Wenyuan Group Faces Critical Liquidity Challenges Amid Complex PRC Regulatory Environment

The latest quarterly filing reveals Wenyuan Group’s acute liquidity constraints and ongoing operating losses, exacerbated by regulatory and currency control issues in China that restrict financial flexibility and growth opportunities.

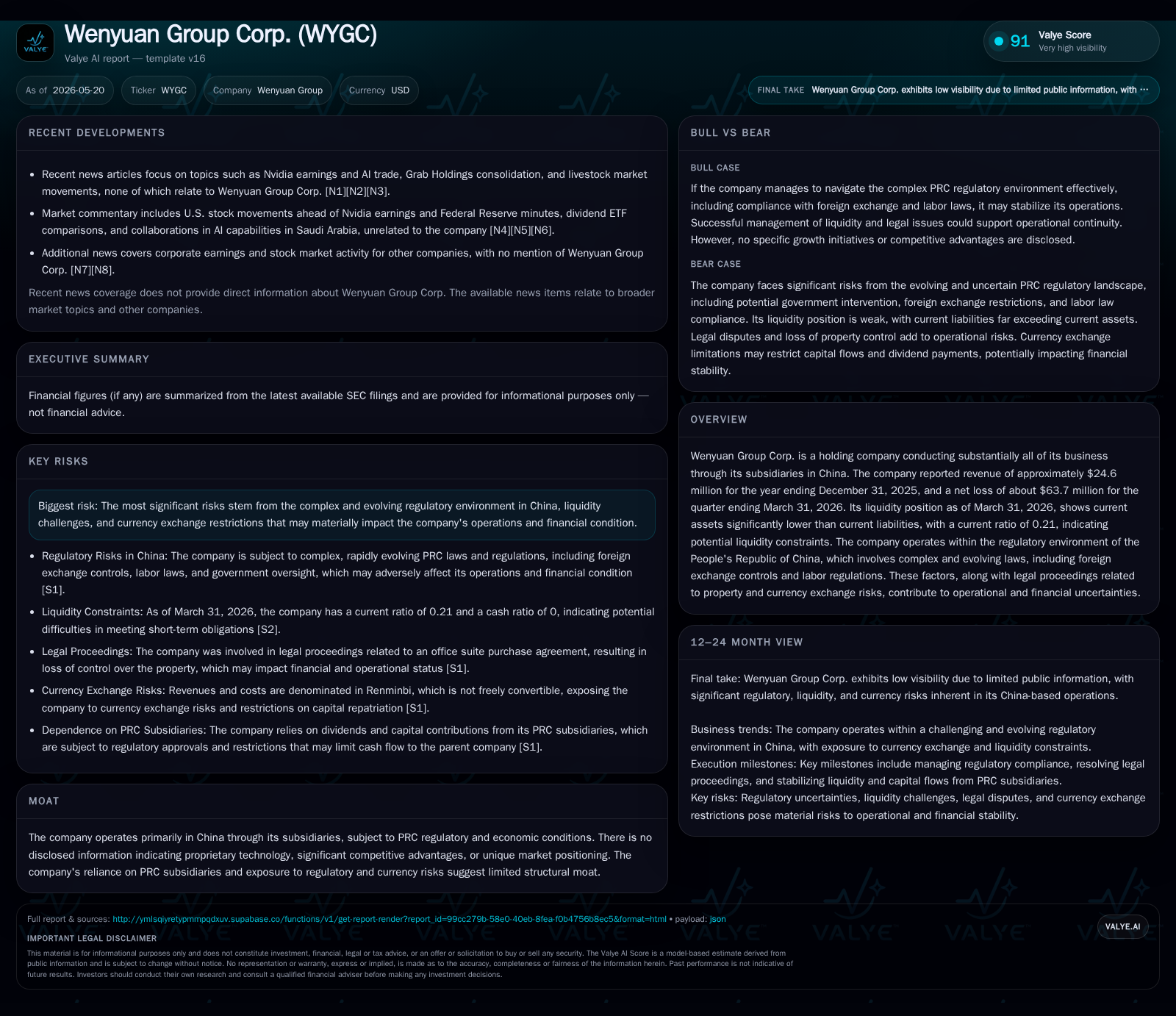

Wenyuan Group Corp.’s Q1 2026 results highlight severe liquidity pressure, with current liabilities vastly exceeding current assets and a sizable net loss. Operating as a U.S.-listed holding company relying on PRC subsidiaries, WYGC faces stringent foreign exchange restrictions and complex regulatory filing requirements that impede capital mobility and strategic initiatives. The absence of clear competitive advantages combined with legal disputes and evolving PRC regulatory oversight increase operational risks. Investors should monitor compliance with CSRC filing mandates, liquidity management efforts, and regulatory developments impacting cross-border capital flows.

Latest Quarterly Operating Update: Intensified Liquidity Pressure and Losses

Wenyuan Group Corp.’s Q1 2026 SEC filing [S2] reveals escalating financial distress through both profitability pressures and liquidity challenges. The company reported a net loss of approximately $63.7 million for the quarter, signaling steep operational difficulties during an uncertain market and regulatory backdrop [F1]. Concurrently, balance sheet data shows current assets of $27.3 million sharply contrasted by current liabilities exceeding $132 million as of March 31, 2026, resulting in a critically low current ratio near 0.21 [F1]. This imbalance highlights urgent short-term funding needs that could threaten ongoing operational continuity absent corrective measures.

Business Model: U.S.-Listed Holding Company Dependent on PRC Subsidiaries

Wenyuan operates primarily as a U.S.-listed holding company with its core business conducted through affiliated subsidiaries domiciled in China [S1]. Revenues totaled roughly $24.6 million for full-year 2025, primarily generated within these PRC entities [F1].

This structure introduces significant challenges due to China’s restrictive regulatory framework governing foreign investment vehicles. The company’s reliance on dividend remittances from Chinese subsidiaries exposes it to currency controls enforced by the State Administration of Foreign Exchange (SAFE), which tightly regulates RMB transfers converted from foreign currency loans or capital contributions made to subsidiaries [S9][S12].

Dividend distributions are also limited by statutory requirements mandating accumulated profits thresholds and reserve fund allocations before repatriation can occur [S11]. Loans extended from WYGC to its subsidiaries must not exceed statutory limits and require local SAFE registration. Noncompliance risks penalties that could disrupt operations.

These factors collectively constrain WYGC’s ability to efficiently allocate capital across borders and complicate its funding cycles given protracted approval processes.

Industry and Competitive Context: Regulatory Environment Dominates Competitive Dynamics

WYGC does not disclose proprietary technologies or significant product differentiation within its segments [S1]. Instead, its competitive positioning is defined predominantly by external regulatory conditions rather than conventional advantages such as scale or intellectual property.

Operating within China subjects the company to extensive government oversight encompassing evolving laws on investments, labor practices, intellectual property rights, and corporate governance—areas characterized by inconsistent enforcement and legal uncertainty [S16][S18]. These conditions are common among similarly structured firms lacking distinctive competitive moats.

Thus, WYGC’s industry positioning centers on navigating regulatory complexities rather than leveraging unique business strengths.

Growth Drivers: Regulatory Compliance as a Prerequisite for Expansion

Growth prospects hinge largely on successful management of regulatory approvals. Acquisition strategies must comply with MOFCOM’s Anti-Monopoly Law clearance requirements when turnover thresholds are met, potentially delaying or impeding expansion plans [S8].

Furthermore, recent CSRC mandates require domestic companies with contractual structures like WYGC’s to complete specific filings for overseas listings. Failure to comply may result in penalties that jeopardize access to capital markets essential for fundraising activities [S3][S10].

Currency convertibility restrictions further limit available funds for operational growth once foreign currency is converted into RMB within subsidiaries’ capital accounts [S9]. Consequently, organic or inorganic growth depends heavily on regulatory navigation rather than purely market-driven factors.

Key Risks: Regulatory Scrutiny, Currency Restrictions, Legal Exposure, and Financial Strain

WYGC faces significant PRC regulatory risk including potential adverse interpretations that could challenge its corporate structure’s compliance. Such outcomes might undermine control over subsidiary assets or dividend flows, risking substantial value impairment for shareholders [S16][S18]

Legal exposure includes litigation stemming from guarantees on third-party liabilities culminating in forced auction of an office suite asset—a material operational risk factor [S5]. Enforcement difficulties related to foreign judgments further compound uncertainty.

Currency controls restrict outbound RMB transfers critical for servicing debt or parent-level expenses; violations carry risk of severe penalties that would exacerbate operational challenges [S9][S12]

Coupled with liquidity stress revealed in Q1 2026 filings—current liabilities vastly exceeding liquid assets—these factors heighten the company’s financial vulnerability.

What to Watch: Compliance Milestones, Liquidity Management Efforts, and Regulatory Developments

Upcoming CSRC filing deadlines tied to overseas listing regulations will be pivotal in determining WYGC’s continued access to U.S. capital markets—a key source for equity fundraising or refinancing existing debt obligations [S3][S10]

Investor attention should focus on management disclosures regarding strategies to address liquidity shortfalls such as asset divestitures or creditor negotiations.

Resolution progress on legal disputes related to asset guarantees could materially affect financial risk profiles.

Additionally, indications of fresh capital injections into subsidiaries or approved acquisitions will provide insight into growth execution capabilities amid restrictive regulatory conditions.

Financial Summary: Negative Working Capital and Earnings Pressure Limit Flexibility

Latest publicly available data from filings and SEC Companyfacts indicate Wenyuan held minimal cash reserves of approximately $151K at quarter-end March 2026 against current liabilities exceeding $132 million—a pronounced negative working capital position unfavorable for sustaining operations without new funding sources [F1]

Total debt stood at about $14 million per earlier disclosures; combined with negligible cash balances this yields a net debt position exceeding $13 million. Ongoing quarterly losses compound erosion of financial buffers.

Given these metrics alongside stringent currency controls limiting upstream dividends or shareholder loans from PRC subsidiaries, near-term financial flexibility appears severely constrained requiring vigilant management oversight.

Disclaimer: This analysis is based solely on Wenyuan Group Corp.’s SEC filings through May 20, 2026 ([S1], [S2], etc.) and associated public numeric data ([F1]). It does not constitute investment advice but provides an informed operational assessment grounded in disclosed evidence.

Financial position in context

As of 2026-03-31, companyfacts shows $151 in cash and equivalents [F1]. Current assets of $27285 and current liabilities of $132003 imply a current ratio near 0.21x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments