability: Assessing 2025 Performance and Strategic Outlook

Valero Energy transitions from peak refiners’ profits toward operational resilience and disciplined capital management amid macro uncertainties.

Valero Energy Corp experienced a notable pullback in operating income in fiscal year 2025, declining roughly 15% year-over-year, signaling a shift from the extraordinary margin environment that characterized recent years. This transition reflects widening cracks in refining throughput profitability driven by inflationary pressures, geopolitical risks, and evolving regulatory regimes. Nevertheless, Valero maintains a robust liquidity profile anchored by $4.7 billion cash and an extended revolving credit facility, supporting operational flexibility. Capital allocation continues to prioritize dividends and share repurchases even amidst earnings pressure, underpinning its value stock stature. Going forward, monitoring crack spread volatility, regulatory developments, and credit covenant compliance will be crucial to understanding Valero’s trajectory.

Historical Earnings Trajectory Highlights Margin Volatility

Valero Energy’s recent financial performance encapsulates the volatility characteristic of integrated refining businesses deeply linked to commodity market cycles and macroeconomic fluxes. Operating income peaked at an exceptional $15.7 billion in fiscal year 2022 before retreating sharply over the next three years to $3.18 billion by year-end 2025 [F1]. This dramatic contraction of approximately -80% over three years underscores the sensitivity of Valero’s refining throughput economics to crack spreads — the differential between crude oil prices and refined petroleum product prices which directly drives margins.

Year-over-year for 2025 alone, operating income contracted by -15.3%, mirroring a net income decline of -15.2% down to $2.35 billion [F1]. Operating cash flows slid similarly (-12.8%), though remained robust at $5.83 billion, indicative of strong underlying business operations tempered by margin pressure [F1]. Capital expenditure increased around +5.9% YoY despite earnings contraction — a nod to the capital-intensive nature of refinery maintenance and upgrades essential for compliance and throughput efficiency [F1].

This earnings trajectory reflects scale benefits during industry supercycles but reveals structural constraints tied to market cycles, regulatory costs, and inflation drags particularly acute in refining conversion margins.

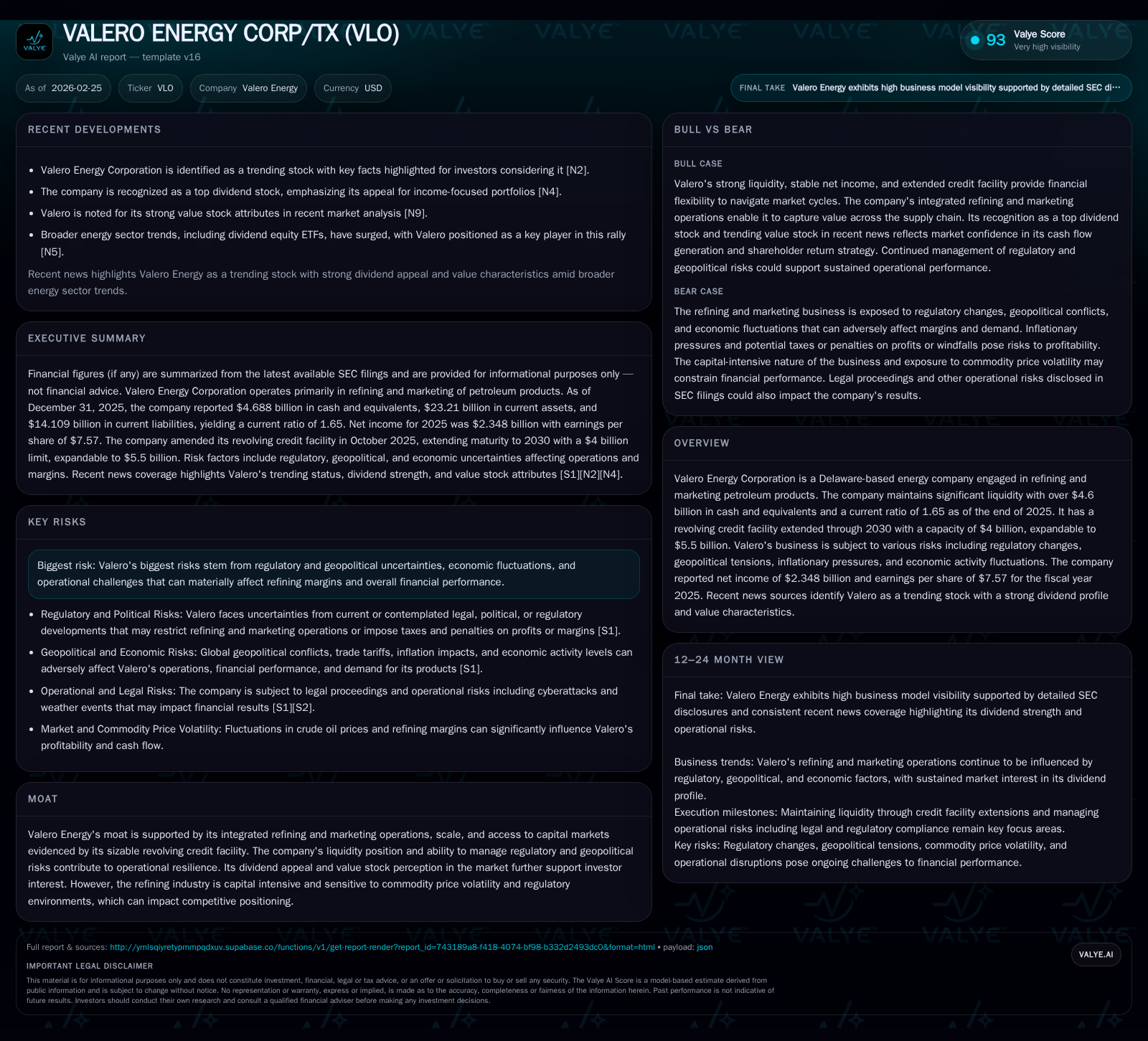

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Net YoY |

|---|---|---|---|---|

| 2025 | 2.3 | 5.8 | 3.2 | -15.2% |

| 2024 | 2.8 | 6.7 | 3.8 | -68.6% |

| 2023 | 8.8 | 9.2 | 11.9 | -23.4% |

| 2022 | 11.5 | 12.6 | 15.7 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | ROE% |

|---|---|---|---|

| 2025 | 1405 | 2.6 | 9.9 |

| 2024 | 1384 | 2.9 | 11.3 |

| 2023 | 1452 | 5.1 | 33.5 |

| 2022 | 1562 | 4.6 | 48.9 |

Source: SEC companyfacts cache [F1].

Note: Capex data only available for recent years; capex YoY calculated from partial data points.

Key Drivers Behind the 2025 Operating Income Decline

The marked earnings slowdown in fiscal year 2025 stems from a confluence of macroeconomic and industry-specific vectors outlined extensively in Valero’s SEC risk disclosures [S4][S6][S7], as well as corroborated through sector news reports [N5][N10]. Inflationary pressures elevated operational costs including energy inputs and maintenance services, squeezing already tight refining margins despite modestly resilient demand for transportation fuels.

Geopolitical tensions — particularly supply disruptions linked to regional conflicts impacting crude feedstock cost stability — exacerbated price volatility while complex and evolving environmental regulations imposed incremental compliance costs necessitating capital allocation toward emissions control technologies rather than expansion [S4][S7]. Commodity market headwinds led to less favorable crack spreads reducing per-barrel margins despite Valero’s integrated marketing channel advantages.

Demand fluctuations influenced by changing economic slowdowns reduced refinery throughput utilization rates slightly below optimal thresholds further pressuring unit margins [N5]. Additionally, uncertainty related to tax policies imposing windfall or excess profit taxes introduced planning difficulties affecting long-term capital strategy coherence.

Liquidity Strength and Credit Facility Flexibility Bolster Financial Health

Despite earnings headwinds, Valero maintains a liquidity fortress underscored by nearly $4.7 billion in cash and short-term equivalents as of December 31, 2025 [F1]. The company’s current ratio stands at a solidly conservative level of approximately 1.65, reflecting prudent working capital management optimizing short-term asset coverage against liabilities [F1].

Crucially, Valero extended its revolving credit facility on October 16, 2025 until October 2030 with a base commitment of $4 billion expandable up to $5.5 billion, underscoring access to substantial committed liquidity lines that support operational robustness amid cyclical uncertainty [S5][S9][S11]. Borrowing costs under this facility remain competitively tiered according to market benchmarks (SOFR plus margin tiers linked to credit ratings), while customary covenants enforce financial discipline without unduly constraining strategic flexibility [S5][S9].

This robust liquidity profile paired with manageable leverage provides effective cover against potential market shocks or investment requirements related to regulatory-driven capital expenditures.

Regulatory and Geopolitical Risks Reshaping Operational Landscape

Valero’s risk disclosures explicitly emphasize exposure to dynamic regulatory regimes encompassing tightening environmental standards both domestically and internationally [S4][S6][S7]. Compliance cost escalation linked to sulfur content limits, greenhouse gas emissions mandates, and renewable fuel standards mandates have driven reallocation of capital budgets toward mitigation infrastructure which may reduce free cash flow available for discretionary uses.

Geopolitical unpredictability surrounding crude sourcing—amidst fluctuating tariffs or trade policy shifts—impacts feedstock pricing and security of supply channels; these externalities challenge throughput planning precision hence affecting operating efficiency metrics such as refinery utilization factors and product slate optimization [S7][N14].

The company's legal filings underscore ongoing diligence around cybersecurity threats and weather-related disruptions that could intermittently impair plant operations or supply chain continuity further amplifying margin volatility risks.

Capital Allocation Emphasis: Balanced Dividends and Share Repurchases

Amidst a more constrained earnings environment for fiscal year ending December 2025, Valero demonstrated commitment to shareholder returns through persistent dividend payments amounting to approximately $1.41 billion consistent with prior years despite margin pressures [F1][S13][S15][N6]. This reflects a payout ratio calibrated carefully against current profitability levels within sector norms balancing retention for reinvestment.

Share repurchases remained substantial at roughly $2.6 billion in FY25 – albeit slightly reduced versus historical peaks – illustrating disciplined buyback programs aimed at enhancing per-share metrics without jeopardizing liquidity or triggering covenant constraints under debt facilities [F1][S22][S23]. The approximate return on equity (ROE) calculated from net income over average equity stood near an adjusted ~9.9%, indicative of steady capital efficiency amid less lucrative operating conditions [F1].

This balanced approach evidences an overarching strategy pivot favoring stability over aggressive growth investment amid external uncertainties.

Forecast Indicators: What Investor Should Monitor Next

While explicit forward guidance is absent within public SEC filings or company news releases for fiscal year beyond December 2025 [N5][N10], several key indicators merit close attention:

- Refining Crack Spread Movements: Given their central role in determining operating income volatility; monitoring product versus crude price relationships especially across naphtha, distillates, gasoline segments matters.

- Regulatory Developments: Updates around EPA standards or state-level emissions legislation impacting compliance expense forecasts.

- Credit Facility Covenant Compliance: Watch quarterly liquidity disclosures for indications on leverage ratios relative to covenants that may impinge flexibility.

- Dividend Sustainability: Dividend declarations amid fluctuating free cash flow will signal management’s confidence in lasting profitability resilience.

- Market Demand Elasticity: Shifts in gasoline/diesel consumption trends stemming from macroeconomic health or energy transition dynamics will affect refinery throughput optimization efforts.

These elements collectively form principal levers influencing Valero’s transition from scale-driven profits toward assured operational stability.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding Valero Energy Corporation or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments