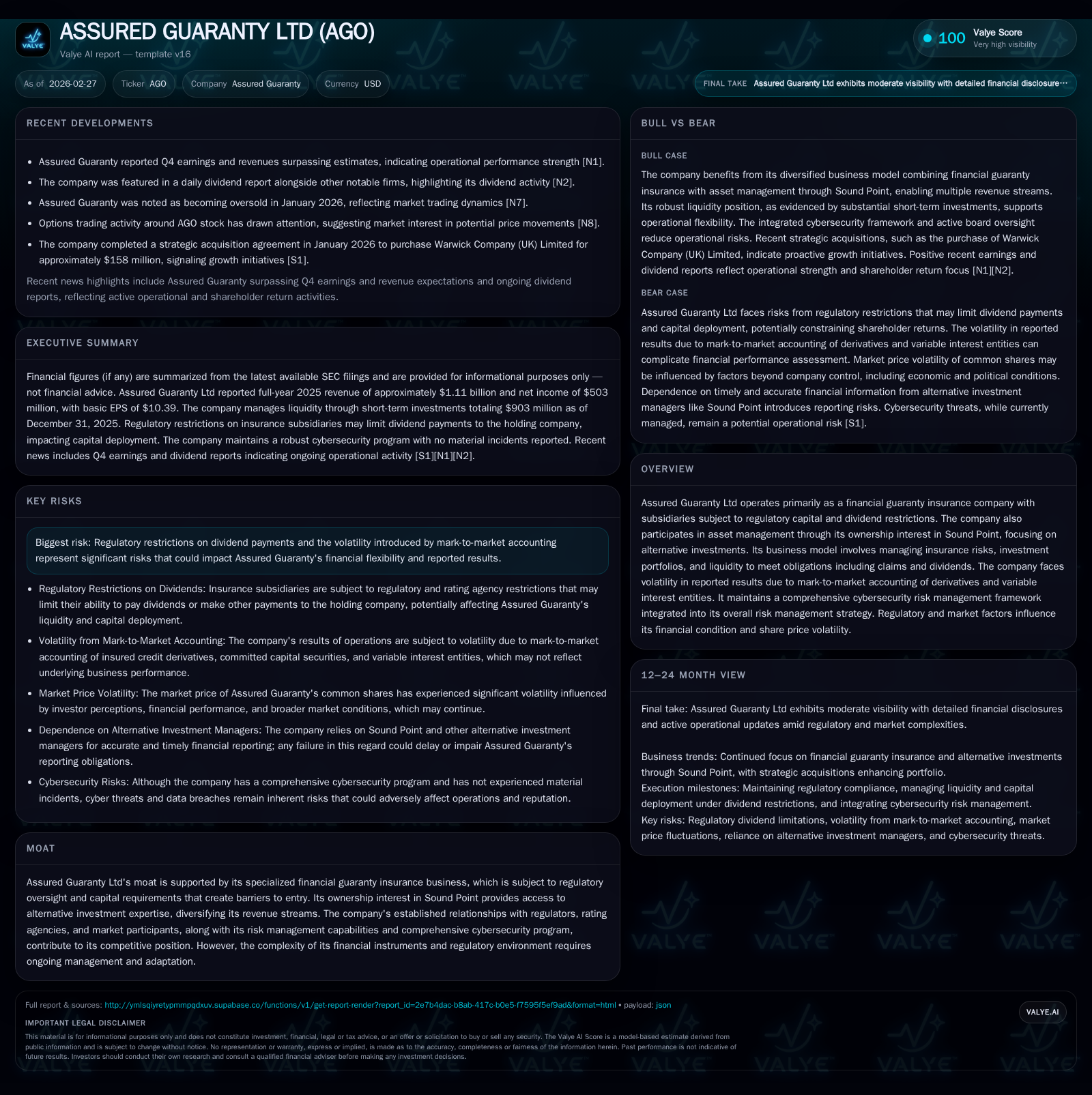

Assured Guaranty Ltd Shows Resilient Financial Growth and Navigates Regulatory Complexities

Assured Guaranty's 2025 performance reflects strong financial recovery, disciplined capital allocation, and proactive management of regulatory dividend constraints.

In 2025, Assured Guaranty Ltd (AGO) posted a robust 27.3% revenue increase to $1.11 billion and a 33.8% net income rebound to $503 million, signaling recovery following 2024's earnings dip. The company’s dual focus on financial guaranty insurance and expanding alternative investments via its Sound Point partnership drove growth amid mark-to-market volatility inherent to derivative valuations under regulatory accounting standards. Dividend restrictions across multiple jurisdictions continued to limit capital return flexibility, compelling AGO to emphasize large share repurchases over dividends in capital deployment. Liquidity and debt management remained sound despite exposure risks tied to evolving regulatory and market conditions. Looking ahead, tight dividend capacity and complex regulatory approvals constitute key factors shaping AGO’s strategic financial trajectory in 2026.

Steady Revenue and Income Recovery: Examining Assured Guaranty’s Recent Growth Drivers

Assured Guaranty Ltd (AGO) demonstrated a notable rebound in fiscal year 2025 after encountering earnings pressure in 2024. Full-year revenue climbed sharply by 27.3% to $1.11 billion from $872 million in the prior year, recovering from a significant dip seen in FY2024 that had followed a strong FY2023 peak at $1.37 billion [F1]. This recovery primarily stemmed from improved underwriting results within its core financial guaranty segment complemented by favorable investment income dynamics amidst a fluctuating market environment [N1][N2]. Net income likewise surged by 33.8% year over year to $503 million in FY2025 from $376 million the previous year, demonstrating enhanced operational profitability despite ongoing volatility inherent to the business model [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1110 | 503 | 0.3 | +27.3% | +33.8% |

| 2024 | 872 | 376 | 0.0 | -36.5% | -49.1% |

| 2023 | 1373 | 739 | 0.5 | +89.9% | +496.0% |

| 2022 | 723 | 124 | -2.5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 68 | 500 | 8.9 |

| 2024 | 68 | 502 | 6.8 |

| 2023 | 67 | 199 | 12.9 |

| 2022 | 64 | 500 | 2.4 |

Source: SEC companyfacts cache [F1].

Source: Company filings and data consolidated from latest available annual reports [F1]

Earnings Volatility Driven by Mark-to-Market Accounting

Despite operational improvements underlying AGO's core business, reported earnings exhibit significant volatility largely attributable to mark-to-market accounting on derivatives and variable interest entities (VIEs). These accounting treatments require AGO to adjust the fair value of certain financial instruments each reporting period based on fluctuating market prices rather than economic realizable value or expected ultimate cash flows [S1][N1]. Such swings can distort periodic earnings visibility even when underlying operational trends remain stable.

This dynamic is especially pronounced within the financial guaranty insurance space where AGO insures portfolios sensitive to macroeconomic shifts and credit cycles; derivative valuation changes may trigger sizeable fluctuations independent of premiums earned or claims paid [S4]. Management addresses this through comprehensive risk management frameworks incorporating scenario analyses consistent with rating agency capital models and regulatory considerations.

Alternative Investments Expansion: Capitalizing on Sound Point Partnership Risks and Rewards

A strategic pillar underpinning recent growth has been AGO's emphasis on alternative credit investments via its majority ownership interest in Sound Point Capital Management [S6][S7]. As the company seeks incremental yield beyond traditional fixed income markets amid low rate environments, expanded allocations into alternative asset classes diversify its risk exposure while improving return potential.

Sound Point operates as an exclusive alternative credit manager for AGO's funds with mandates covering collateralized loan obligations (CLOs), direct lending strategies, and opportunistic credit funds — all aiming at enhanced risk-adjusted returns through active credit selection and market timing expertise [N1]. However, these alternatives introduce additional risk dimensions including reduced liquidity compared to public markets, heightened credit default risk particularly during economic downturns, as well as reputational risks linked to complex structured instruments [S6][S7]. The company mitigates these through rigorous due diligence protocols coupled with internal portfolio oversight functioning alongside external manager governance.

Regulatory Dividend Restrictions Impacting Financial Flexibility

Regulatory capital rules across Bermuda (AGO's domicile), the U.K., France and certain U.S. states restrict the timing and quantum of dividends payable by AGO’s insurance subsidiaries — legal entities that generate earnings used upstream for dividends or share repurchases at the holding company level [S1][S4][S8]. These jurisdictions impose limits designed to maintain insurer solvency by requiring retention of substantial statutory surplus beyond prudentially necessary levels.

Consequently, normal payout capacity is constrained absent regulator waivers or relief measures; subsidiaries may be forced to retain excess capital even when management contends it exceeds business needs [S12]. This restriction reduces liquidity available for discretionary capital returns creating tension between shareholder return objectives and compliance obligations.

Capital Allocation Trends: Balancing Strong Buybacks With Conservative Dividends

Reflecting regulatory constraints on dividends but a continued commitment to returning cash efficiently to shareholders, AGO maintained relatively flat dividend payments around $68 million annually in FY2025 compared with prior years while executing substantial share repurchases totaling roughly $500 million — nearly matching the record pace set in FY2024 [F1][N2][S23][S25]. This pattern illustrates managerial pragmatism: dividend growth potential remains capped by insurance law while repurchases offer flexibility for adjusting capital return pace without immediate regulatory approval delays.

Operating cash flow strengthened markedly in FY2025 to $259 million (451% increase YoY), albeit still below peak levels seen pre-2024 disruption — underscoring improved internal cash generation supportive of continued buyback programs alongside prudent balance sheet management [F1].

Liquidity Profile and Debt Management Amidst Market Uncertainties

AGO’s liquidity strategy centers on maintaining diversified sources including positive operating cash flow generated by insurance operations; income distributions from Sound Point’s alternative assets; access to external financing markets; holdings of liquid securities; and proceeds from asset sales when necessary [S6][S7][S13]. Despite these layers of support, the firm recognizes ongoing risks such as asset/liability mismatches prevalent in annuity reinsurance contracts which demand close monitoring given potentially volatile liability durations relative to asset maturities.

The company maintains several debt tranches differing in maturities stretching into the early-2030s or beyond offering durable capital base buffer with manageable refinancing requirements noted in recent disclosures [S3]. Nonetheless, unexpected claim payments or material revisions in regulatory capital calculations could pressure liquidity necessitating contingency capital planning.

Watchlist for 2026: Key Milestones and Risk Factors To Monitor

Investors evaluating AGO should observe developments across several dimensions:

- Progress on obtaining regulatory approvals related to dividend increases or expanded buyback authority will materially influence financial flexibility [N1][N2].

- Rating agency reviews by Moody’s & S&P impacting insurance subsidiary ratings can affect new business volumes and pricing power given reliance on high credit quality designations [S4].

- Outcomes of ongoing litigation connected with distressed obligor restructurings remain unpredictable but could influence expected loss reserves or cash flow profiles [S10].

- Taxation developments arising from OECD BEPS adjustments or U.S./U.K. tax code modifications may alter net profitability metrics over time [S22].

- Cybersecurity threats persist as an operational risk area requiring continual investment aligned with evolving regulatory expectations globally [S16].

- Any significant shifts in market interest rates or credit spreads impacting mark-to-market valuations of derivatives or alternative investments carry notable earnings implications requiring vigilant management oversight.

AGO's narrative underscores balancing rigorous regulatory adherence while deploying capital strategically through diversified businesses amid inherent earnings variability—key themes shaping its trajectory into the coming year.

This analysis is prepared solely for informational purposes without any expressed or implied recommendation concerning securities mentioned herein. Readers should consult their own professional advisors before making any financial decisions related to Assured Guaranty Ltd.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments