Salesforce’s Agentforce 360: Accelerating Growth with Embedded AI

Salesforce integrates autonomous AI agents through its Agentforce 360 platform to scale revenue, operational efficiency, and competitive barriers in CRM software.

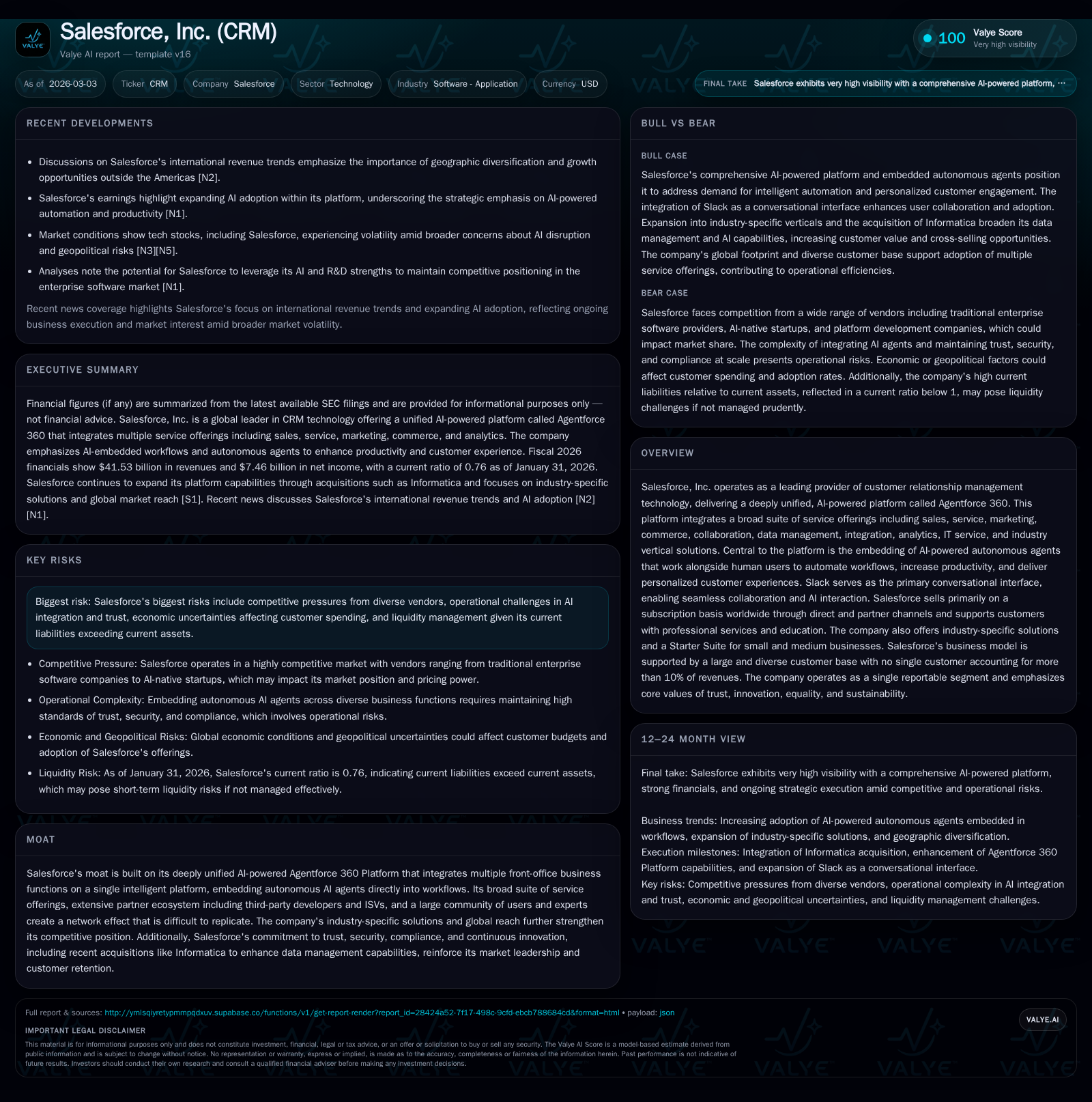

Salesforce has shown robust double-digit revenue growth alongside significant expansion in operating and net income, driven by adoption of subscription services and integration of AI technologies. The Agentforce 360 platform, embedding autonomous AI agents directly into workflows via Slack, differentiates Salesforce in the competitive application software market. International expansion and partner ecosystems offer scalable growth opportunities, while regulatory complexity, competition, and operational risks around AI remain challenges. Capital allocation reflects disciplined buybacks funded by strong free cash flow but liquidity concerns persist due to current liabilities exceeding current assets.

Financial Performance Highlights: Sustained Growth and Operating Leverage

Salesforce's fiscal performance reflects sustained growth driven by its subscription-based CRM services scaled globally. Revenue increased at an approximate CAGR of 26.8% from FY2017 through FY2025 to $22.94 billion as of January 31, 2026 [F1]. Operating income rose sharply by about 66.3% year-over-year to $8.33 billion in FY2025, demonstrating improved operating leverage as fixed costs are absorbed over higher volumes.

Net income similarly expanded by roughly 80.3% YoY to $7.46 billion in FY2025 [F1], while operating cash flow grew approximately 46.5% YoY to nearly $15 billion—signaling robust cash generation supporting ongoing investments and capital returns.

Capital expenditures declined by about 19.3% YoY to $594 million reflecting efficient asset deployment aligned with cloud infrastructure strategies [F1]. Total equity stood near $59 billion at fiscal year-end [F1], though liquidity is pressured by current liabilities exceeding current assets resulting in a current ratio of 0.76 [F1].

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 7.5 | 15.0 | 8.3 | 594 | +80.3% |

| 2024 | 4.1 | 10.2 | 5.0 | 736 | +1888.5% |

| 2023 | 0.2 | 7.1 | 1.0 | 798 | -85.6% |

| 2022 | 1.4 | 6.0 | 0.5 | 717 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 12.6 | 14.4 | 12.6 |

| 2024 | 7.6 | 9.5 | 6.9 |

| 2023 | 4.0 | 6.3 | 0.4 |

| 2022 | 5.3 | 2.5 |

Source: SEC companyfacts cache [F1].

Note: "NA" indicates data not explicitly provided.

Agentforce 360 Platform: Embedding Autonomous AI Agents

A core driver behind Salesforce's differentiation is its Agentforce 360 platform—a unified AI-powered architecture embedding autonomous agents directly into workflows primarily accessed via Slack as a conversational interface [S1][S4]. This allows automation of workflows, contextual decision-making, predictive analytics, and personalized customer interactions seamlessly integrated into daily operations.

This 'agentic enterprise' concept enables digital labor alongside human users to boost productivity while reducing operational costs across sales, marketing, service, commerce, IT management, analytics, and industry-specific applications [S16]. The platform benefits from network effects fueled by millions within Salesforce’s Trailblazer community plus thousands of independent software vendors (ISVs) on the AppExchange marketplace [S4][S13].

However, advanced AI deployment entails execution risks including accuracy challenges, bias mitigation efforts, trust building with users, and adherence to evolving privacy and ethical regulations governing AI use [S9][S17].

Subscription Model & International Expansion

Salesforce generates most revenue from global subscription sales supported by a direct sales force complemented by channel partners such as system integrators and consulting firms [S4][N2]. High renewal rates underpin predictable recurring revenue streams.

While North America remains the largest region (~80%+ total assets), international markets including Europe and Asia are key growth areas despite regulatory complexities related to data localization and compliance regimes differing significantly across jurisdictions [S6][N2]. Expanding marketplace channels and partner ecosystems supports deeper penetration among large enterprises seeking compliant turnkey cloud solutions.

Industry-specific offerings for financial services, healthcare/life sciences, manufacturing enhance cross-selling within accounts while addressing sector-specific regulatory needs [S4][S21].

Risks & Competitive Landscape

Salesforce faces multiple risks that could impact growth or market position:

- Competition: Established incumbents like Microsoft Dynamics and nimble SaaS startups investing heavily in proprietary AI capabilities intensify competitive pressure on pricing and innovation speed [S16].

- AI Trust & Compliance: Potential inaccuracies or biases from AI outputs could erode user trust or invite regulatory scrutiny under laws such as the EU AI Act or state-specific U.S. legislation requiring ongoing investments in governance frameworks [S9][S15].

- Regulatory Burden: Evolving data privacy laws including cross-border transfer restrictions increase compliance costs complicating uniform platform delivery amid geopolitical tensions [S5][S18][S22].

- Sales Cycles & Pricing: Larger enterprise deals involve longer sales cycles with increased pricing pressure affecting near-term bookings visibility [S1].

- Talent & Infrastructure: Scaling support for rapid user growth stresses personnel resources risking service quality if not managed effectively [S1][S20].

Capital Allocation: Buybacks Supported by Strong Cash Flow

Fiscal discipline guides Salesforce’s capital deployment balancing innovation investment with shareholder returns [F1][S8][S12]. In FY2025 ending January 31, the company repurchased approximately $12.6 billion of shares under Board-authorized programs totaling $50 billion authorization overall [F1][S12], executed primarily through open market transactions.

Operating cash flow near $15 billion funds these repurchases alongside capital expenditures of about $594 million resulting in strong free cash flow generation ($14.4 billion) supporting financial flexibility [F1]. Dividends remain stable at $0.416 per share quarterly ($400 million per quarter), reflecting a measured approach favoring reinvestment balanced with systematic capital return [S12].

Return on equity stands near approximately 12.6% based on latest net income relative to shareholders’ equity—a healthy indicator of earnings efficiency though moderated by liquidity considerations given the sub-1 current ratio highlighting short-term obligations exceed liquid assets available [F1].

Outlook: Key Milestones & Forward Considerations

Investors should monitor several developments:

- AI R&D & Adoption: Progress in Agentforce’s autonomous capabilities will test scalability balanced against ethical scrutiny surrounding generative content features recently discussed among analysts [N1]. Incremental product rollouts will reveal value versus complexity trade-offs.

- Informatica Integration: Ongoing integration enhances data governance critical for compliance-heavy industries supporting Data360 platform extensions—a potential competitive edge especially in regulated sectors [N10][S3].

- Geographic Revenue Mix: Continued international diversification exposes variable risks/opportunities linked closely with data localization mandates such as EU DORA framework and geopolitical uncertainties impacting cloud resilience strategies [N2][S6][S18].

- Regulatory Evolution: Adapting proactively to intensifying privacy laws plus emerging U.S./EU AI policies remains vital for maintaining go-to-market agility amid rising compliance costs [S9][S14][S22].

- Competitive Innovation: Tracking competitors’ advanced AI integration velocity offers benchmarks for Salesforce’s innovation pace and pricing power sustainability within enterprise CRM ecosystems serving Fortune-level clients reliant on uptime and vendor trustworthiness [S16].

Salesforce’s combination of deep platform integration through embedded autonomous agents coupled with an expansive ecosystem provides structural advantages; however navigating operational complexities and external headwinds will determine sustained leadership in a hypercompetitive SaaS CRM market.

Disclaimer: Analysis based solely on cited sources including SEC filings ([F1], [S#]) and news ([N#]). Not investment advice.

Comments