CG Oncology Advances Phase 3 Bladder Cancer Asset Despite Widening Losses and Cash Burn

Clinical-stage focus on intermediate-risk NMIBC with cretostimogene pivots growth toward regulatory submission in 2026.

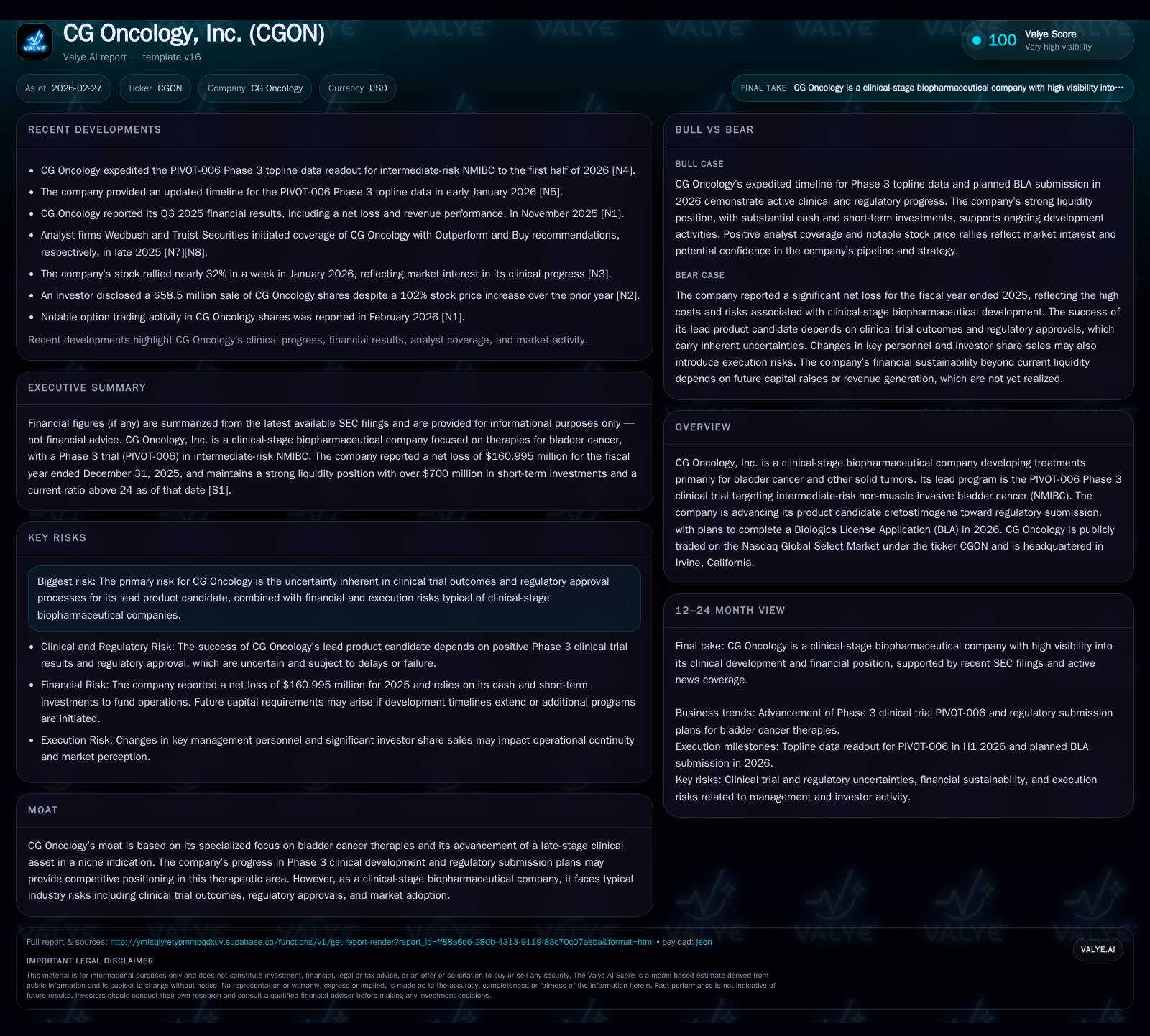

CG Oncology, Inc. is a clinical-stage biopharmaceutical company centered on bladder cancer therapies, primarily advancing its lead program cretostimogene through the pivotal PIVOT-006 Phase 3 trial for intermediate-risk non-muscle invasive bladder cancer (NMIBC). The company expects to complete its Biologics License Application (BLA) in 2026, marking a significant regulatory milestone. Historically, CG Oncology has experienced accelerating losses and negative operating and cash flow metrics reflecting heavy R&D investments. The upcoming topline data from PIVOT-006 and ongoing trial readouts represent key catalysts, though financial sustainability depends on capital raises amid no current revenues or returns.

Company Overview

CG Oncology, Inc., publicly traded under ticker CGON on Nasdaq, is a clinical-stage biopharmaceutical firm headquartered in Irvine, California, focusing on novel therapeutics primarily targeting bladder cancer and other solid tumors [S1][S7]. Its flagship program is cretostimogene grenadenorepvec (CG0070), an investigational gene therapy designed for intermediate-risk non-muscle invasive bladder cancer (NMIBC) — specifically those patients who remain underserved despite standard-of-care treatments. The lead trial advancing this candidate is the PIVOT-006 Phase 3 randomized study evaluating adjuvant intravesical therapy versus surveillance [S16][S17]. The company aims to submit a Biologics License Application (BLA) with the FDA during 2026 based on the topline data from this study [N3][S16].

Historical Performance and Financials

As a clinical-stage entity without commercialized products, CG Oncology reflects typical biopharma developmental-stage financials characterized by substantial R&D investment and corresponding operating losses. Over the past two fiscal years ending December 31, CG Oncology's operating income deteriorated sharply from -$115 million in FY2024 to -$191 million in FY2025—a decline of approximately 66% year-over-year [F1]. Net loss expanded commensurately from -$88 million to nearly -$161 million, representing an ~83% increase in losses [F1]. These escalating deficits underscore intensifying clinical development expenses tied to late-stage pivotal trial activities.

Operating cash flow trends mirror income statement performance. Negative CFO worsened by over two-thirds from -$79 million to -$132 million during the same period [F1]. Capital expenditures remain nominal reflective of minimal fixed asset investment requirements in biotech research phases [F1]. CG Oncology ended FY2025 with roughly $32.5 million in cash and equivalents against current liabilities of about $30.8 million—a current ratio exceeding 24 times—indicating strong near-term liquidity but underscoring dependence on continued financing given burn rates [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -161 | -132 | -191 | 134000 | -82.9% |

| 2024 | -88 | -79 | -115 | 234000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -132 | -21.4 |

| 2024 | -79 | -12.0 |

Source: SEC companyfacts cache [F1].

Approximate return on equity stands negative at about -21%, reflecting sustained losses without commercial revenue streams [F1]. CG Oncology has not declared dividends nor engaged in share buyback programs consistent with its investment phase status [S23][S26].

Clinical Development Milestones and Trial Updates

The PIVOT-006 Phase 3 trial is pivotal for Creotostimogene’s path forward. This study targets intermediate-risk NMIBC patients characterized by heterogeneity including solitary high-grade Ta lesions under three centimeters, representing a sizeable population segment exceeding 50,000 U.S.-based patients [S16]. In January 2026 disclosures, CG Oncology announced accelerated timelines for top-line data expected in H1 2026 [S16][N3], a critical event signaling potential transition to commercialization.

Prior supportive data derive from Phase 2 cohorts such as BOND-003 Cohort P and CORE-008 Cohort A with promising efficacy parameters:

BOND-003 Cohort P: In BCG-unresponsive papillary-only NMIBC patients, high-grade event-free survival (HG-EFS) estimates at three, six, and nine months were reported at approximately 96%, 85%, and 80%, respectively [S16]. Safety was favorable with no Grade ≥3 treatment-related adverse events or treatment discontinuations.

CORE-008 Cohort A: Focused on BCG-naïve high-risk NMIBC patients with carcinoma in situ (CIS), this cohort demonstrated complete response rates upward of nearly 84% overall; notably, an optimized two-step administration technique yielded an enhanced CR rate of approximately 88% versus around 79% for original delivery methods [S16]. No serious safety concerns emerged.

These findings suggest cretostimogene could offer best-in-disease durability and tolerability compared to existing options, though confirmation awaits PIVOT-006 results [S16][S20].

Market Opportunity and Competitive Positioning

Intermediate-risk NMIBC represents an underserved clinical subset where treatment options beyond transurethral resection often lack robust durability or carry significant side effects/re-treatment burdens. Creotostimogene’s design as a non–muscle-invasive intravesical gene therapy differentiates it pharmacologically and administratively. Phase 2 data improvements via newer two-step dosing protocols may further differentiate CG Oncology’s candidate versus traditional intravesical immunotherapies or chemotherapies.

Despite these advantages, competition exists from established chemotherapeutic regimens like Mitomycin C or emerging immune checkpoint inhibitors targeting similar indications. Market adoption post-approval will depend heavily on final Phase 3 readouts validating efficacy/safety claims as well as reimbursement positioning within urological oncology workflows.

Capital Structure and Governance Developments

CG Oncology has actively raised substantial capital through at-the-market offerings under agreements initiated in March 2025, increasing aggregate offering capacity to $550 million during Q1–Q2 of fiscal year ending December 31, 2025 [S14]. This approach aligns with ongoing financing needs driven by costly late-stage trials absent product revenues.

Management changes include appointment of Jim DeTore as interim principal financial officer starting November 2025 after previous interim officer resignation—reflecting efforts to stabilize financial leadership amid scale-up challenges [S24][S25]. The Board also saw replacement of a key compensation committee chair alongside addition of new director Christina Rossi in late November 2025—suggestive of governance recalibration accompanying strategic inflection points [S23][S26].

Risks and Considerations

As explicitly enumerated across multiple SEC filings ([S4],[S5],[S6],[S8],[S9],[S10]), CG Oncology faces standard clinical stage biopharma risks including:

- Uncertainty regarding final Phase 3 clinical trial outcomes that could delay or derail regulatory approvals.

- Potential unforeseen adverse events impacting safety profile upon broader patient exposure.

- Dependence on successful regulatory submission processes culminating in FDA acceptance of the BLA planned for 2026.

- Financial risks stemming from heavy cash burn requiring continued access to capital markets; inability to secure funding would constrain operational runway.

- Competitive threats from alternative therapeutic modalities under active development or recent approval.

Outlook: Catalysts and What to Watch

The focal near-term catalyst remains the topline readout of PIVOT-006 expected mid-year which will inform regulatory timelines including probable BLA filing later in calendar year 2026 [N3][S16]. Positive data could validate cretostimogene’s market viability underpinning subsequent licensing partnerships or commercial preparations.

Parallel updates from ongoing cohorts like CORE-008 will provide complementary support regarding efficacy durability and tolerability dynamics especially with optimized dosing approaches now explored clinically [S16].

Financially, watch for quarterly filings disclosing incremental cash flows highlighting burn rate trajectory alongside any additional equity offerings given absence of revenue generation [F1][S22]. Progress toward establishing commercial infrastructure post approval remains speculative but essential eventually.

In sum, CG Oncology stands at a high-risk/high-reward juncture: advancing promising bladder cancer gene therapy through late stage trials while managing typical early biopharma fiscal pressures without current revenue streams.

This report is intended solely for informational purposes regarding CG Oncology’s business developments and financial position based on publicly available data as of February 27, 2026. It does not constitute investment advice or recommendations to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments