Broadcom’s Strategic Leverage of AI-Ready Technologies Amid Robust Financials and Rising Debt

Broadcom navigates semiconductor leadership by balancing strong liquidity and rising debt while advancing its AI-driven innovation.

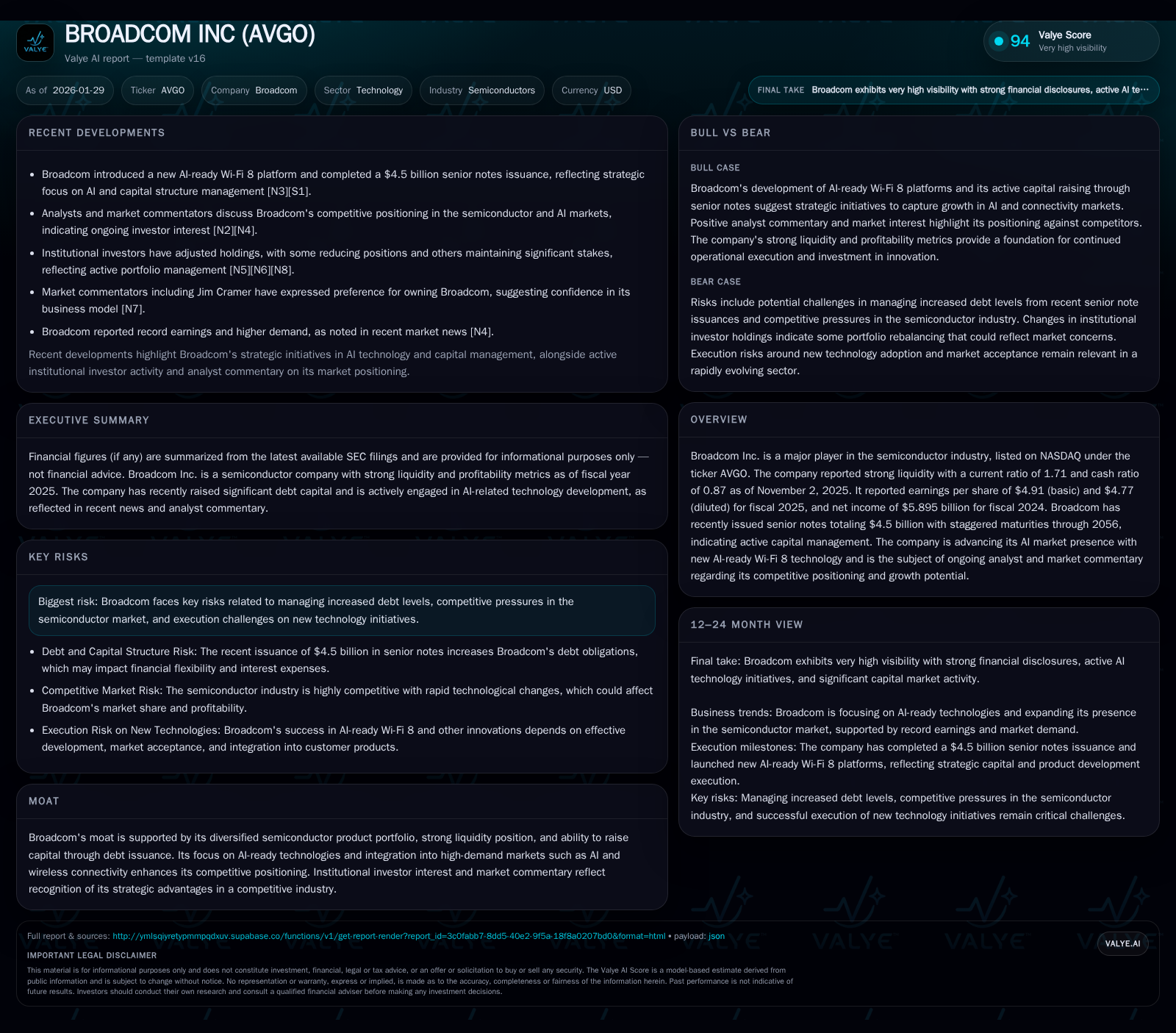

Broadcom Inc. reported record earnings and robust liquidity with a current ratio of 1.71 as of fiscal year 2025, underpinning its capacity to finance ambitious growth initiatives. The company actively manages its capital structure through $4.5 billion in senior note issuances, reflecting a deliberate strategy to fuel investments in AI-ready technologies, including Wi-Fi 8 and custom ASICs. Amid intense semiconductor market competition and AI-driven disruption fears, Broadcom’s diversified portfolio and AI market positioning secure a resilient competitive moat, albeit tempered by execution risks and elevated leverage.

Broadcom’s Financial Foundation: Liquidity, Earnings, and Capital Moves

Broadcom Inc. arrived at the close of fiscal year 2025 on solid financial footing, underpinned by a robust liquidity position and record earnings performance. As of November 2, 2025, the company reported cash and cash equivalents of approximately $16.2 billion alongside current assets totaling nearly $31.6 billion against current liabilities around $18.5 billion — yielding a current ratio near 1.71 [F1]. This metric reflects Broadcom’s ability to cover short-term obligations comfortably without compromising capital allocation for strategic growth.

Net income for fiscal year 2024 stood at $5.895 billion [F1], illustrating consistent profitability even amid turbulent semiconductor industry cycles. Earnings per share (EPS) also reached new highs for fiscal year 2025 with basic EPS at $4.91 and diluted EPS at $4.77 [valye_report_excerpt]. These figures embody not just underlying operational efficiency but also effective cost controls and pricing power within select high-demand product segments.

This strong financial foundation equips Broadcom with significant optionality to fund R&D initiatives targeting emergent technologies and markets — notably artificial intelligence (AI) infrastructure — without immediate reliance on dilutive equity issuance or asset sales.

Debt Strategy: Balancing Growth Ambitions and Risk

While Broadcom’s liquidity metrics keep it well-positioned operationally, its capital structure reveals an active deployment of leverage aimed at expansion. The company has issued senior notes aggregating $4.5 billion with tenor profiles extending through 2056 [valye_report_excerpt]. This long-duration debt issuance strategy underscores a confident approach to securing low-cost capital in today’s credit markets while deferring principal repayment far into the future.

Such staggering allows flexibility in managing cash flows over multiple economic cycles; however, elevating leverage introduces heightened risk if macroeconomic or industry downturns compress margins or slowdown innovation adoption.

Critically, this move enables Broadcom to accelerate investments into next-generation offerings like AI-ready Wi-Fi 8 platforms and custom ASIC chips — segments requiring substantial upfront capex and engineering resources before scaling revenue streams materialize [S1]. Yet stakeholders must remain vigilant regarding interest coverage ratios and covenant compliance as debt levels begin to rise against operating income trajectories.

Could peak leverage undermine balance sheet resilience if innovation programs encounter execution delays?

Innovation Spotlight: The Push into AI-Ready Wi-Fi 8 and Custom AI Chips

Broadcom’s R&D thrust has zeroed in on embedding AI capabilities across its connectivity portfolio. A standout milestone includes launching an AI-ready Wi-Fi 8 platform designed explicitly with machine learning optimizations that target reduced latency, enhanced throughput, and adaptive network management [N14].

Complementing this wireless leap is Broadcom’s escalating shipment volumes of application-specific integrated circuits (ASICs) tailored for AI workloads — with projections hinting at a tripling pace over recent periods [N13]. These ASICs serve as critical accelerators within data center compute fabrics where bespoke silicon architecture trumps generic CPU/GPU designs in performance-per-watt efficiency.

By expanding these technology vectors simultaneously — wireless connectivity fused with advanced compute silicon — Broadcom cultivates a product moat that intersects vital sectors such as cloud infrastructure, edge computing, and mobile devices.

Such breadth widens barriers for competitors dependent solely on one technology axis while positioning Broadcom as a system-level collaborator rather than merely a component supplier.

AI Market Positioning: Capturing the Custom Chip Opportunity

Amid the semiconductor industry's transformative shift towards AI-first architectures, Broadcom aims to dominate the custom chip niche projected to represent a lion’s share of total AI silicon spending by the latter half of this decade.

Industry analyses forecast Broadcom securing approximately 60% market share in custom AI processor shipments by 2027 [N12], an aggressive target supported by its growing ecosystem partnerships and specialized design services tailored to hyperscale cloud providers’ unique workloads [N11]. This dominance contrasts markedly against legacy players whose broader portfolios dilute focus on customized solutions optimized for machine learning frameworks.

Broadcom’s strategy leverages architectural customization combined with manufacturing scale advantages in packaging technologies, enabling faster time-to-market cycles — an increasingly critical factor given rapid iteration demands within AI research communities.

Can such concentrated investment translate into reproducible growth vectors capable of offsetting cyclical headwinds endemic to semiconductors?

Competitive Landscape: Surviving Amid Semiconductor Rivalry and AI Disruption Fears

The semiconductor sector encountered notable volatility recently as broad market indices experienced declines linked to fears around AI disruption and overvaluation corrections among chipmakers [N6][N8]. Longstanding rivals such as AMD have suffered share price setbacks despite solid earnings beats due to cautious forward guidance [N2].

In this turbulence, Broadcom’s diversified business model offers resilience; it is less exposed to any single end-market downturn due to balanced revenue sources spanning wired infrastructure components, wireless solutions, storage adapters, and burgeoning AI chips [valye_report_excerpt]. Analysts note that while no semiconductor company is immune from market swings, Broadcom appears comparatively insulated given its scale and stable contract-based customer relationships.

Nevertheless, competition from entrenched giants pursuing analogous AI silicon strategies remains fierce — necessitating constant innovation pace acceleration.

Insights from Market Commentary and Analyst Expectations

Recent analyst discourse reflects a cautiously constructive tone toward Broadcom’s near-term outlook. Expectations lean toward another earnings beat propelled by continued demand for AI infrastructure components amidst upgraded network deployments [N3][N4]. Equity flows into ETFs focusing on technology stocks embracing artificial intelligence themes increasingly favor stocks like Broadcom that combine hardware muscle with software-enablement capabilities [N9].

The Zacks Analyst Blog highlighted Broadcom alongside other industry leaders as beneficiaries of growing data center investments centered on accelerating machine learning workloads [N7]. However, these endorsements come tempered with recognition that headline earnings beats may not shield shares from overall tech sector sentiment shifts tied to macroeconomic query risks.

Evaluating Risks: Execution Challenges and Capital Structure Concerns

Despite promising fundamentals, certain risk vectors loom large over Broadcom's trajectory. The expanding debt load exemplified by recent senior note issuances necessitates precise cash flow management; any slippage could impair credit metrics or constrain funding windows for future strategic acquisitions or R&D increases [valye_report_excerpt][S1].

Simultaneously, the complexity inherent in deploying cutting-edge AI-related hardware risks schedule slippages or production yield challenges impacting predefined shipment ramp targets for ASICs and Wi-Fi technologies.

Competitive pressures intensify as global semiconductor supply chains face geopolitical uncertainties along with aggressive moves from companies pursuing alternative architectures or software-driven acceleration approaches.

Is Broadcom's blend of engineering agility and financial discipline sufficient to mitigate these converging headwinds?

The Investment Thesis: Long-Term Moat Rooted in Diversification and AI Integration

Looking beyond near-term noise reveals a compelling business narrative anchored by Broadcom's strategic strengths across finance, technology innovation, and market positioning. Its diverse product footprint shields revenue streams from volatile single segments while proprietary advances in AI-ready silicon embed it deeper into emerging ecosystems where demand is expected only to accelerate [valye_report_excerpt].

Institutional investor interest signals market recognition that Broadcom holds durable competitive advantages founded on scale economics combined with nimble innovation cycles responsive to rapid shifts in compute paradigms.

While execution risks are non-trivial—especially under rising leverage—the company's current liquidity buffer coupled with proactive capital management provides runway for sustained bets on transformational technologies vital to modern digital infrastructures.

Ultimately, Broadcom exemplifies how semiconductor leaders can navigate complexity by fusing financial stewardship with forward-looking product development focused squarely on next-generation AI applications—solidifying their foothold amid one of technology's most consequential evolutions underway today.

This document reflects analysis derived from publicly available information including SEC filings ([S1],[S2]), recent news reports ([N1]-[N14]), company facts ([F1]), and Valye News proprietary excerpts. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments