Community Healthcare Trust’s Growth Moderated by Regulatory Complexity and Tenant Concentration Risks

CHCT’s healthcare-focused REIT model delivers steady rental income but grapples with sector-specific regulatory pressures and geographic concentration.

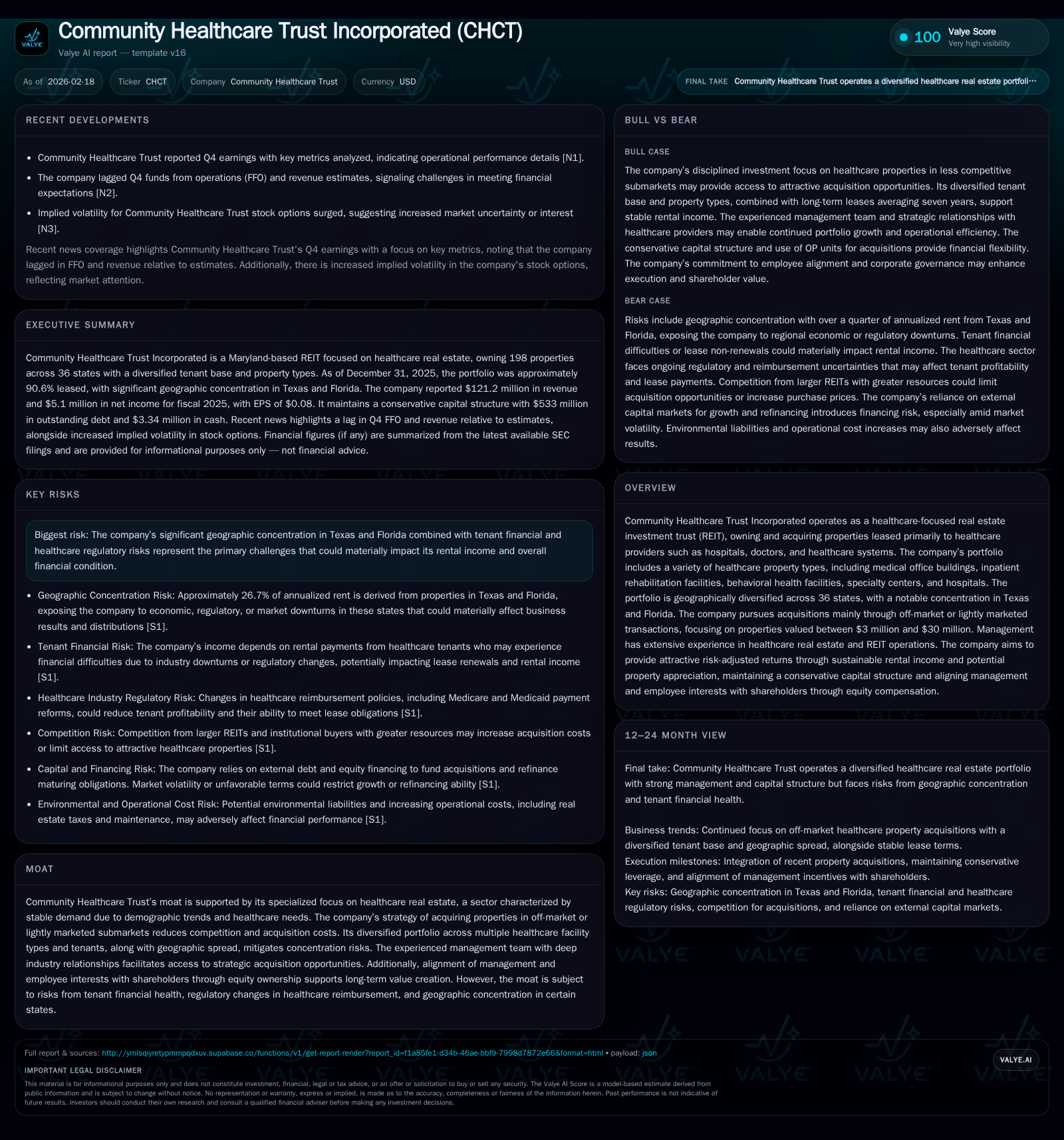

Community Healthcare Trust Inc (CHCT) operates a specialized REIT platform owning healthcare properties across 36 states, emphasizing off-market acquisitions. Revenue grew modestly over recent years, supported by a diversified tenant base and facility types. However, concentrated exposure to Texas and Florida tenants alongside ongoing healthcare regulatory reforms presents risks to stability and growth. CHCT’s capital structure reflects moderate leverage with stable cash flows, yet net income volatility underscores sensitivity to sector dynamics and regulatory shifts.

Company Overview

Community Healthcare Trust Inc (CHCT) is a healthcare real estate investment trust primarily engaged in acquiring, owning, and managing healthcare-related properties leased principally to hospitals, physicians, and healthcare systems. Founded in 2014 and headquartered in Tennessee, CHCT owns 198 properties comprising approximately 4.5 million square feet spread over 36 states as of year-end 2025 [S1]. The portfolio is weighted towards medical office buildings (36% of annualized rent) but also includes inpatient rehabilitation facilities (21%), behavioral health facilities (about 19% combined), specialty centers, surgical centers, hospitals and long-term acute care hospitals [S4].

CHCT pursues an acquisition strategy focused on smaller-scale deals valued between $3 million and $30 million, often through off-market or lightly marketed transactions. This strategy aims to reduce acquisition costs and competition while targeting stable tenants in a sector characterized by demographic secular growth trends related to aging populations and increasing healthcare demand.

Historical Financial Performance

The company has demonstrated consistent revenue growth over the past four fiscal years driven by portfolio expansion and rent escalations within its diversified tenant base. Revenue rose from approximately $97.7 million in fiscal year 2022 to $121.2 million in fiscal year 2025—a compound annual growth rate of roughly 7%, with the latest year showing a 4.7% increase year-over-year [F1]. Operating cash flows have remained strong though slightly declining from $60.3 million in FY2022 to $56.4 million in FY2025.

Net income has shown more volatility: after healthy earnings of $22 million in FY2022 and $7.7 million in FY2023, CHCT reported a net loss of $3.2 million in FY2024 before returning to profitability with net income of $5.1 million in FY2025 [F1]. This fluctuation reflects sector headwinds including tenant credit challenges amid reimbursement pressures as well as elevated costs associated with asset management during expansion phases.

Capital expenditures have trended upward from roughly $4.36 million in FY2022 to about $6.55 million in FY2025 (+42%), signaling reinvestment into maintaining property quality and selective development or improvement projects [F1]. Stockholders' equity has fluctuated somewhat inversely with these results, declining especially during the net loss year but stabilizing near $429 million at end-2025.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 121 | 5 | 56 | 7 | +4.7% | +260.4% |

| 2024 | 116 | -3 | 59 | 5 | +2.6% | -141.2% |

| 2023 | 113 | 8 | 61 | 4 | +15.5% | -65.0% |

| 2022 | 98 | 22 | 60 | 4 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 50 | 1.2 |

| 2024 | 54 | -0.7 |

| 2023 | 57 | 1.5 |

| 2022 | 56 | 4.4 |

Source: SEC companyfacts cache [F1].

Note: Data for operating income, dividends paid, and buybacks are not available from the provided tags.

Industry Positioning and Moat

CHCT operates within the niche of specialized healthcare real estate—a segment known for resilient demand due to demographics as well as less cyclical occupancy patterns compared to general commercial real estate [S1]. Its broad property type mix reduces risk concentration at the asset level while varied tenants including Adventist HealthCare Inc., Hospital Corporation of America, Tenet Healthcare Corporation, Lifepoint Health among others lower counterparty risk [S4]. No single tenant accounts for more than 10% of annualized rent.

The substantial footprint across geographically diverse markets mitigates market-specific downturns except for noted concentrations: Texas (14.3%) and Florida (12.4%) account for over one-quarter of rents representing a meaningful geographic concentration risk under adverse economic or regulatory conditions specific to those states [S1][S26].

Competition is intense for attractive healthcare assets but CHCT’s off-market deal focus limits bidding wars allowing for disciplined pricing discipline.

Regulatory & Sector Risks

Tenant operations rely heavily on government payor programs such as Medicare and Medicaid along with private insurers whose reimbursement models are increasingly subject to cost containment pressures through legislation such as the Affordable Care Act (ACA) modifications and CMS site-neutral payment rules aimed at standardizing rates across provider settings [S10][S15][S20]. These policies can suppress healthcare providers’ profit margins leading to potential financial strain that could impair rent collections.

Expanded legal scrutiny around fraud & abuse laws—including Anti-Kickback Statute, Stark Law, False Claims Act—and heightened audit regimes increase compliance costs for tenants which may indirectly impact their financial stability or ability to renew leases [S9][S19][S20]. Cybersecurity risks affecting tenant protected health information add another layer of operational vulnerability [S27].

Some state Certificate of Need (CON) regulations restrict construction or expansion capabilities for certain types of facilities which can limit tenants’ organic growth opportunities thereby influencing future leasing demand dynamics.

Capital Structure & Returns

At year-end FY2025 CHCT had total debt outstanding of approximately $533 million derived mainly from revolving credit facilities and term loans under its credit agreement capped at a conservative debt-to-total capitalization ratio of about 43%, below the internal policy ceiling of 45% [S24][S29]. Interest rate risk exists especially since approximately $183 million is variable rate debt unhedged at December-end though management employs swaps intermittently [S25].

Return on equity (ROE) is subdued at roughly 1-1.2%, reflecting elevated leverage combined with depressed net income levels relative to equity base [F1]. The company generates robust operating cash flow providing modest free cash flow after capital expenditures — approximately $49.9 million estimated — supporting stable distributions though explicit dividend data is unavailable for recent periods.

No data on share repurchases or buybacks was available from the provided tags.

Growth Outlook & Catalysts

Future growth will hinge on maintaining occupancy levels amid evolving reimbursement landscapes while sourcing new acquisitions accretively within targeted pricing bands ($3-30 million) potentially aided by off-market deal advantages leveraging management’s strong industry relationships.

Key milestones include monitoring lease renewal rates given vulnerable tenant sectors such as behavioral health increasingly impacted by payer reforms along with prospective capex efficiencies enhancing NOI margins over time.

Interest rate trajectories bear watching given impact on cost of capital; successful hedging programs could significantly stabilize interest expense going forward.

Potential headwinds include state-level regulatory shifts impacting construction or permitting affecting tenant expansions plus any deterioration in largest regional markets' economic conditions particularly Texas and Florida which could pressure occupancy or rents materially.

Analysts should observe upcoming quarterly FFO figures closely relative to consensus estimates since recent Q4 earnings showed shortfalls relative to expectations highlighting potential near-term execution challenges or sector headwinds [N2][N4]. Also watch balance sheet developments regarding refinancing activities due within next few years given reliance on capital markets for liquidity beyond internally generated cash.

Conclusion

Community Healthcare Trust offers targeted exposure into the healthcare real estate subsector providing relatively stable rental revenues buffered by portfolio diversity yet remains exposed materially to geographic concentration risk plus macro-level reimbursement reform uncertainties that challenge tenant credit quality. The company’s prudent capital structure coupled with disciplined acquisition approach underpin steady albeit modest growth prospects requiring continual operational vigilance against evolving healthcare policy risks affecting its tenants. Investors tracking CHCT would do well to monitor regulatory developments alongside financial metric trends such as occupancy rates, FFO delivery versus estimates, interest cost variability, and renewal activity within top states.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data as of February 18, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments