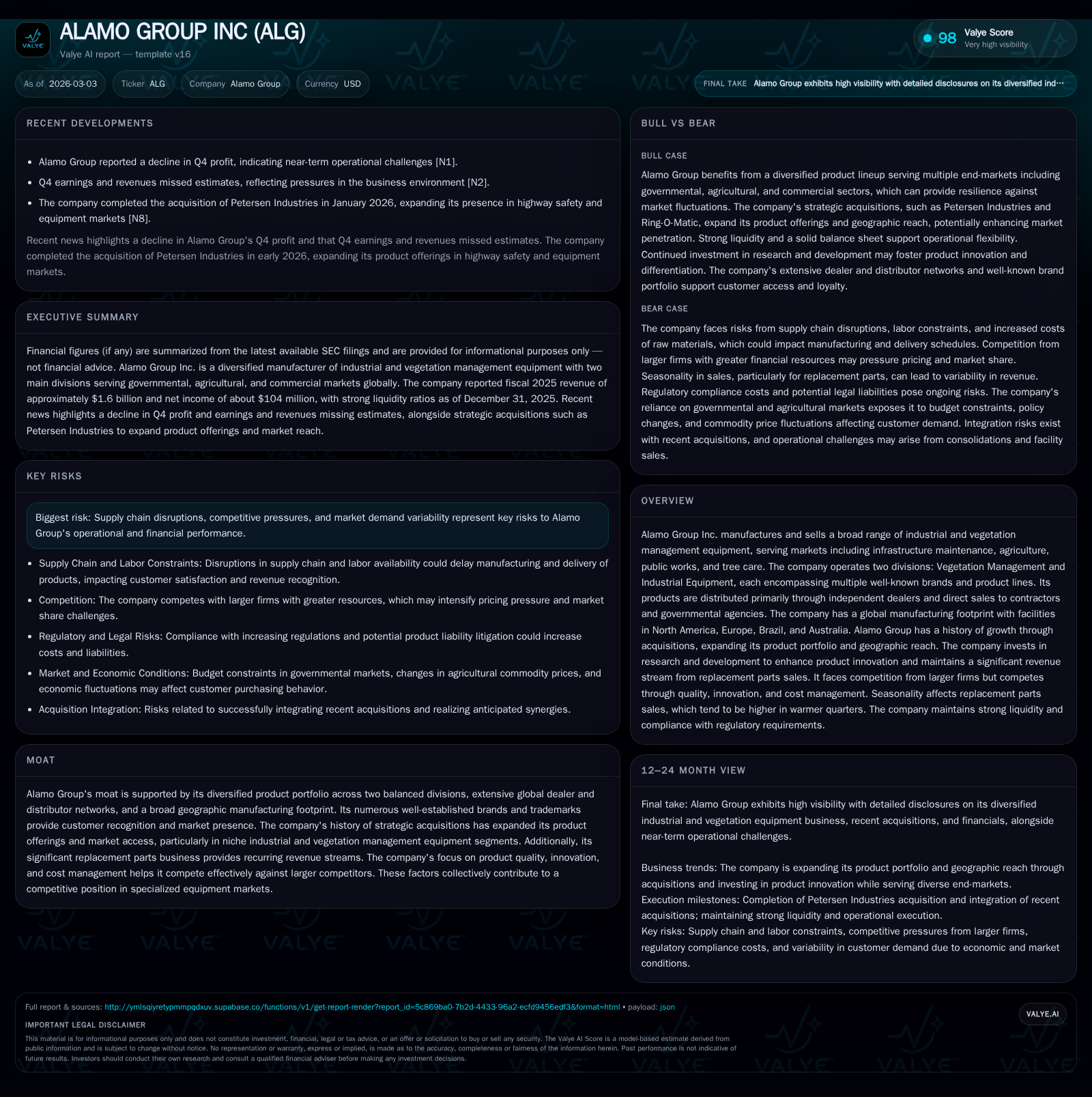

Alamo Group's Steady Footprint Amid Evolving Industrial Equipment Markets

Alamo Group blends a broad industrial and vegetation management product portfolio with disciplined capital allocation amid recent operational challenges.

Alamo Group Inc. has established itself as a diversified manufacturer of vegetation management and industrial equipment, operating globally with 27 manufacturing facilities and nearly 3,800 employees. Its growth through targeted acquisitions and product innovation has expanded its market reach, although profitability contracted in 2025 alongside a modest revenue decline. Operational pressures, including competitive dynamics and supply chain constraints, contributed to a recent earnings miss, underscoring risks ahead. The company maintains solid cash flow generation and a conservative capital return approach, supported by a robust balance sheet with a current ratio of 4.57.

Historical Revenue and Profit Trends Reflecting Product and Market Diversification

Alamo Group's financial trajectory over the four fiscal years ending 2025 underscores a broadly steady but slightly declining revenue base paired with more pronounced profit variability [F1]. Revenues reached $1.60 billion in FY2025, down by about 1.5% from $1.63 billion in FY2024. Operating income fell more sharply by approximately 8% year-over-year to roughly $152 million, while net income declined by 10.5% to near $104 million. This divergence suggests margin pressures that could be linked to cost inflation or operational inefficiencies.

Operating cash flow remained positive though it contracted by around 15%, from roughly $210 million to $178 million. Meanwhile, capital expenditures increased by over 22% to $30.6 million, indicating ongoing investments in manufacturing capabilities or product development.

Alamo’s two main segments—the Vegetation Management Division and the Industrial Equipment Division—represent balanced but distinct product offerings [S6][S8]. Vegetation Management brands like Rhino®, Bush Hog®, McConnel®, Bomford®, and Morbark® cater to agricultural, forestry, and municipal markets globally using technologies such as rotary cutting, flail mowers, hydraulic boom mowers, and wood chippers. The Industrial Division offers vocational trucks (e.g., Royal Truck & Equipment®), excavators through Gradall®, street sweepers via Schwarze®, vacuum trucks under VacAll® and Super Products®, alongside snow removal equipment brands like Tenco® and RPM Tech™.

Replacement parts sales consistently contributed approximately 16-17% of revenues from 2023 through 2025—a testament to the company's effective aftermarket positioning sustaining recurring income from installed base machinery [S7][S8][F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1604 | 104 | 178 | 152 | -1.5% | -10.5% |

| 2024 | 1629 | 116 | 210 | 165 | -3.6% | -14.9% |

| 2023 | 1690 | 136 | 131 | 198 | +11.6% | +33.6% |

| 2022 | 1514 | 102 | 15 | 149 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 14 | 3 | 147 |

| 2024 | 12 | 2 | 185 |

| 2023 | 10 | 1 | 93 |

| 2022 | 9 | 1 | -17 |

Source: SEC companyfacts cache [F1].

Data reflects FY period over period changes; Capex increase aligned with R&D expansion initiatives.

Operational Shifts: What Changed in Alamo Group’s Recent Performance?

The Q4 earnings report released March 2, 2026 revealed an earnings and revenue miss relative to analyst estimates [N1][N6]. Revenues softened amid continuing order fulfillment challenges with unfilled customer orders declining from $668.6 million at end-2024 to $599.7 million at end-2025 [S4]. Such declines may signal either delayed orders caused by supply chain constraints or cancellations as customers reassess capex plans under uncertain macroeconomic conditions.

Supply chain improvement is noted compared to prior years but lingering inflationary raw material costs—particularly steel and hydraulics—continue to pressure margins [S27]. Labor availability issues also persist regionally affecting production flow.

Seasonality is less marked than some peers given Alamo’s diverse end-markets; however replacement part sales spike into mid-year maintenance cycles which helps smooth revenue variability somewhat [S6]. Competitive forces remain significant as Alamo confronts larger multinational companies deploying greater resources for marketing and innovation [S4]. Dealer network strength remains vital for distribution but also creates complexity in managing customer service quality during volatile periods.

Growth Drivers: Acquisitions, Innovation, and Geographic Expansion

Acquisition-led expansion has been central to Alamo's historical growth strategy [S12][S17]. The completion of the Petersen Industries buyout early in FY2026 expands penetration into adjacent niche equipment sectors complementing existing brands [N5]. Previous acquisitions include Timberwolf Limited (UK), Morbark LLC (Michigan), Royal Truck & Equipment (Pennsylvania), Ring-O-Matic (vacuum excavation), Dixie Chopper (zero-turn mowers), among others—each adding geographic breadth or product diversification.

Research & Development spend sustained at $11.2 million (around ~0.7% of sales in FY25) supports refinements such as Nite-Hawk’s hydraulic sweepers featuring innovative auxiliary engine elimination systems improving fuel efficiency [S6]. Engineering teams numbering over two hundred focus on enhancing flail mower designs, integrating remote control capabilities for boom mowers (McConnel®), and expanding snow removal equipment efficacy.

Manufacturing spans North America (US & Canada), Europe (UK & France), Brazil, and Australia offering risk-mitigated exposure across cyclical markets with established dealer networks allowing localized customer support [S1][S14].

Challenges Ahead: Competitive Pressures and Supply Chain Constraints

Intensifying global competition against industry giants like Deere & Company or CNH Industrial generates ongoing pricing pressure exacerbated by input cost inflation—with particular sensitivity around steel prices impacting heavy-duty equipment margins [N3][N4][S13]. Supply chains improved but are not immune to shocks; supplier constraints on drivelines, gearboxes, hydraulic hoses necessitate close vendor management [S27].

Order cancellations remain a tangible risk given customer budgets often linked to government spending cycles affecting infrastructure projects [S13][S26]. Additionally compliance with rising environmental regulations such as EU Tier IV/V emission standards or CARB zero emission mandates adds complexity especially regarding available truck chassis platforms for certain mounted equipment lines [S26]. Dealers represent both a competitive barrier through entrenched relationships yet a point of vulnerability if dealer contracts or stocking levels adjust downward due to economic headwinds [S4][S13].

Earnings Miss Explained: Recent Quarter Insights and Market Reactions

The Q4 results shown in early March confirm lower-than-expected revenues and profits driven partly by reduced unfilled orders and softer demand dynamics across some segments [N1][N6]. Notably peers Deere (DE) and CNH Industrial (CNH) reported solid beats on earnings attributed mostly to strong agricultural equipment demand spurred by commodity price recovery—factors less pronounced for Alamo given its broader industrial exposure [N3][N4].

Competition from larger players with scale advantages hints at medium-term sentiment challenges for ALG shares despite its established niche positions [N1]. Margin contraction plus slower order book inflow emphasize the need for operational tightening.

Capital Allocation Discipline: Dividends, Share Repurchases, and Cash Flow Generation

Alamo Group exhibits prudent capital use balancing shareholder returns with reinvestment needs [F1][S28]. Dividends have gradually increased annually—from just above $8 million paid out in FY22 to $14.4 million in FY25—signaling consistent cash return policy aligned with stable free cash flow generation.

Buybacks remain modest relative to market cap (~$3 million in FY25) illustrating conservative share repurchase activity rather than aggressive leverage-driven capital returns.

Operating cash flow at $177 million comfortably covered capex of $30 million yielding approximately $147 million free cash flow in FY25 [F1]. The company holds a strong current ratio of about 4.57 indicating robust liquidity buffer amidst uncertain demand pulses.

Return on equity stood around a moderate ~9% in FY25 calculated as net income over average equity ($1.15 billion year-end equity) illustrating efficient though not exceptional capital profitability within niche construction equipment markets.

Investment Highlights and What to Monitor Moving Forward

Alamo Group’s entrenched position leveraging diversified vegetation management and industrial equipment categories alongside an extensive geographic footprint constitutes its core strength [N7][N8]. A rich portfolio of trademarks including Rhino®, Gradall®, Morbark®, Schwarze®, Tiger®, Ring-O-Matic®, among others provide high customer recognition within specialized verticals.

On the downside potential order book erosion stemming from competitive intensity combined with supply chain jitters represent principal near-term cautionary factors.

Key developments to observe include successful integration outcomes from recent acquisitions such as Petersen Industries; continued R&D outputs impacting product competitiveness; evolving regulatory impacts especially around emissions standards; shifts in dealer inventory strategies reflecting macroeconomic sentiment; raw material cost trajectories; plus general infrastructure spending affecting governmental procurement cycles.

Taken together these variables will influence whether ALGO can restore top-line momentum while stabilizing margin pressures seen most acutely through late FY25.

This analysis reflects publicly available information up to March 2026 without recommendation or investment advice concerning Alamo Group Inc.'s securities or operations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments