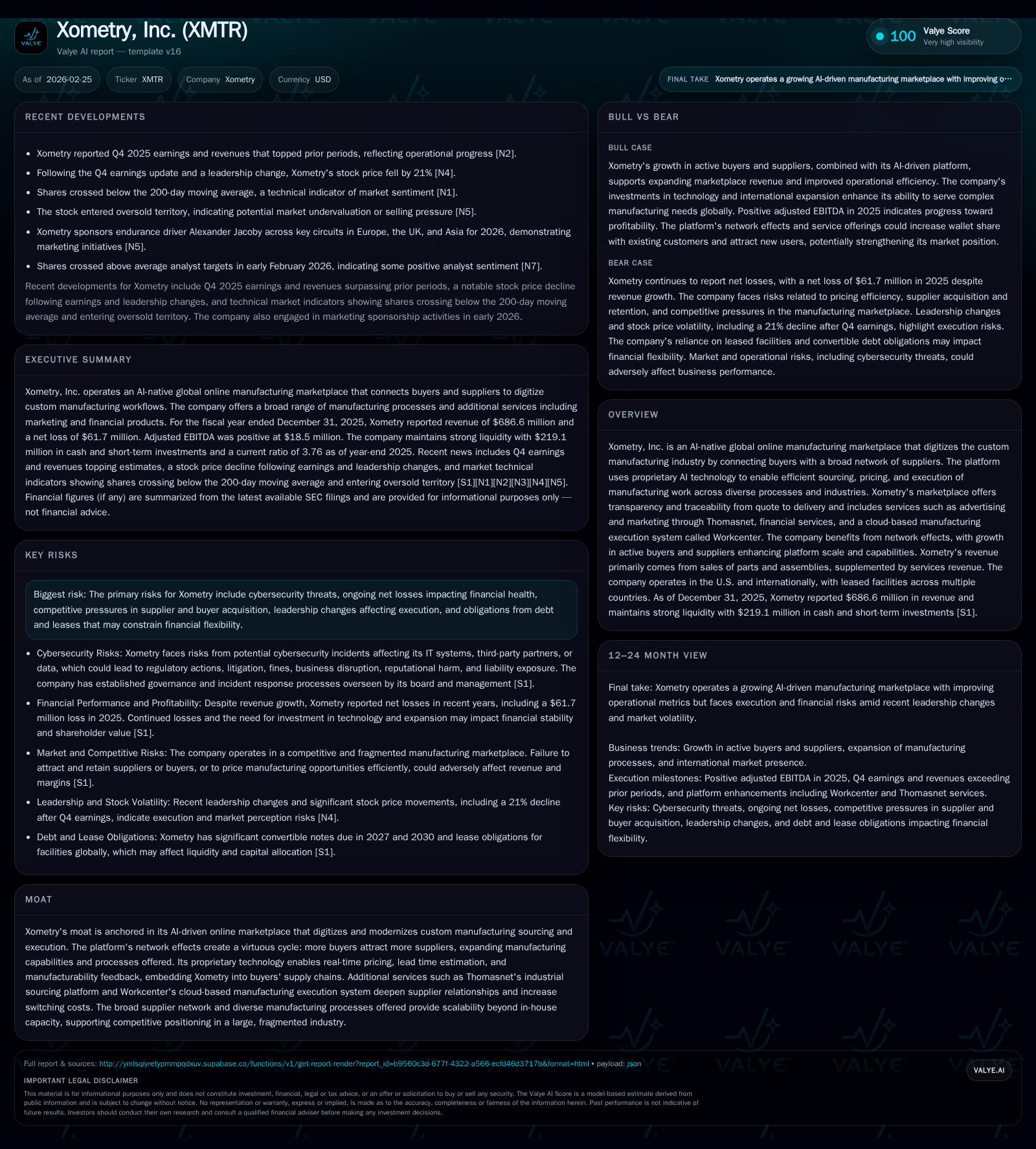

Xometry’s AI-Driven Platform Sparks Marketplace Expansion and Operational Pivot

Detailed analysis of Xometry’s growth trajectory, AI-driven marketplace dynamics, leadership changes, and capital strategy amid profitability challenges.

Xometry has leveraged its proprietary AI technology to drive substantial marketplace expansion, particularly in the U.S., with notable improvements in segment profitability. Despite growing operating losses, the company has improved adjusted EBITDA and cash flow from operations due to operational efficiencies and platform scaling. Leadership transitions and modest share repurchases underline a strategic pivot towards driving long-term profitability. Key risks include cybersecurity, competitive pressures, and debt obligations, while future progress hinges on sustaining network effects and advancing AI capabilities.

Evolution of Growth: Revenue Gains and Operating Income Trajectory

Xometry’s fiscal 2025 marked continued strong expansion in its digital manufacturing marketplace. Total revenue increased by 26% year-over-year to approximately $686.6 million from about $545.5 million in fiscal 2024 [S9][S10]. The revenue surge was largely propelled by a vigorous 30% increase in marketplace sales to approximately $629.6 million, driven predominantly by heightened buyer activity among enterprise customers located primarily in the U.S. [S10]. In contrast, services revenue experienced a slight contraction of 4%, reflecting declines in Thomas advertising and marketing services partially offset by gains in financial services [S10].

Operating income losses narrowed meaningfully from approximately -$56.1 million in fiscal 2024 to -$45.5 million in fiscal 2025 — representing an improvement of nearly 19% [F1]. This progress is a function of enhanced top-line growth outpacing expense increases alongside operating efficiencies realized through platform scaling.

Cash flow dynamics revealed a notable turnaround as operating cash flow improved by about 140%, delivering positive net cash provided of $6.1 million versus a negative $15.4 million the prior year [F1]. However, free cash flow remained negative at an estimated -$24.1 million when accounting for a sharp increase in capital expenditures (Capex) which jumped roughly 67% year-over-year to $30.2 million fueled by investments into internal-use software development related to platform enhancements [F1][S18][S22].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 6 | -46 | 30 | ||

| 2024 | -15 | -56 | 18 | ||

| 2023 | -67 | -30 | -74 | 18 | +11.3% |

| 2022 | -76 | -63 | -74 | 14 | -23.9% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -24 | |

| 2024 | -33 | |

| 2023 | -48 | -20.5 |

| 2022 | -76 | -20.3 |

Source: SEC companyfacts cache [F1].

*Revenue figures are derived from segment reporting as total revenue is not available from XBRL tags [S9] Note: Net income data is partially unavailable; no dividend information disclosed.

Artificial Intelligence Fuelling Marketplace Scaling and Gross Margin Dynamics

Central to Xometry's value proposition is its proprietary AI technology that automates pricing quotations and optimal supplier matching across its extensive manufacturing network [S6][S7][S10]. The AI-driven instant quoting engine leverages machine learning models trained on extensive historical data to deliver real-time pricing estimates balancing buyer budgets with supplier costs efficiently.

This capability supports competitive marketplace gross margin spreads, reflected by an increase in marketplace gross margin improving slightly to 34.7% for FY2025 from 33.5% for FY2024 despite accelerated growth favoring lower-margin marketplace business mix [S10][S14]. The platform’s matching algorithm enhances cost efficiency by dynamically routing orders to suppliers able to produce at optimal time and cost parameters.

Network effects form a reinforcing cycle where increasing active buyers attract more suppliers offering wider process capabilities — propelling further pricing precision improvements through richer data feeds into the AI system [S12]. These effects elevate switching costs as buyers embed Xometry's instant pricing feedback into supply chain planning.

Additional services including Thomasnet’s industrial sourcing advertising platform deepen supplier engagement, increasing retention through operational integration.

Geographic Footprint and Segment Performance Insights

Xometry operates two primary geographic segments: U.S., which dominates revenue share, and International markets showing robust growth but lagging profitability [S9]. For fiscal 2025, the U.S.-based segment generated approximately $574 million—up about 26% from $457 million the prior year—while International revenues rose nearly 27% to about $113 million [S9][S10].

Profitability contrasts sharply: the U.S segment posted positive Segment Adjusted EBITDA of $31 million compared with near break-even levels ($0.2 million) in the prior year [S8][S9]. Conversely, International segment Adjusted EBITDA remained negative at $(12.5) million though worsening slightly from $(9.8) million previously, signaling ongoing investment for market penetration with longer-term profitability goals.

The disparity highlights differing maturity stages where U.S operations benefit from entrenched networks while International expansion entails continued infrastructure investments.

Leadership Changes at the Helm: Strategic Implications

In February 2026, Xometry announced Sanjeev Singh Sahni as incoming CEO effective July 1, following Q4 earnings that triggered a >20% share price decline amid investor concerns over loss sustainability despite growth momentum [N3][S3]. Sahni’s appointment signals intent for strategic recalibration aimed at execution rigor amid intensifying competition.

Investor caution stems less from fundamental deterioration than uncertainty over turnaround timing and operating loss trajectory [N3][N2]. Management reiterated commitments to operational efficiency balanced with technology investments bolstering network effects and margins [N2]. Future performance will hinge on translating marketplace growth into sustainable profitability under new leadership.

Cybersecurity and Competitive Risks Amid Expansion

Cybersecurity is recognized as a material risk overseen by the Audit Committee with active involvement from CTO Vaidyanathan Raghavan and VP Information Technology Brendan Hamilton (CISSP certified) [S1]. Incident response protocols escalate critical events up to CEO level ensuring rapid response [S1]. Given reliance on digital connectivity for order routing and pricing algorithms, breaches could cause reputational damage and regulatory liability.

Competitive pressures persist on supplier acquisition across diverse manufacturing processes alongside buyer recruitment focused on enterprises [S4][N5]. Financial constraints arise from convertible notes exceeding $335 million maturing between 2027–2030 limiting flexibility [S8][S13][S28]. Managing these risks remains vital as Xometry scales internationally while refining profitability levers.

Capital Deployment: Cash Flow Trends, Capex Ramp-Up, and Share Repurchases

Capital allocation balances aggressive reinvestment with shareholder returns albeit modestly currently. Capex surged ~67% to $30+ million primarily for internal-use software development enhancing AI capabilities, cloud infrastructure scalability, and platform robustness supporting medium-term margin improvements but driving negative free cash flow despite positive operating cash flow [F1][S18][S22][S29].

Share repurchases totaled approximately $8 million during FY2025 via treasury stock buybacks funded partly through proceeds from June 2025 issuance of convertible notes raising net proceeds near $241 million—boosting liquidity without immediate dilution [F1][S24][S16][N12]. No dividends were paid aligning with growth-phase priorities favoring reinvestment over distributions.

The June 2025 issuance of low-coupon convertible senior notes due in 2030 finances expansion efforts while controlling financing costs but carries conversion features affecting long-term equity dilution potential [S13][S19].

Profitability Outlook and Market Expectations

Explicit forward guidance remains unavailable publicly; however, key metrics include active buyer/supplier counts supporting network effect strength alongside incremental non-GAAP profitability improvements such as adjusted EBITDA margin rising into positive territory (2.7%) during FY25 compared with prior negative margins (-1.8%) [N1][N2][S29].

Analysts should weigh accelerating top-line against ongoing GAAP net losses (~$61.7 million FY25) necessitating sustained operational discipline coupled with scalable technology execution [F1][S18]. The upcoming leadership transition introduces uncertainties balanced against strategic reset opportunities toward clearer path to profitability.

Note: Dividend data is not available from provided tags; approximate ROE calculated at -24.5%. Free cash flow is estimated as operating cash flow minus capex resulting in approx -$24.1 million for FY2025 based on tagged data [F1].

Disclaimer: This analysis is based solely on available regulatory filings and news disclosures through February 25, 2026; it does not constitute investment advice or recommendations regarding Xometry securities or other entities discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments