West Bancorporation Drives Regional Strength Through Capital Discipline and Strategic Loan Growth

WTBA leverages focused regional commercial lending and prudent capital management to fuel earnings growth and operational resilience.

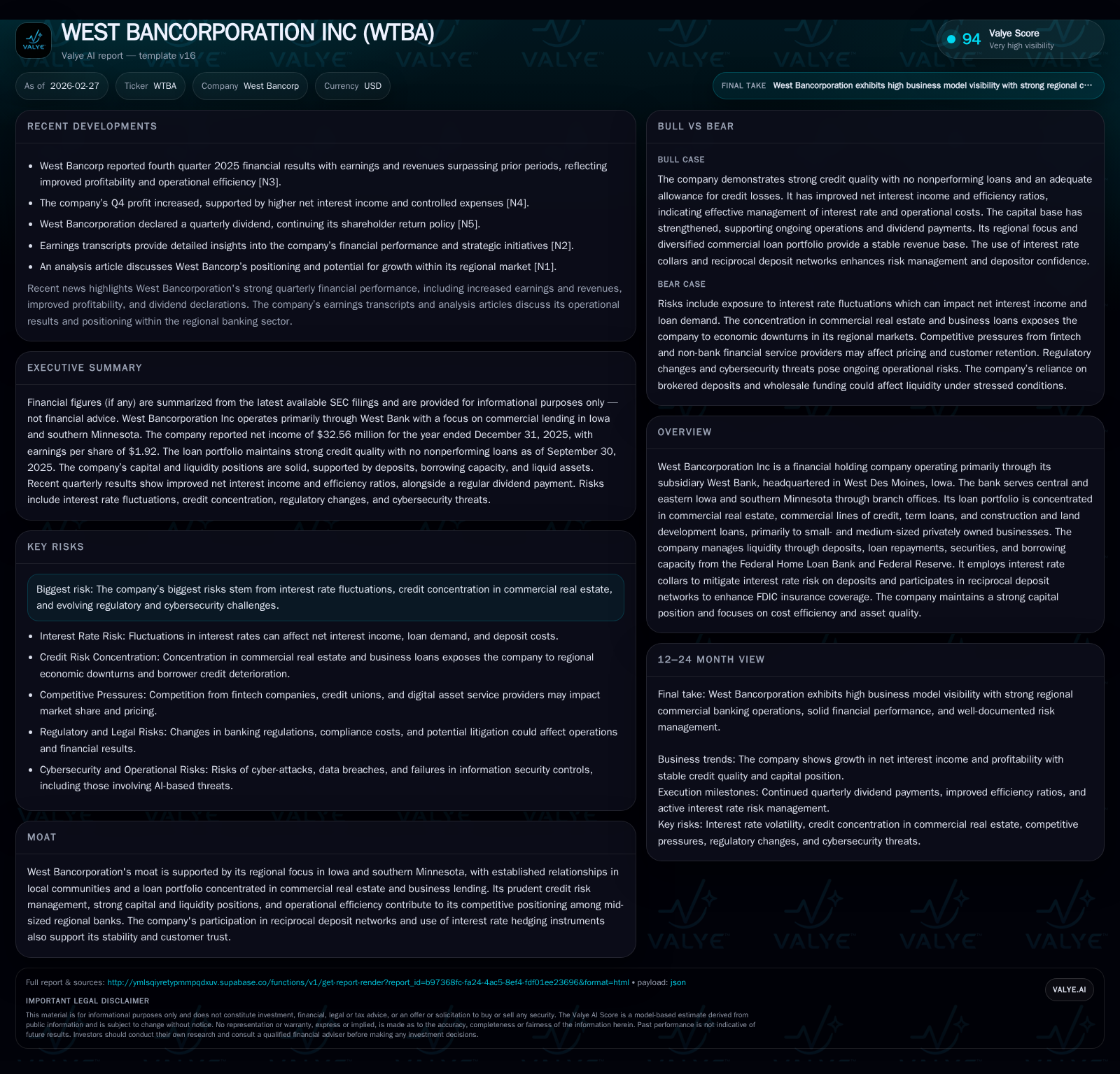

West Bancorporation Inc (WTBA), operating primarily through its subsidiary West Bank, marked a robust FY2025 with a 35% net income increase supported by strategic loan portfolio management and strong cash flow. Concentrated in commercial real estate and small- to medium-sized business loans across Iowa and southern Minnesota, WTBA balances growth ambitions with credit concentration risk prudently monitored under rigorous regulatory frameworks. Capital discipline is evident in rising equity, consistent dividends, and negligible buybacks, all underscored by effective liquidity and interest rate risk controls. The bank’s operational efficiency amid evolving macroeconomic headwinds positions it for sustainable future growth contingent on monitoring asset quality trends and deposit stability.

Regional Focus and Lending Portfolio: Foundations of Growth

West Bancorporation operates predominantly through West Bank with a geographic focus on central and eastern Iowa plus southern Minnesota [S1][F1]. This concentrated footprint underpins a carefully curated loan portfolio consisting chiefly of commercial real estate loans, commercial lines of credit, term loans, as well as construction and land development financing [S1][S29]. The clientele largely comprises small- to medium-sized privately held businesses that demand larger balance credits whose repayment depends upon ongoing successful operations.

This specialization grants WTBA an entrenched niche—stimulating relationship banking evidenced by stable customer engagement but simultaneously amplifying exposure to credit concentration risk inherent in commercial real estate (CRE) cycles. Management maintains asset quality vigilance via regulatory thresholds compliance (e.g., CRE exposure limits relative to capital) while employing rigorous monitoring protocols for delinquency or stress calls—a vital facet in maintaining their moat within this mid-sized regional bank peer group framework [S18][S29].

Financial Performance Trends: Earnings and Cash Flow Evolution

The company exhibited a notable rebound in profitability for the fiscal year ending 2025. Net income soared approximately 35%, climbing from $24.05 million in FY2024 to $32.56 million in FY2025 [F1]. This robust earnings progression corresponds with improved operational efficiency as reflected in a 16.8% rise in operating cash flow ($39.8 million to $46.5 million) over the same period.

Simultaneously, capital expenditures underwent a dramatic contraction shrinking by about 87%, dropping from $26.14 million in FY2024 to just $3.33 million in FY2025. Such a sharp pullback likely signals shifting strategic priorities toward optimizing existing infrastructure rather than heavy new investments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 33 | 46 | 3 | +35.4% |

| 2024 | 24 | 40 | 26 | -0.4% |

| 2023 | 24 | 25 | 36 | -48.0% |

| 2022 | 46 | 59 | 21 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 17 | 43 | 12.2 |

| 2024 | 17 | 14 | 10.6 |

| 2023 | 17 | -11 | 10.7 |

| 2022 | 17 | 38 | 22.0 |

Source: SEC companyfacts cache [F1].

The results indicate WTBA’s capability to translate lender specialization into earnings momentum while reining capex aligns resources toward profitability.

Interest Rate Strategy and Risk Mitigation Tactics

WTBA implements comprehensive asset-liability management practices tailored to prevailing market conditions focusing heavily on mitigating interest rate risk arising from their liability structure—mainly deposits—and short-term wholesale funding.

The Company has adopted interest rate collars on deposits that enable offsetting payments contingent on index fluctuations between predetermined floors and caps [S10]. Moreover, all FHLB advances—amounting to approximately $270 million as of mid-2025—are one-month rolling short-term borrowings which are fully hedged through long-dated interest rate swaps maturing through mid-2029 at fixed contract rates from about 1.86% to 4.32% [S6][S10]. This hybrid instrument suite effectively converts otherwise floating-rate liabilities into cost-stable fixed-rate exposures.

Participation in reciprocal deposit networks further supports liquidity risk control by enhancing FDIC insurance coverage beyond single institution limits—a critical confidence builder for wholesale depositors wary of uninsured balances under volatile market scenarios [S6].

Liquidity Management: Balancing Deposits, Wholesale Funding, and Securities

Liquid assets management revolves around maintaining sufficient cash resources drawn primarily from core customer deposits augmented variably by brokered deposits which declined from over $266 million at end-2024 to about $205 million by September 2025 reflecting strategic balance sheet tuning [S10][S6]. Removing brokered deposits reveals modest organic core deposit growth supporting loan book expansion without overreliance on potentially more costly wholesale funding.

Loan repayments combined with proceeds from securities maturities also contribute regularly to liquidity buckets used to fulfill ongoing financial obligations or grow lending capacity dynamically.

At September-end 2025, cash combined with highly liquid securities including government agency-backed collateralized mortgage obligations approached $233 million along with additional borrowing capacity exceeding half a billion dollars via FHLB lines and Federal Reserve discount windows available as buffer instruments against unplanned liquidity stress [S4][S8].

Capital Allocation: Shareholder Returns Amid Rising Equity

Book equity rose strongly within FY2025 from approximately $228 million up to around $266 million driven by retained earnings accumulation balanced partially by unrealized losses netted through comprehensive income accounts reflecting market rate volatility effects on securities portfolios [F1][S8].

Dividends paid remained essentially flat around $16.9 million confirming steady payout discipline despite fluctuating earnings levels—the absence of share repurchases signals prioritization of capital adequacy over buyback-driven EPS accretion at this phase [F1][N3].

Approximate return metrics suggest an ROE near 12.2%, indicating competent capital utilization relative to peers given prevailing market conditions while comfortably exceeding minimum regulatory ratios evidenced by Tier 1 capital ratios above required conservation buffers at both consolidated entity and bank subsidiary levels per latest filings [F1][S20][S25].

Growth Opportunities and Operational Constraints Ahead

Management commentary underscores optimism about sustained growth potential anchored by steady deposit bases anchoring loan expansion opportunities primarily within existing regional markets [N8][S2]. Nonetheless, risk factors explicitly flagged include significant credit concentration risks especially within the commercial real estate sector which could exert pressure during economic contractions or valuation declines.

Furthermore, rapidly evolving regulatory landscapes coupled with increasing cybersecurity threats pose operational challenges requiring continual investment—increasingly complex given evolving technology adoption imperatives such as AI-enabled tools discussed abstractly within filings—but no major transformative IT rollout appears imminent based on available data [S12][N8].

Key Industry Dynamics Affecting Future Outcomes

WTBA competes within an Upper Midwestern regional banking context characterized by similar mid-sized institutions navigating deposit competition not just from banks but also non-bank entities such as credit unions and fintech platforms leveraging alternative delivery models with digital efficiencies often challenging traditional relationship models [N4][N5][N6].

Macro-level interest rate fluctuations remain critical determinants influencing net interest margins across the sector as seen in peer performance reports which show mixed earnings beats tied closely to effective hedging strategies vis-à-vis underlying funding cost volatility.

In this environment, WTBA’s demonstrated success balancing credit quality focus with efficient funding cost management lends credible resilience compared with peers subject to broader economic shocks.

What Investors Should Monitor Next

Though explicit guidance is absent, key metrics warrant close observation moving forward:

- Evolution of nonperforming assets ideally maintaining near-zero status given prior improvements.

- Loan portfolio seasoning effects especially commercial real estate segment underwriting standards tested against potential economic downturns.

- Shifts in deposit composition between core vs brokered components indicating funding stability.

- Net interest margin developments reflecting the interplay between asset repricing speed versus hedged liability costs.

- Regulatory actions or disclosures hinting at changes in allowance levels or credit loss provisioning requirements.

- Progress or delays in technological modernization initiatives impacting operational agility amidst growing fintech competition. Monitoring these factors can contextualize WTBA’s trajectory amid broader sector cyclicality while assessing sustainability of recent financial gains.

This analysis synthesizes reported facts and inferred industry context without providing investment advice or forecasts beyond disclosed statements.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments