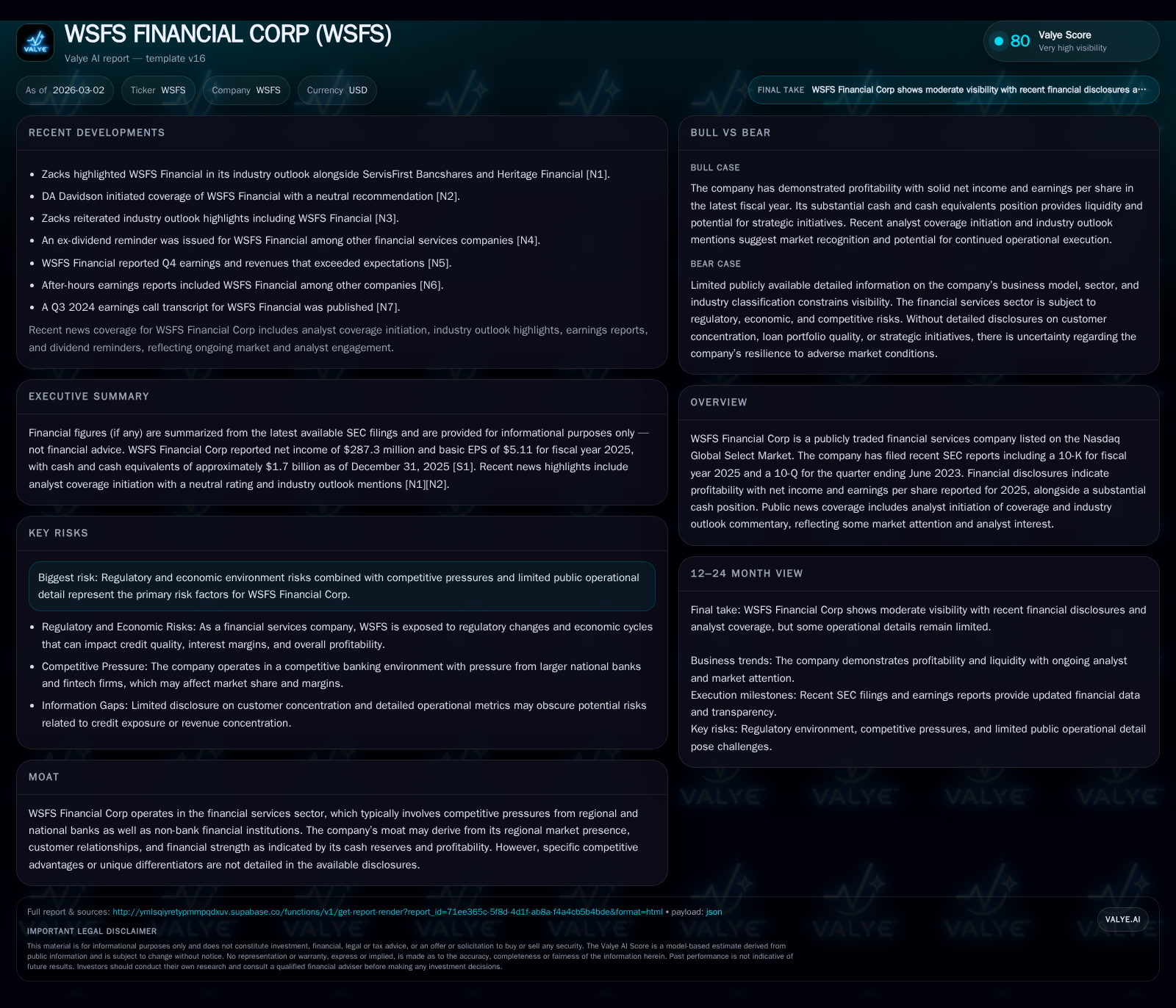

WSFS Financial’s Earnings Acceleration and Capital Strategy Spotlight Regional Strength

WSFS Financial Corp drives growth through strong revenue gains and disciplined capital management, emphasizing its regional banking franchise.

WSFS Financial has demonstrated robust revenue growth with a notable 50.2% increase in fiscal year 2022, followed by steady net income growth of 9% in fiscal year 2025. This performance underscores operational effectiveness and strategic capital deployment, including significant share repurchases and consistent dividends. The company’s regional footprint across Delaware, Pennsylvania, and New Jersey supports its competitive positioning amid a complex financial services landscape. Strong liquidity and recent debt refinancing enhance flexibility for organic and inorganic growth, while regulatory and economic risks remain key considerations.

Strong Revenue and Profit Growth Fuel WSFS's Momentum

WSFS Financial Corp’s fiscal year 2022 results reveal an impressive top-line acceleration with revenues reaching $963.9 million, representing a sharp 50.2% increase compared to $641.8 million in fiscal year 2021 [F1]. This surge contrasts with relatively stable revenues seen in prior years around the $709 million to $715 million range during 2019–2020.

Net income continued on an upward trajectory, rising to $287.3 million for FY2025—a roughly 9% increase from $263.7 million in FY2024—indicating effective expense management alongside growing revenues [F1]. Operating cash flow remained stable near $220 million during this period while capital expenditures declined sharply by over half to approximately $6.4 million in FY2025, reflecting prudent investment discipline [F1].

These financial trends highlight WSFS's sustained momentum driven by scalable regional banking operations combined with sound financial stewardship.

Distinctive Capital Allocation: Balancing Dividends, Buybacks, and Regulatory Capital

WSFS demonstrates a balanced approach to capital allocation that rewards shareholders while preserving regulatory capital adequacy. In FY2025 alone, the company repurchased about $290 million of common stock under its ongoing repurchase programs initiated since mid-2022—significantly accelerating buyback activity relative to previous years where annual repurchases ranged from approximately $54 million to over $200 million [F1][S1]. Dividends remained steady at roughly $37 million annually across recent years, signaling consistent shareholder returns without compromising capital buffers [F1].

Regulatory disclosures confirm a target Common Equity Tier 1 (CET1) capital ratio near 12%, comfortably above the "well-capitalized" threshold mandated by banking regulators. This prudent capital positioning supports ongoing share repurchases while maintaining strong tiered capital metrics—a hallmark of disciplined bank capital management aimed at optimizing shareholder returns without jeopardizing solvency [S1].

Additionally, WSFS completed issuance of $200 million fixed-to-floating rate senior unsecured notes in late 2025 to refinance higher-cost debt maturing earlier. This transaction extends maturities and enhances interest expense control without diluting equity or raising regulatory concerns [S10]. Such refinancing complements dividend and buyback strategies by improving balance sheet flexibility.

Evaluating WSFS’s Regional Banking Moat Amid Competitive Pressures

The company operates an extensive network comprising 87 branches primarily located in Delaware, southeastern Pennsylvania, and southern New Jersey, supplemented by approximately two dozen loan production offices extending into Florida, Nevada, and Virginia [S1]. This footprint enables relationship-driven banking critical for deposit gathering and community engagement within its core markets.

Facing competition from large national banks and fintech entrants as noted in risk disclosures, WSFS leverages customer intimacy and local presence as key differentiators rather than scale or proprietary technology advantages typical of larger institutions [S4][S13][S21].

While no singular disruptive advantage is publicly emphasized beyond geographic focus and relational banking strengths common among mid-sized regional banks, incremental expansion through loan production offices may provide diversification supporting margin resilience and growth opportunities [S1].

Financial Position and Liquidity Underpinning Growth Capacity

At December 31, 2025, WSFS held approximately $1.7 billion in cash and cash equivalents—a substantial liquidity cushion providing capacity for organic growth initiatives or acquisitions aligned with strategic objectives [F1]. The company's recent debt refinancing involved issuing senior unsecured notes bearing a fixed coupon of 5.375% until December 2030 before converting to a floating rate linked to SOFR plus spread thereafter. This structure extends maturity profiles while potentially reducing interest costs relative to previous debt instruments maturing sooner at lower fixed rates [S10][S11].

This solid financial position aligns with typical regional bank practices ensuring runway availability amidst market volatility while enabling measured expansion consistent with corporate strategy.

Operational diversification into ancillary services such as Cash Connect® further contributes to stable cash flows beyond traditional lending activities as referenced in property disclosures [S1], bolstering resilience against cyclical downturns.

Risks from Regulatory Constraints and Economic Cyclicality

WSFS acknowledges regulatory complexities impacting dividends and share repurchases through prudential standards governing "well-capitalized" status among banking institutions. These constraints act as guardrails limiting aggressive capital return policies despite internal appetite for shareholder distributions [S4].

Economic sensitivity within lending portfolios exposes WSFS to credit risk fluctuations during downturns or regional slowdowns concentrated around its East Coast branch network. Competition from larger banks with scale advantages remains a continuous pressure on margins and deposit pricing dynamics detailed in SEC filings [S13][S21].

Legal proceedings disclosed are currently immaterial but underscore ongoing compliance vigilance amid evolving regulations affecting community-focused banks like WSFS.

Outlook: Earnings Releases, Expansion Plans, and Capital Management Monitoring

Looking forward, upcoming quarterly earnings will shed light on the sustainability of revenue momentum potentially driven by loan volume increases or fee income growth alongside any margin pressures from deposit competition or credit cost shifts [N5][N3].

Management notes limited available space at current branch facilities suggesting potential new real estate investments or office acquisitions that could signal geographic expansion beyond existing footprints—monitoring these developments will be key for assessing growth strategy evolution [S1].

Tracking announcements related to share repurchase program renewals or dividend policy adjustments will also be critical given recent accelerated buybacks; balancing payout ambitions against capital retention needs will influence shareholder value generation going forward [N4][N5].

WSFS Financial Corp Selected Financial Metrics (FY2019–FY2025)

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 287 | 220 | 6 | +9.0% |

| 2024 | 264 | 220 | 14 | -2.0% |

| 2023 | 269 | 237 | 6 | +21.0% |

| 2022 | 222 | 481 | 9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 37 | 290 | 214 |

| 2024 | 36 | 96 | 206 |

| 2023 | 37 | 55 | 231 |

| 2022 | 36 | 200 | 472 |

Source: SEC companyfacts cache [F1]. *Note: Revenue data for FY23-FY25 is not fully available; latest reported full-year revenue used for illustration purposes only.

This analysis integrates comprehensive public financial disclosures alongside operational insights shaping WSFS Financial Corp's recent performance trajectory. Its strong regional franchise combined with disciplined financial management supports current momentum; however, regulatory oversight coupled with economic cyclicality underscores the sector's inherent challenges within mid-sized U.S. bank holding companies.

Disclaimer: This memo is based exclusively on publicly available information cited herein and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments