CRAWFORD & CO’s Shifting Revenue Mix and Strategic Outlook

Examining CRD-A’s revenue trends, segment dynamics, and capital management amidst claim volume volatility and operational risks.

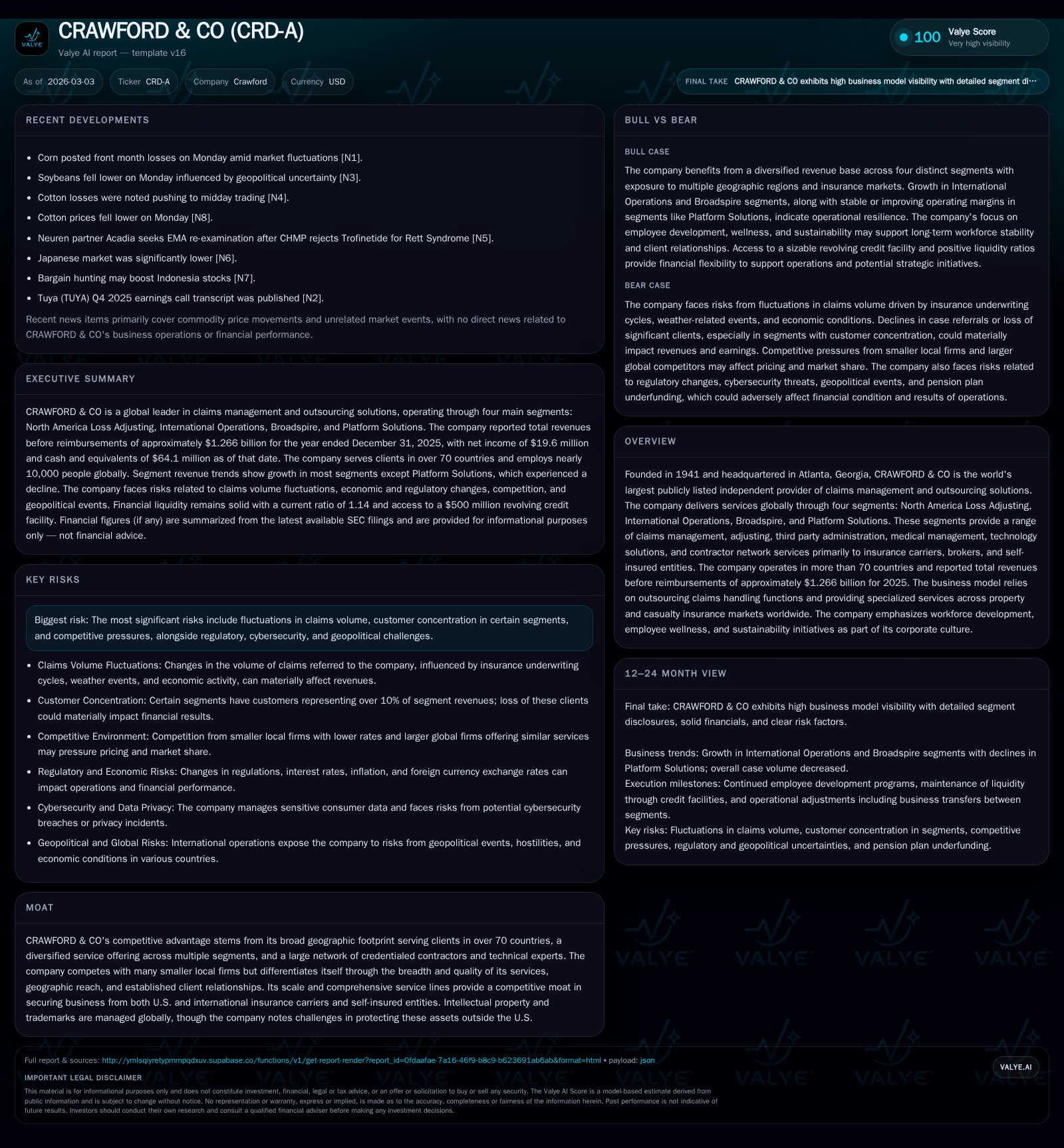

CRAWFORD & CO, the largest publicly traded independent claims management firm globally, reported a 3.5% revenue decline and a 26.2% net income drop in 2025 amid fluctuating claim volumes and shifting segment contributions. The company's diversified global footprint across four key segments underpins its competitive moat, yet reliance on concentrated client contracts in certain units introduces risk. Operating cash flows nearly doubled despite net income headwinds, supporting continued dividends and buybacks while capital allocation remains cautious amid pension funding and debt covenant considerations. Looking forward, contract renewals, regulatory pressures including cybersecurity and pension rules, and claim volume unpredictability represent critical growth levers and challenges.

Historical Revenue Patterns and Profit Drivers

CRAWFORD & CO has demonstrated a relatively stable but recently pressured revenue profile. In fiscal year 2025, total revenues before reimbursements declined by approximately 3.5% reaching about $1.27 billion, reversing moderate prior stability as indicated by historical company facts showing revenues around $1.12 billion in 2018 compared to a peak above $1.24 billion in 2015[F1]. This downward shift is paired with a more pronounced 26.2% decrease in net income to $19.6 million for year-end 2025—a significant compression that points to cost pressures or margin erosion beyond topline softness[F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 20 | 102 | 7 | -26.2% |

| 2024 | 27 | 52 | 6 | -13.1% |

| 2023 | 31 | 104 | 5 | +267.2% |

| 2022 | -18 | 28 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 14 | 11 | 95 |

| 2024 | 14 | 4 | 45 |

| 2023 | 13 | 3 | 99 |

| 2022 | 12 | 27 | 21 |

Source: SEC companyfacts cache [F1].

Operating income figures fluctuate historically but the last definitive value available dates further back at $84 million in 2019[F1]. These divergent trends suggest emerging challenges balancing scale efficiencies with volatile operating fundamentals.

Segment-Level Insights: Contributions and Growth Shifts

CRAWFORD & CO operates through four main segments delivering global claims management services: North America Loss Adjusting (24.1% of revenue in 2025), International Operations spanning UK/Europe/Asia/Latin America, Broadspire focused on U.S.-based third-party administration for workers' compensation and liability claims, and Platform Solutions which includes Contractor Connection networks and catastrophe operations within the U.S.[S1][S6][S18]

Platform Solutions carries notable client concentration risk—two customers individually accounted for more than 10% of segment revenues in the most recent year[S1][S6]. Loss Adjusting segments rely heavily on outsourcing arrangements where carriers delegate claims handling especially for complex or catastrophe-related cases[S18]. Broadspire emphasizes medical case management combining clinical expertise with technology tools[S20], tying its performance closely to corporate clients’ workers’ compensation claim volumes.

Client Concentration and Outsourcing Dynamics

While no single client accounts for more than 10% of consolidated revenues overall, concentrated pockets exist particularly within Platform Solutions where loss of one or two major contracts could materially impact segment results[S1][S6]. Claims handling outsourcing penetration rates vary widely across geographies and insurer strategies; unexpected shifts towards insourcing or consolidation may reduce referral streams[S1][S2][S8]. This dependency creates inherent top-line volatility given limited visibility into clients’ outsourcing plans.

Assessing Revenue Risks from Fluctuating Claim Volumes

Claims volume unpredictability stems from factors including irregular timing of catastrophic weather events (hurricanes, floods), insurance underwriting cycles affecting demand, changes in workplace injury rates tied to employment levels, and competitor actions such as carrier expansion into administrative roles[S1][S8][S9][S10]. These dynamics can abruptly compress revenues tied to case counts or referral rates.

Property & casualty market cycles influence claims referrals frequency while catastrophe event frequency spikes workload episodically[S9]. Client consolidation trends may further diminish total claim volumes available for service providers like CRD-A[S1], underscoring the importance of resource flexibility and service line diversification.

Capital Structure, Cash Flow Strength, and Capital Allocation

Liquidity is supported by a revolving credit facility of $500 million with multiple banking partners—comprising sub-limits for UK, Canadian, Australian borrowers—and secured by a first-priority lien on assets[S4][S5]. As of December 31, 2025, borrowing capacity was approximately $290.7 million after drawdowns[S4], providing financial flexibility though subject to leverage ratio and interest coverage covenants requiring vigilant monitoring given earnings pressure.

Operating cash flow was robust despite net income declines: reaching nearly $102 million in 2025—a near doubling (+97%) compared to the prior year[F1]. Capital expenditures mildly increased by about 13%, consistent with ongoing investments in technology platforms critical for maintaining competitiveness[F1]. Dividend payments totaled approximately $14.3 million with share repurchases around $10.5 million during the year[F1], reflecting a disciplined approach balancing shareholder returns with liquidity preservation.

Pension plan underfunding presents liquidity considerations; notably, the U.S. qualified defined benefit plan had a deficit of $15.4 million at year-end[S4], with expected discretionary contributions of approximately $3 million planned for 2026 that could constrain free cash flow availability.

Operating Cash Flow Evolution vs Earnings Volatility

A notable feature is the divergence between accrual-based earnings performance and operating cash flow generation.FCF approximated $95 million (operating cash flow minus capex) illustrating strong working capital management or sizable non-cash adjustments[F1]. This likely reflects timing differences in receivables collections or deferrals common within insurance services managing large pass-through costs alongside complex contract terms.

This cash conversion efficiency provides resilience even as profitability faces margin pressures from pricing challenges or contract renewals affecting mix.

Outlook: Dependencies, Regulatory Factors, and Market Conditions

Looking forward, CRD-A’s growth depends on successful renewal of major contracts—especially within customer-concentrated Platform Solutions—and managing regulatory evolutions such as defined benefit pension funding requirements potentially increasing cash outflows[S4]. Cybersecurity risk mitigation remains critical given extensive sensitive data holdings involving personal health information across jurisdictions[S8][S10]. Emerging AI regulations influencing claims processing also warrant attention.[S10]

Competitive dynamics continue evolving as insurers consider expanding internal claims handling capacity potentially eroding outsourced volumes[N1][S2]. Macroeconomic factors like geopolitical tensions or downturns could modulate insurance activity levels impacting claim frequency.

Environmental risks linked to climate change may increase catastrophe claim incidence over time but remain challenging to forecast precisely.[S9]

What to Watch: Contract Renewals, Pension Funding, and Debt Covenants

Upcoming milestones include negotiation outcomes for large client contracts contributing significant revenue shares—in particular Platform Solutions where loss of one major client could materially depress segment performance[S1][N1]. Monitoring discretionary pension contributions aimed at reducing underfunding slated around $3 million in 2026 will be important due to their impact on liquidity buffers[S4].

Compliance with credit facility covenants on leverage ratio and interest coverage must remain under close management scrutiny given earnings volatility.[S5]

Operationally, evolving data protection compliance requirements affecting cross-border data flows should be monitored carefully given the company’s international footprint.[S22]

In summary, CRD-A operates at an intersection of scale advantages across diverse global market segments offset by pronounced sensitivities tied chiefly to claim volume variability, client concentration risks, pension funding obligations, and regulatory complexity.Its recent ability to generate robust operating cash flow amidst earnings challenges provides strategic flexibility but underscores the need for vigilant execution around contract retention and cost discipline going forward.

This analysis reflects information compiled as of early March 2026 based on SEC filings (10-K/10-Q/8-K) supplemented by recent earnings disclosures without offering investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments