BRC Inc. Faces Profitability Challenges Despite Wholesale Growth and Operational Restructuring

Veteran-founded coffee brand expands retail presence while grappling with persistent losses and channel shifts.

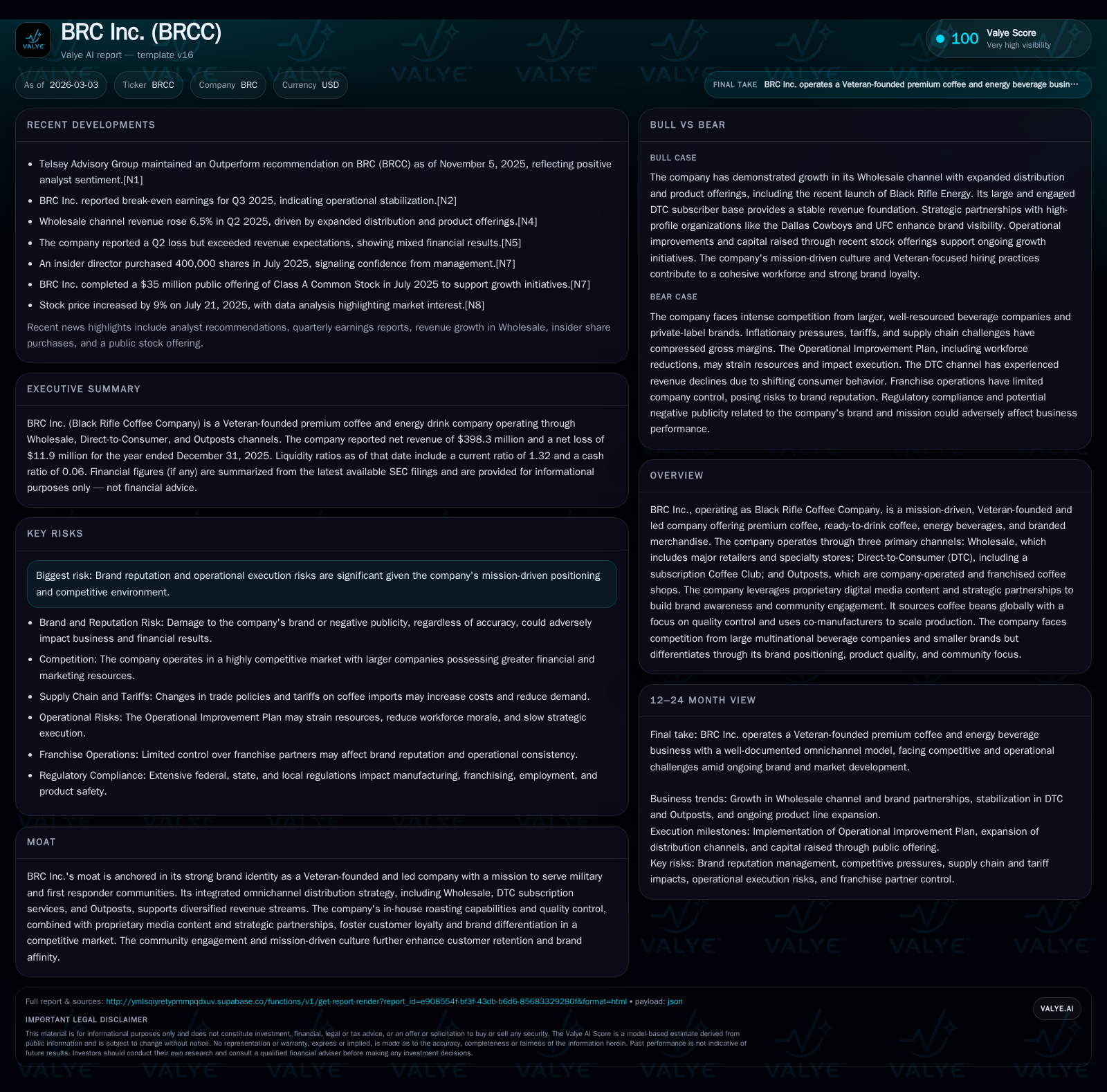

BRC Inc., operating as Black Rifle Coffee Company, has built a distinctive brand tied to Veteran and first responder communities, growing its wholesale channel significantly to become the largest revenue contributor. However, financial results show continued operating losses, driven by elevated marketing spend and operational costs despite an efficiency plan begun in 2025. The direct-to-consumer subscription business is declining, reflecting both strategic shifts and higher acquisition costs. The company’s liquidity remains adequate but constrained by debt covenants. Future growth hinges on scaling wholesale distribution and introducing new products within a competitive specialty coffee and energy drink market.

Company Overview

Founded in 2014 by U.S. Army Veteran Evan Hafer, BRC Inc., known as Black Rifle Coffee Company (BRCC), has developed into a premium coffee and energy beverage brand with a deeply embedded mission focus supporting active military members, Veterans, first responders, and affiliated communities [S1][S9]. The company's identity as a Veteran-founded entity is central to its marketing narrative and brand positioning, fostering loyalty through community engagement and proprietary digital media content.

BRCC operates primarily through three channels: Wholesale distribution via major Food, Drug & Mass (FDM) retailers and specialty stores; Direct-to-Consumer (DTC), including an e-commerce subscription service dubbed the Coffee Club; and Outposts—company-operated or franchised brick-and-mortar coffee shops [S1][S9]. Its product portfolio spans roasted coffee beans (in-house roasting for most bagged products), ready-to-drink (RTD) coffee beverages, an energy drink line launched late 2024 (Black Rifle Energy), plus branded apparel and outdoor lifestyle gear designed to deepen brand engagement.

Past Growth and Historical Performance

Revenue Mix Trends

BRCC's strongest growth segment is Wholesale, which climbed from approximately $245 million in 2024 to about $258 million in 2025 — increasing its contribution to roughly 65% of total revenue [S10][S18]. This channel includes major national players like Walmart, Sam's Club, regional grocery chains, convenience stores such as 7-Eleven and Circle K, as well as specialty retailers like Bass Pro Shops.

Conversely, the DTC channel contracted during this period due to heightened customer acquisition costs alongside the company's strategic shift away from heavy direct advertising towards expanding presence on third-party e-commerce platforms [S1][S18]. Outpost operations stabilized but showed limited revenue growth prospects with management focusing on operational improvements and potential closures of low-performing units to enhance profitability [S1].

Financial Metrics Summary

The company has struggled with profitability since going public. Operating income was negative $24.6 million for fiscal year (FY) 2025 but reflected improvement compared with much larger operating losses in FY2023 (-$50.2 million) and FY2022 (-$67.8 million). Similarly, net income losses narrowed to -$11.9 million in FY2025 from deeper losses earlier [F1].

Operating cash flow remained negative at approximately -$9.8 million, contrasting with positive operating cash flow generated ($11.3 million) in FY2024 before the intensified restructuring efforts took hold [F1]. Capital expenditures decreased markedly from historic highs exceeding $27 million down to $3.7 million in FY2025—indicative of more restrained investment after aggressive expansion phases [F1].

The operational restructuring effort that commenced mid-2025 aimed at expense reduction involved severance payments and logistics provider changes costing $5.6 million but is projected to save over $8.9 million annually per management estimates [S1][S15]. By year-end 2025 roughly $5.3 million of these savings had materialized.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -12 | -10 | -25 | 4 | -303.6% |

| 2024 | -3 | 11 | 4 | 9 | +82.4% |

| 2023 | -17 | -25 | -50 | 27 | +79.8% |

| 2022 | -83 | -116 | -68 | 30 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | -13 | ||

| 2024 | 0 | 3 | |

| 2023 | 0 | 0 | -52 |

| 2022 | 0 | 20 | -147 |

Source: SEC companyfacts cache [F1].

Table: Key financial metrics illustrating volatility in profitability coupled with recent operational cost containment.

Balance Sheet & Liquidity

At year-end 2025, BRCC held cash reserves of roughly $4.3 million along with working capital of $24.2 million against current liabilities near $76 million for a current ratio of about 1.32 — indicating modest near-term liquidity cushion [F1]. Post a June-July 2025 equity offering generating net proceeds totaling approximately $37 million the company strengthened its balance sheet notably [S4][F1]. It retains borrowing availability under existing credit facilities totaling over $55 million and remains compliant with all financial covenants related to leverage ratios and liquidity thresholds as required by lenders [S6][S19].

Future Growth Prospects

Wholesale Expansion Initiatives

Management highlights ongoing efforts to increase penetration within the Wholesale channel via new retailer partnerships and broader geographic reach across multiple retail segments including club stores, grocery chains, convenience outlets, and specialty shops [S1][S14]. Continued investments are planned for product launches — particularly innovations that build upon Black Rifle Energy beverages introduced recently — strengthening SKU diversity for sustained consumer interest.

DTC Optimization & Marketplace Presence

Despite declining DTC revenues due principally to changing consumer purchase behaviors favoring broader retail availability over subscriptions, BRCC aims to revitalize this channel through personalized shopping experiences supported by tailored digital content strategies while growing third-party e-commerce marketplace exposure [S1][S18]. However, challenges remain around customer acquisition cost control and retention stability.

Outposts Rationalization

The brick-and-mortar Outpost footprint is expected to see limited growth near term while focusing on improving profitability metrics through enhanced customer retention tactics alongside possible closure or repositioning of underperforming locations [S1][S14]. This reflects a strategic reallocation towards higher-return channels.

Product Innovation Pipeline

The company intends continual product line expansions encompassing new roast profiles sourced handsomely from Latin America alongside African and Asian origins; enhanced RTD offerings leveraging co-manufacturers scale; lifestyle branded merchandise growth; plus energy drinks diversification — all elements designed not only for top-line growth but also margin enhancement under tighter cost controls [S13][S20].

Forecasts / Milestones / Expectations

While explicit forward guidance beyond general statements is absent from the filings reviewed, key performance indicators to monitor include:

- Wholesale revenue trajectory given its critical mass role (~65% of revenues).

- Trends in DTC subscriber counts and average order values amidst pricing or model changes.

- Progress against estimated Operational Plan savings exceeding $8 million annually.

- Execution outcomes regarding Outpost portfolio optimization.

- New product launches cadence and initial market reception especially energy beverages.

- Impact of global trade tariffs on coffee bean cost structures affecting gross margins.

- Legal developments surrounding ongoing contract disputes noted which could affect contingencies expenses [S16][S22].

These factors collectively will signal the company’s ability to transition toward sustained profitability.

Returns & Capital Allocation

BRCC has not paid dividends since before going public circa FY2021 when a one-time dividend paid was recorded [$7m], nor has it engaged in share repurchases during the last three reported years amidst reinvestment priorities amid uneven earnings performance [F1]. Return on equity based on FY2025 results is negative approximately -26%, reflecting ongoing net losses against shareholder equity expansions following capital raises [F1].

Free cash flow remains negative near -$13.47 million after factoring capital expenditures outflows from operating cash flows performance almost entirely impaired by recurring operating losses and working capital demands [F1].

Liquidity levers remain primarily oriented toward managing debt maturities cautiously while growing sales volumes with organic marketing investments rather than returning excess capital at this stage.[S4][S6]

Market Position & Competitive Environment

BRCC operates in highly competitive sectors spanning premium coffee roasting/retail and RTD beverages where dominant global incumbents such as Nestlé (with premium brands like Nespresso), Starbucks (with extensive store networks), PepsiCo/Mountain Dew (energy drinks), Monster Beverage (energy category), alongside private-label brands vie intensely for shelf space, consumer mindshare, innovation leadership, distribution partnerships, pricing advantage, packaging design differentiation, and promotional budgets [S12][S20].

However, BRCC's moat stems principally from authenticity tied to its Veteran-founded mission-driven ethos which resonates strongly within military-connected audiences—a niche seldom deeply penetrated by large multinational competitors providing a degree of community-driven loyalty uncommon elsewhere [S20]. Their integrated omnichannel approach combining media production capabilities enhances brand engagement further distinguishing it amid many digitally native competitors lacking physical retail scale or vice versa.

Nonetheless risks persist from rising competitor entries targeting Veteran communities themselves alongside commodity price pressures related notably to agricultural tariffs impacting raw coffee green bean acquisitions primarily originating from Colombia, Brazil—and increasingly diversified Latin America suppliers—as well as Africa/Asia sources adopted recently seeking risk mitigation-[S13][S18].[N.B.: Recent tariffs implemented since Trump era have clouded supply cost predictability per filings S2]

Operational & Regulatory Risks Summary

BRCC acknowledges inherent vulnerabilities linked to brand reputation given its political polarity at times attracting boycotts or adverse publicity unrelated directly to operations but detrimental financially especially when amplified via social media channels without rapid redress options [S7][S10][S21]. Franchise-partner exposure compounds reputational risk owing limited direct control over their operational compliance thereby magnifying possible negative spillovers across Outpost network reputation contagion effects.[S10]

Additionally ongoing legal disputes primarily relating to contract disagreements with consultants/co-manufacturers may result in financial liabilities (~$2.7m accrued per filings plus litigation defense costs) weighing into near-term outflows until resolution occurs.[S16]

Extensive compliance obligations encompass federal/state workplace laws affecting franchise employment practices potentially forcing increased employer liability jointly under evolving US legislation proposals such as the Protecting the Right To Organize Act expanding joint employer definitions.[S11]

Further complications arise from cybersecurity/data privacy compliance imperatives amid evolving legal regimes contributing added operational complexity potentially increasing costs or causing business disruptions if events occur.[S21]

Summary Evaluation

BRC Inc.’s trajectory demonstrates clear success expanding Wholesale distribution—now primary revenue pillar—leveraging strong branding anchored in Veteran identity coupled with innovative digital content strategies fueling customer engagement beyond mere product quality metrics alone.[F1,S20] Yet profitability remains elusive despite meaningful cost containment recent initiatives underscored by expense-heavy scaling attempts between FY22-FY24 shifting into partial recovery mode through structured operational improvement measures during FY25.[F1,S15]

Key inflection points over coming quarters entail arresting decline within DTC subscription economics or redefining its role effectively amidst shifting consumer behaviors alongside establishing Outposts at sustainable profitability thresholds given limited growth outlooks therein.[N.B.] Capital preservation appears prudent given persistent free cash flow deficits obliging careful liquidity management under debt covenant constraints though bolstered by fresh public equity inflows mid-2025 consolidating balance sheet resilience[S4,F1].

Growth opportunities reside mostly within wholesale channel expansion complemented by new product rollouts across RTD coffee variants and Black Rifle Energy lineup playing off already-established brand credibility achieving differentiation vs entrenched incumbents.[N.B.] Tariff environment shifts will require adaptive supply chain planning ensuring commodity price shocks do not erode essential margin buffers.[F1,S2] Overall vigilance regarding reputational risks amplified across media/social ecosystems combined with tight regulatory scrutiny especially franchise employment law exposures remains imperative—any missteps could produce disproportionate adverse financial impacts beyond operational setbacks alone.

This analysis consolidates publicly available information up through March 2026 including SEC filings filed by BRC Inc., augmented by domain expertise contextualizing industry dynamics specific to specialty coffee distribution models allied with emerging beverage innovations serving targeted community segments without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments