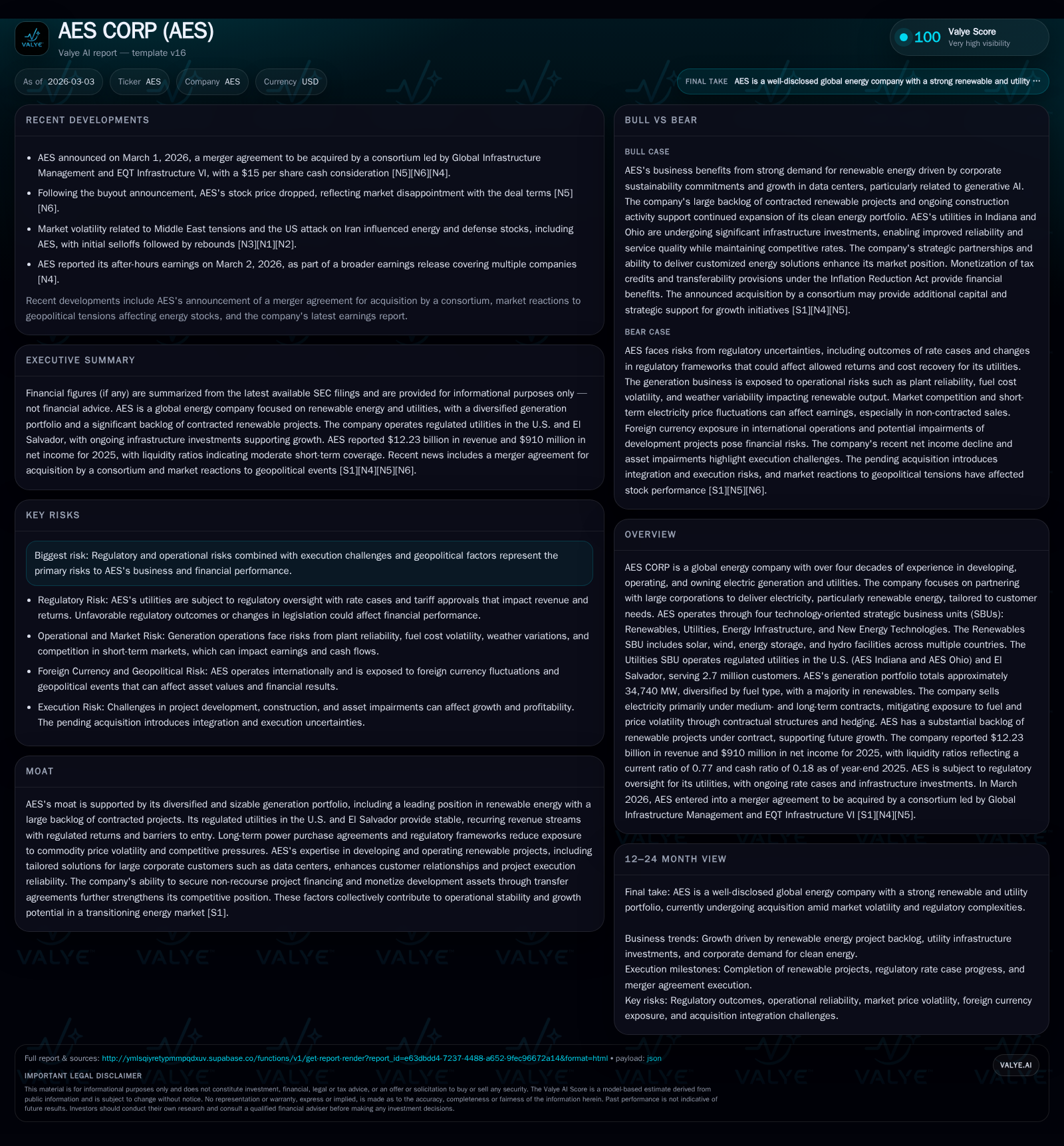

AES CORP’s Strategic Transformation: From Coal Monetization to Renewable PPAs and Utility Rate Base Growth

The company’s net income declined notably in 2025 amid coal asset transitions, yet a robust renewables backlog and accelerating utility rate base growth frame its forward trajectory.

In 2025, AES CORP reported a sharp net income decline primarily due to coal plant monetization, derivative losses, and foreign currency impacts, while renewables and utilities segments demonstrated strong expansion supported by long-term contracts and increased demand from data centers. The renewables backlog surged to 12 GW with 5.7 GW under construction, reinforcing AES’s leading position in corporate renewable PPAs. Utilities delivered record double-digit rate base growth through regulatory approvals, driven importantly by investments aligned with data center electricity demand. Operating cash flow improved substantially despite flat consolidated revenue, reflecting operational efficiencies and tax credit monetization. Risks persist around regulatory changes and geopolitical instability, requiring close monitoring of project execution and contract conversions.

Historical Revenue and Profit Trends Reflecting Portfolio Changes

AES CORP's financial profile in FY2025 reflects a transitional narrative between legacy coal asset wind-downs and growth engines in renewables and utilities. Consolidated revenue was essentially flat at $12.23 billion compared to $12.28 billion in FY2024 [F1], masking significant variances within strategic business units (SBUs). While Renewables revenue rose by 11% to $2.91 billion driven by new projects placed in service and improved hydrology, Utilities grew revenues 14% to $4.12 billion powered by increased transmission, distribution, wholesale rates, and retail demand improvements linked to favorable weather conditions [S1][S4]. In contrast, Energy Infrastructure revenue decreased by 13% ($805 million) largely due to the absence of prior year gains from Warrior Run coal PPA monetization and lower derivative gains [S1][S4]. The net impact was an operating margin decline of about 4%, illustrating margin pressures from asset impairments at AES Clean Energy related to sales-type leases initiation and foreign currency transaction losses.

Net income fell sharply from $1.68 billion in FY2024 to $910 million in FY2025 (-46%) largely attributable to the prior-year gain on sale of AES Brasil ($351 million), asset impairments ($224 million), higher unrealized foreign exchange losses ($79 million), loss of coal-related earnings streams, as well as derivative losses impacting Energy Infrastructure [F1][S1]. Yet adjusted EBITDA rose by $232 million reflecting solid contribution growth in Renewables and Utilities.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | Capex ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 12.2 | 910 | 4.3 | 5.9 | -0.4% | -45.8% |

| 2024 | 12.3 | 1679 | 2.8 | 7.4 | -3.1% | +574.3% |

| 2023 | 12.7 | 249 | 3.0 | 7.7 | +314.0% | +127.6% |

| 2022 | 3.1 | -903 | 2.7 | 4.6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 501 | -1.6 | 22.4 |

| 2024 | 483 | -4.6 | 46.1 |

| 2023 | 444 | -4.7 | 10.0 |

| 2022 | 422 | -1.8 | -37.1 |

Source: SEC companyfacts cache [F1].

Table summarizes AES annual financial trends noted above [F1]

Renewables Backlog and Corporate PPAs: The Core Growth Engine

AES's Renewables segment underscores the company’s strategic pivot toward carbon-free generation with a vast contracted pipeline totaling approximately 12 GW of projects at December 31, 2025—of which around half (5.7 GW) are currently under construction [S6]. This backlog solidifies AES as a top global seller of renewable power via power purchase agreements (PPAs), particularly concentrated in high-demand sectors such as U.S.-based hyperscale data centers deploying generative AI workloads [S10][S14]. These PPAs typically span medium- to long-term durations with creditworthy counterparties, affording revenue predictability.

Tax credit monetization under U.S. federal mechanisms such as the Inflation Reduction Act (IRA) plays an integral role in enhancing project economics through investment tax credits (ITCs) and production tax credits (PTCs), some transferred directly to tax equity investors or buyers under transferability provisions [S14][S18]. Plant availability metrics remain critical given the intermittent nature of solar and wind resources; thus effective storage integration adds dispatch flexibility.

The Renewables SBU generated increased operating margins (+26%) reflecting mature contract structures that limit exposure to spot market pricing volatility while benefiting from inflation-indexed contract escalators [S1][S6]. With active development pipelines exceeding $12 billion in capital requirements for upcoming plants alone [S6], progress on Construction-to-Operation conversion rates will be vital.

Expanding Utilities SBU: Capturing Data Center-Driven Demand

AES’s Utilities business now serves approximately 2.7 million customers across U.S. states Indiana & Ohio plus El Salvador utilities [S24][S25]. The U.S utilities—AES Indiana (integrated generation & distribution) and AES Ohio (transmission & distribution)—are undergoing their fastest period of rate base expansion historically supported by regulatory approvals including multi-year Integrated Resource Plans (IRPs) filed with state commissions [S6][S9]. Through mid-2020s filings with bodies like the Indiana Utility Regulatory Commission (IURC) and Public Utilities Commission of Ohio (PUCO), AES secured authorizations for transmission/distribution rider revenues alongside base rate increases designed to fund necessary grid modernization linked tightly with accelerated electricity consumption from advanced manufacturing sites and burgeoning data center clusters sited in their service regions [S6][S17].

Strategic site positioning near fiber optic networks combined with ample land/water resources creates natural advantages for attracting hyperscale data centers seeking renewable energy at scale [S6]. Smart Grid Phase initiatives underway at AES Ohio reflect proactive modernization aligned with reliability standards mandated via performance-based regulation frameworks [S17]. The utilities collectively provide steady cash flow streams insulated from commodity price swings via regulated tariffs that permit recovery of prudent capital expenditure plus allowed returns on invested capital assets [S24][S28].

Energy Infrastructure's Transition and Margin Pressures

The Energy Infrastructure SBU is navigating an inflection point whereby conventional fossil-fuel generation assets—primarily coal plants—are being monetized or phased out creating headwinds for revenue streams once boosted by transactional PPA monetizations like those from Warrior Run coal assets realized prominently during prior years [S1][S4]. Revenues declined by $805 million (-13%) reflecting both lower coal-derived cash flows and reductions in mark-to-market derivative gains tied partly to hedging activities.

Fuel pass-through cost elements—chiefly rising natural gas prices—alongside steadily evolving generation dispatch economics have compressive effects on margins as slower-growing gas-fired plants assume more flexible roles supporting grid stability amid increasing variable renewable penetration [S27]. Furthermore, unhedged exposure combined with restricted legacy contract extensions adds transition risk variability here.

Driving forward a diversified fuel mix portfolio whilst maintaining availability commitments remains central as AES balances energy security demands while advancing decarbonization targets through integration with Renewables SBU efforts.

Capital Allocation, Cash Flow, and Shareholder Returns Overview

Despite static top-line performance year-over-year (-0.4%), AES notably increased operating cash flow by +56.5% to $4.31 billion reflecting efficient operational execution coupled with tax credit transfers related primarily to renewable energy projects that enhance non-cash accounting benefits under GAAP rules [F1][S1][S18]. Capital expenditures moderated by nearly one-fifth (-19.8%) from $7.39 billion in FY2024 down to approximately $5.93 billion consistent with staged progression out of heavy upfront developmental phases toward construction completion across renewables programs as well as measured utility investments focused on system upgrades rather than large greenfield expansions [F1][S22].

Dividend distributions held steady at around $0.5 billion annually showing commitment to predictable shareholder returns amid ongoing strategic transformation; however no material repurchase activity has been observed recently evidencing prioritization of capex over buybacks given growth opportunities available [F1]. Equity capital swelled modestly over recent periods reaching approximately $4 billion at end-FY2025 helping sustain an estimated return on equity near a robust ~22% despite net income declines caused mainly by one-off impairments rather than core margin erosion [F1]. Free cash flow generation remains challenged due to elevated capex but is expected to improve as development pipelines mature into operations.

Regulatory Environment and Operational Risks Impacting Growth Trajectory

AES acknowledges several principal risk vectors including regulatory outcome volatility where allowed rates of return or cost recovery mechanisms may be subject to revisions across multiple jurisdictions encompassing Indiana’s IURC reviews or PUCO’s ongoing distribution rate proceedings including appeals pending before state Supreme Courts concerning rider designations affecting tens of millions in annual revenue streams [S16][S17]. Commodity price hedging mitigates fuel cost risks but cannot fully insulate against disruptions triggered by geopolitical events such as ongoing Middle East tensions affecting energy markets generally seen during early March ’26 trading sessions following US-Iran military escalations driving cautious investor sentiment toward energy stocks including AES exposures highlighted recently in market reports [N4]-[N7].

Operational execution risks arise chiefly from managing rapid build cycles underlying the sizeable renewables backlog coupled with development-to-construction transfers requiring sophisticated project management expertise amidst supply chain constraints per industry norms; delivery delays or cost overruns would weigh on adjusted EBITDA projections absent mitigating contingencies built into contractual agreements allowing remedy options through negotiated extensions or liquidated damages clauses typically included within project contracts [S16][N13].

Currency exposures remain material given international footprint spanning Latin America, Eastern Europe, and Asia necessitating vigilant foreign exchange risk management policies especially when cross-border tax credit financing mechanisms are involved.

What Investors Should Track Going Forward

With AES lacking explicit multi-year financial guidance post-FY2025 release other than broad strategic milestones articulated publicly, key monitoring metrics will revolve around conversion efficiency—defined as effective transition rates from signed PPA-backed pipeline projects into commercial operation status—and the pace with which incremental renewable megawatt hours translate into stabilized cash flows thus underpinning future adjusted EBITDA growth trajectories [N1][N2]. Regulatory docket outcomes including timely completions of IRP approvals filed at AES Indiana for continued resource planning alongside PUCO adjudications regarding electric distribution expressions for AES Ohio bear significant implications on permitted rate base capitalization limits bolstering utility earnings visibility.

Data center electricity demand trajectories nationally will serve as pivotal barometers influencing incremental infrastructure spend appetite beyond currently approved plans given early indications suggest faster-than-feared adoption curves driven by generative AI applications requiring more power-intensive compute capabilities elevating sustainable electricity procurement priorities within these hyperscale environments [S6][N13]. Moreover, commodity price exposure mitigation effectiveness especially amid potential volatility spikes impacting natural gas markets should remain front-burner topics alongside any potential new financing structures or asset-level M&A catalysts arising from announced acquisition plans involving global infrastructure funds.[N13]

In summary, AES CORP straddles a blend of near-term earnings headwinds arising from legacy coal transitions while simultaneously capitalizing on dynamic secular tailwinds stemming from ESG-driven renewables expansion backed by long-term contracted volumes complemented by regulated utility growth embedded within stable tariff regimes enhanced by evolving technology customer demand profiles.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments