Winning Catering Group’s Strategic Transition From Land Development to M&A Shell

Transitioning from an active land developer to a shell company, Winning Catering Group faces uncertain prospects amid a transformational merger.

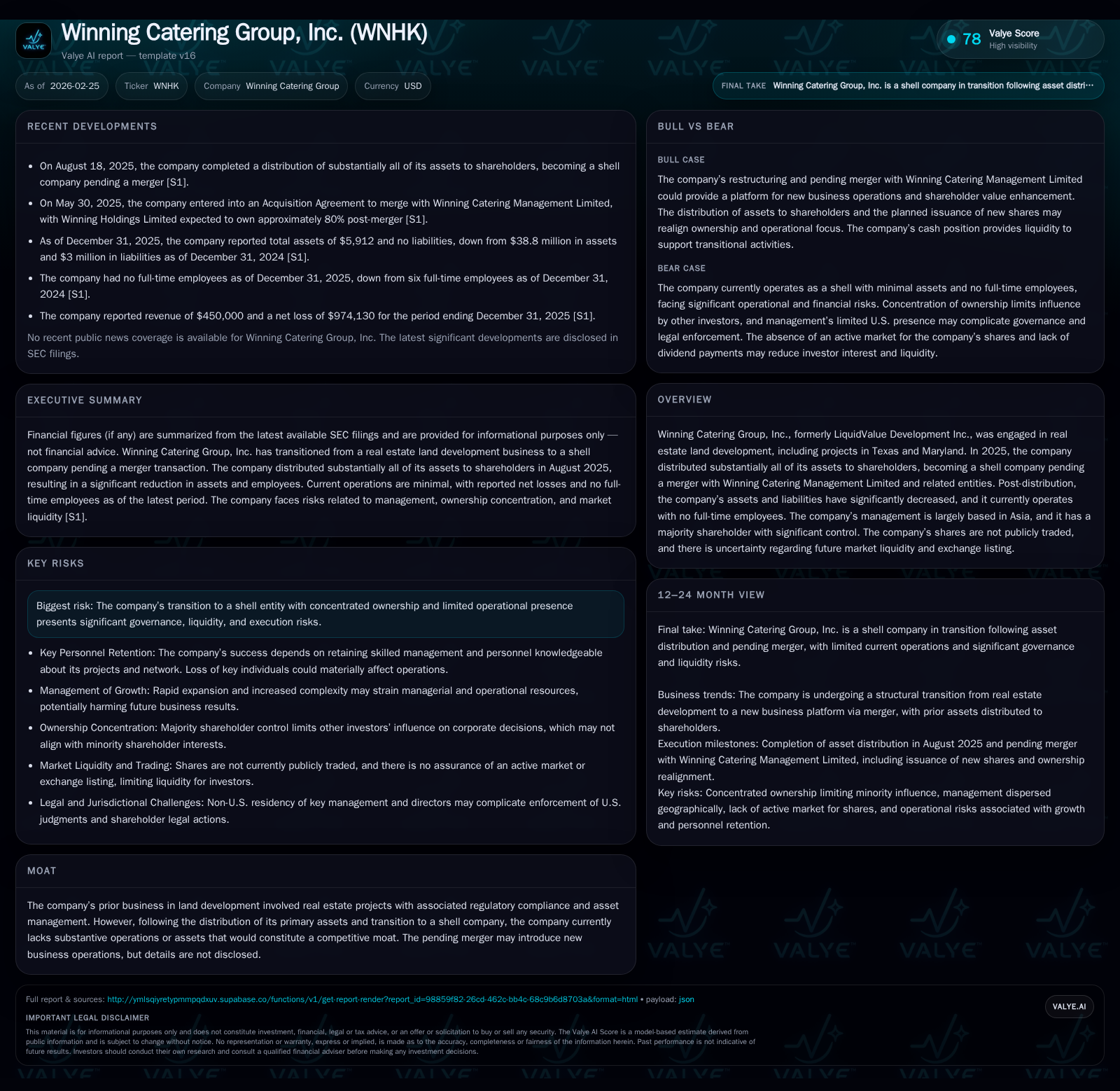

Winning Catering Group, Inc. has undergone a dramatic shift from an operating land development company to a shell entity pending a merger. Historically driven by real estate subdivision projects in Texas and Maryland, the company distributed nearly all assets to shareholders in 2025, resulting in near-zero revenues and operating cash flows. The pending acquisition by Winning Catering Management Limited introduces significant ownership concentration risks as the new majority stakeholder will control approximately 80% post-merger. Investors face material uncertainties surrounding future operations, liquidity, and governance given the transition phase and limited operational disclosure.

From Growth to Divestiture: Tracing Winning Catering’s Historical Performance

Winning Catering Group, formerly LiquidValue Development Inc., operated principally in real estate land development until mid-2025. Its core activities comprised land subdivision developments notably in Texas and Maryland, including the Lakes at Black Oak project near Houston and the Ballenger Run development in Frederick County. These land projects involved significant asset management agreements and regulatory compliance costs such as federal and state environmental studies that shaped project execution timelines.

Financially, the company demonstrated volatile but notable revenue growth prior to its transition: revenue rose from approximately $22.9 million in FY2019 down to $18.1 million by FY2023 before collapsing after divestiture [F1]. Operating income mirrored this trend with positive EBITDA intervals flanked by losses during earlier growth phases; net income swung accordingly from sizeable profits ($6.2M in FY2023) to steep losses by FY2025 following strategic divestment [F1].

Operating cash flows were similarly volatile; from negative $10 million in FY2022 reflecting expansion costs and project spending, CFO swung positive above $12 million through FY2024 supported by lot sales and community enhancement fees on residential subdivisions—a key cash generation lever common among developers who monetize incremental fees per lot sold alongside principal sales revenue [F1][S21].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1 | -1 | -1 | 1650 | -114.6% |

| 2024 | 7 | 14 | 6 | 1650 | +7.8% |

| 2023 | 6 | 13 | 6 | 3083 | +347.2% |

| 2022 | -3 | -10 | -1 | 3083 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1 | -16477.2 |

| 2024 | 14 | 18.7 |

| 2023 | 13 | 21.5 |

| 2022 | -10 | -11.2 |

Source: SEC companyfacts cache [F1].

*FY2025 figures reflect post-asset distribution impact leading to shell status.

Note: Operating Income and Net Income are available only for recent years; historic capex data limited.

(See Table Above)[F1]

Dissecting the 2025 Asset Distribution: Impact on Financials and Operations

In August 2025, Winning Catering executed a one-time special dividend distributing all shares of its wholly owned subsidiary Alset Real Estate Holdings Inc.—the holder of substantially all prior operating assets—to shareholders on a pro-rata basis [S14][S26]. This distribution amounted to approximately $34.8 million of carrying value representing nearly total net asset value at that time.

This transaction effectively severed the company’s operational business unit responsible for land development projects like Lakes at Black Oak and Ballenger Run from the parent holding entity. Post-distribution financials revealed total assets shrunk dramatically from $38.8 million at end-2024 to just $5,912 at end-2025 with liabilities extinguished entirely (zero reported) [S10][F1].

Operational headcount scaled back from six full-time employees as of December 31, 2024 to zero full-time employees by end-2025 reflecting elimination of ongoing project management roles [S10]. The cessation included termination or expiry of leasing contracts such as model home leases in Montgomery County Texas which had contributed ancillary rental revenue until early 2025 [S4].

From a regulatory perspective the distribution removed much of the need for costly environmental studies ($71K historically incurred pre-distribution) as control over development projects was migrated out of the parent Company scope [S10]. This step effectively transformed Winning Catering Group into what securities regulations term a "shell company"—an entity lacking meaningful operations—with attendant consequences on liquidity due to lack of tradeable operating assets or revenues [S14].

The Strategic Pivot: Evaluating the Planned Merger with Winning Catering Management Limited

Prior to completing its asset distribution strategy but subsequent thereto formally renamed Winning Catering Group on September 22, 2025 [S27], the Company entered an Acquisition Agreement dated May 30, 2025 signaling a strategic pivot away from real estate towards catering management operations [S1][S7]. This agreement contemplates merging LVD Merger Corp.—a wholly owned subsidiary—into Winning Catering Management Limited (the "Winning Group") with Winning Group surviving as a wholly owned subsidiary.

This transaction implies substantial changes including issuance of new common stock wherein Winning Holdings Limited is expected to own about 80% post-merger—resulting in considerable dilution for legacy shareholders who would retain only approximately 15% ownership per plans described prior to divestiture completion [S7][S16][S26].

While detailed disclosures concerning Winning Group’s business model have not yet been made public limiting visibility on operational synergy or growth prospects post-merger, this represents a complete overhaul of business purpose—from passive real estate asset manager toward active catering management firm based principally in Asia with corporate staff located there [N# similar context analysis][S1]. Integration risks loom large considering cross-border operational complexities and lack of legacy governance overlap.

Ownership Concentration and Governance Risks Amid Structural Change

Post-distribution and pending merger completion reveal significant ownership concentration concerns; SeD Intelligent Home Inc., currently holding ~99.99%, will retain dominant voting control which restricts minority shareholders' ability to influence key governance decisions including board composition and corporate transactions [S11][S1].

Management’s predominantly Asian residency—with Co-CEOs based overseas—and only one U.S.-based director raise enforcement risk for U.S.-investor claims in case of disputes given potential jurisdictional obstacles typical with foreign non-resident officers [S8][S11]. Such governance concentration combined with limited management resources amplifies exposure especially given the absence of employees post-divestiture.

Cross-border shareholder communications may be constrained culturally or legally complicating minority oversight further.

Liquidity, Capital Structure, and Cash Flow Profile in Transition

The asset distribution precipitated a collapse of tangible capital structure metrics: total assets ended fiscal year 2025 at merely $5,912 (down from nearly $38.8 million twelve months earlier), while liabilities fell from roughly $3 million to zero reflecting full repayment or reclassification upon transfer out of operating subsidiaries [F1][S10]. This effectively left no working capital runway.

Operating cash flow swung sharply negative (-$1.2M) despite minimal capital expenditure ($1.65K) indicating core business operations had ceased generating cash with overhead likely borne temporarily by retained contractors or minimal administration costs before merger integration begins [F1][S10].

The historical current ratio around 0.27 previously suggested liquidity constraints even during active development phases; this liquidity metric now lacks relevance given negligible working capital & activity levels.

Capital Allocation: Dividend History, Buybacks, and ROE Analysis Before and After Asset Distribution

Before its divestiture pivot period Winning Catering paid dividends intermittently with distributions totaling roughly $411K in FY2020 after $1 million in FY2019 showcasing reasonable free cash generation surplus at historical peaks—although buyback activity was negligible throughout firm history reflecting limited capital return focus amidst growth needs [F1][S7].

Return on equity calculations illustrate severe inversion post-divestiture; approximated ROE plunged to -16,477%, expressing loss-making structural realities with almost non-existent equity base ($5.9K as reported) serving as denominator against negative net income (-$974K FY25) [F1].

No announced plans exist for dividend resumption or share repurchases during transitional period pending merger realization; capital preservation coupled with external ownership control appears prioritized over distributions currently.

Forecast Horizons: What Investors Should Watch as the Merger Advances

Explicit guidance around closing milestones remain sparse though material events include finalization timing for LVD Merger Corp.'s absorption into Winning Catering Management Limited which will trigger issuance of new common shares diluting existing ownership significantly around expected ~80%-majority holder Winning Holdings Limited stake post-closing [S1][S7].

Upcoming developments to watch:

- Regulatory filings disclosing full details on new operational segment under catering management business line,

- Market relisting possibilities if applicable given current non-traded status impacting liquidity,

- Any capital raises or further corporate restructurings announced,

- Tracking commitments regarding management appointments or retention impacting integration success.

Given current inactivity with zero full-time staff and dormant asset base outside merger processes; realization hinges substantially on execution efficacy upstream from parent company.

Disclaimer

This report is prepared solely for informational purposes referencing publicly available documents including SEC filings up to February 25th, 2026 without incorporation of speculative or market rumors beyond reported facts. It does not constitute an investment recommendation or advice but aims to deliver an analytical narrative on Winning Catering Group's structural transformation phase accompanied by associated financials and governance considerations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments