ZKH Group Ltd Struggles with Profitability but Advances MRO Platform and Fulfillment Infrastructure

ZKH’s latest quarter shows modest operational progress amid ongoing losses and strategic efforts in China’s emerging online MRO procurement market.

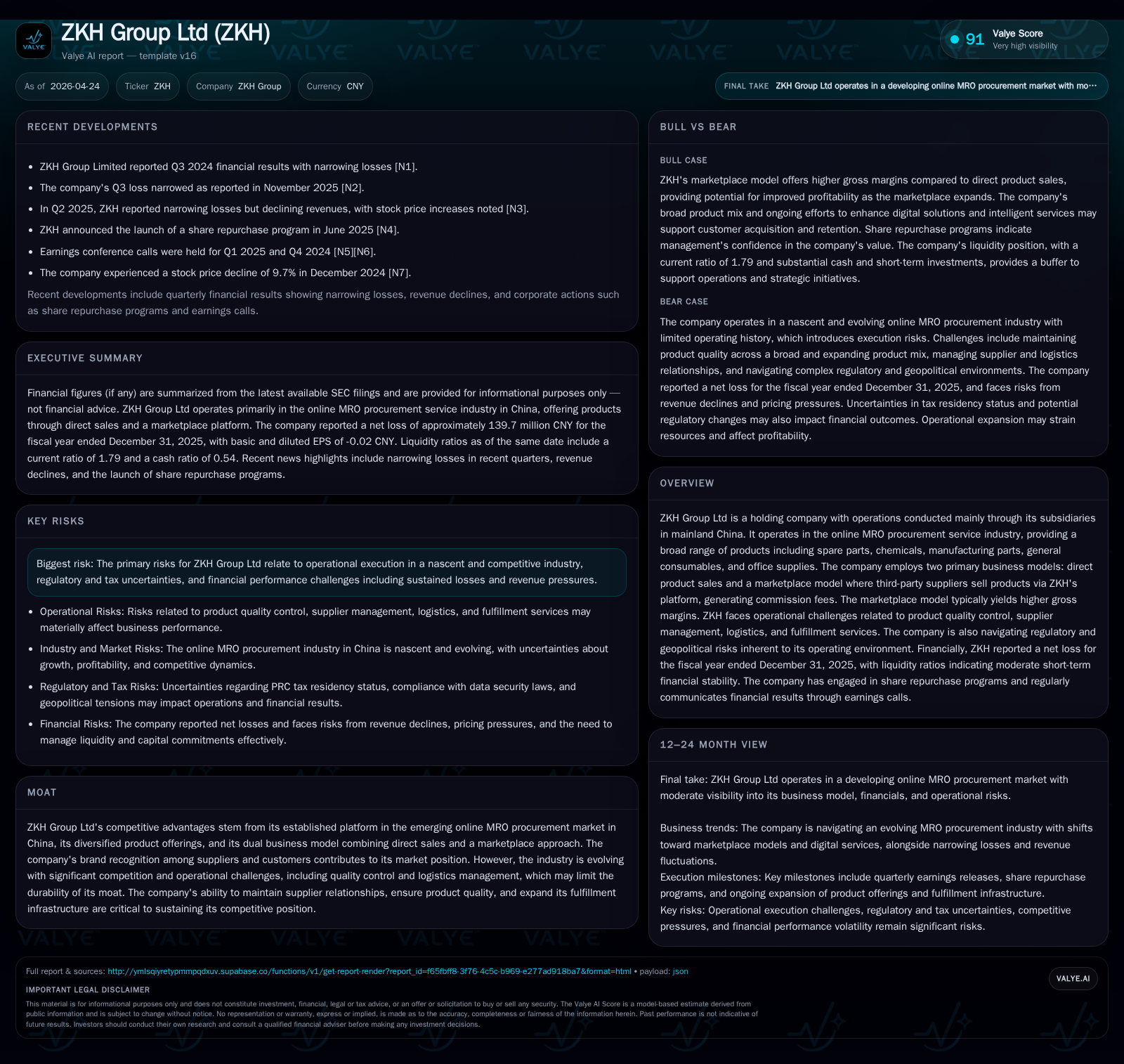

ZKH Group Ltd reported continued net losses for fiscal 2025, improving operating income yet still negative, underscoring persistent profitability challenges in a nascent but competitive Chinese MRO procurement industry. The company pursues growth by expanding its dual business model—direct product sales and a higher-margin marketplace—and investing in fulfillment facilities in industrial hubs to enhance delivery reliability and customer experience. However, operational complexities, quality control issues, pricing pressures, and evolving regulatory risks pose material constraints. ZKH’s solid liquidity position supports planned capital expenditures, including a committed industrial facility project aimed at bolstering technical support and quality assurance.

Recent Operating Update

ZKH Group Ltd filed its latest quarterly report on March 19, 2026 (6-K) confirming adherence to SEC reporting requirements without disclosing major operational changes or new forward guidance [S2]. The absence of event-driven updates signals a continuation of previously disclosed trends rather than abrupt business shifts. This filing anchors the current analysis by situating ZKH in a phase focused on steady execution amid outlining strategic priorities from the recent annual report dated April 24, 2026 (20-F).

Financially speaking for FY2025 ending December 31, ZKH reported an operating loss of RMB -213 million and a net loss of about RMB -140 million [F1]. These losses reflect improvement compared to the prior two years but still underscore ongoing challenges in reaching profitability. Operating cash flow slipped dramatically year-over-year by over 96% to approximately RMB 9 million while capital expenditures decreased by one-third to RMB ~53 million reflecting moderated investment activity possibly tied to cautious spending following substantial prior commitments [F1].

Business Model

ZKH operates primarily through subsidiaries located in mainland China delivering MRO (maintenance, repair, operations) procurement services via an integrated digital platform that encompasses two main business models:

- Direct Product Sales: ZKH purchases inventory for resale.

- Marketplace Model: Third-party suppliers list products on ZKH's platform; ZKH earns commission fees.

The marketplace model offers the advantage of higher gross margins due to reduced inventory risk and operational leverage from scale [S6]. Nonetheless, direct sales continue to comprise the majority of revenue as ZKH builds supplier networks. Product offerings span five broad categories: spare parts, chemicals, manufacturing parts, general consumables, and office supplies. Variations in product mix materially influence gross margin profiles – with lower-margin categories occasionally diluting overall profitability [S6].

Operationally, quality control is pivotal; third-party supplier quality issues can directly impact brand reputation given marketplace reliance. Managing supplier pricing inputs also affects customers’ trust since inaccurate or outdated pricing information leads to dissatisfaction [S18]. Moreover, logistics management is crucial as ZKH expands its fulfillment network with warehouses strategically located near China's major industrial clusters such as Taicang (Jiangsu Province), which houses a significant factory construction project aimed at enhancing technical support and quality assurance capabilities [S12] [F1].

Industry Structure and Competitive Position

China’s online MRO procurement sector remains relatively early-stage compared with mature e-commerce industries. It is characterized by fragmentation among suppliers and buyers coupled with rising adoption of digital platforms for indirect materials procurement. Competition is intensifying with multiple players vying on product breadth, price competitiveness, platform functionality, technological innovation (such as AI-based recommendations), and fulfillment reliability.

ZKH's competitive strengths include its established platform presence in this emerging market niche supported by brand recognition among suppliers and customers. Its dual business models enable revenue diversification while leveraging marketplace commissions for margin enhancement. The company also differentiates through developing fulfillment capabilities – adding direct control over delivery logistics distinguishes it from pure marketplace operators relying entirely on third parties [S13].

However, sustaining differentiation demands constant innovation in platform design (scalability, security), expansion into additional product categories (with attendant quality risks), and superior supplier relationship management. Industry competitors might undercut prices or offer broader value-added services such as integrated supply chain analytics or automated inventory replenishment – areas where ZKH must invest significant resources to maintain parity or edge [S21].

Growth Drivers and Constraints

Growth Drivers:

- Expanding Online Adoption: Increasing digitization among Chinese industrial buyers looking for streamlined procurement solutions supports structural demand.

- Fulfillment Infrastructure Expansion: Ongoing investments in warehouses like the Taicang facility aim to reduce delivery times and enhance customer experience—a critical driver for repeat purchase behavior.

- Marketplace Scaling: Growing supplier enrollment can improve product variety without proportional inventory risk.

- Technology Enhancements: Digital solutions such as intelligent recommendation engines may increase platform stickiness if successfully deployed.

Constraints:

- Profitability Challenges: Despite improved operating income trends (-37% YoY loss narrowing), sustained net losses highlight difficulties balancing growth investments with margin management [F1].

- Operational Execution Risks: Quality control over diverse suppliers is complex; failures can damage brand trust adversely affecting retention.

- Competitive Pricing Pressure: Market fragmentation causes downward pressure on prices risking margin erosion especially if commodity input costs rise unexpectedly.

- Regulatory Complexity: Ambiguity around licensing (e.g., value-added telecom licenses) plus evolving cybersecurity/data protection mandates impose compliance burdens that can increase costs or restrict certain activities [S4] [S8] [S24].

- Macroeconomic/Geopolitical Uncertainty: Trade tensions affecting commodity pricing or industrial activity could reduce demand volumes or disrupt supply chains.

What to Watch Next

Key milestones include progress on the Taicang facility construction which requires capital expenditures commitment (~RMB 273 million noted) mainly aimed at technical support and quality assurance functions—important for long-term operate leverage leverage gains [S12] [F1]. Other indicators include the pace of supplier additions to the marketplace platform reflecting growing ecosystem strength.

Management’s ability to sustain improvements in gross margin via shift toward marketplace sales is worth monitoring given its direct impact on earnings scalability. Also critical are developments in regulatory compliance that could either ease operational risks or bring unforeseen liabilities.

Customer behavior trends such as repeat order rates or complaint levels may offer leading signals regarding brand health amid quality challenges. Lastly, continued liquidity position will enable needed capex support but any adverse swings here could constrain growth initiatives given past operating cash flow volatility.

Financial Profile

ZKH's financial footing remains reasonably solid despite persistent losses:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -140 | 9 | -213 | 53 | +47.9% |

| 2024 | -268 | 229 | -339 | 79 | +11.9% |

| 2023 | -304 | -568 | -399 | 50 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 41 | -44 | -4.8 |

| 2024 | 41 | 150 | -8.7 |

| 2023 | -618 | -9.5 |

Source: SEC companyfacts cache [F1].

Cash & equivalents totaled approximately RMB 1.03 billion year-end 2025 versus minimal total debt (45 million RMB), positioning net debt significantly negative ( -986 million RMB), indicative of strong liquidity headroom supporting investment plans [F1]. Capital commitments notably include large factory construction funding alongside ongoing operating lease payments primarily for office space [S1].

The trajectory shows consistent narrowing of operating losses suggesting early positive impact from scale efficiencies or cost rationalization yet free cash flow remains negative after capex investment indicating continuing need for financial discipline moving forward.

Conclusion

ZKH Group Ltd inhabits a challenging yet potentially rewarding segment within China’s burgeoning online MRO procurement ecosystem. Its dual business model provides flexibility but also exposes it to complex operational risks especially around supplier management and logistics fulfillment. The move toward scaling marketplace sales aligns well with margin improvement goals but is offset by competitive pressures and volatile input costs.

The company’s commitment to expanding fulfillment infrastructure represents strategic safeguarding against logistics failures which are known pain points industry-wide but impose capital intensity during build-out phases. Regulatory uncertainty requires vigilant compliance efforts given evolving PRC standards impacting internet-based commerce operators.

Ultimately, sustainable growth hinges on achieving reliable quality controls across an expanding supplier base while successfully integrating innovative digital solutions tailored to industrial customers’ evolving demands. ZKH’s financial posture enables ongoing investments but profitability remains elusive requiring scrutiny of future execution effectiveness against sector headwinds.

This analysis is based exclusively on publicly available securities filings up to April 24, 2026 ([S1]-[S28]) consolidated with financial data ([F1]) and recent quarterly disclosures ([S2]). It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments