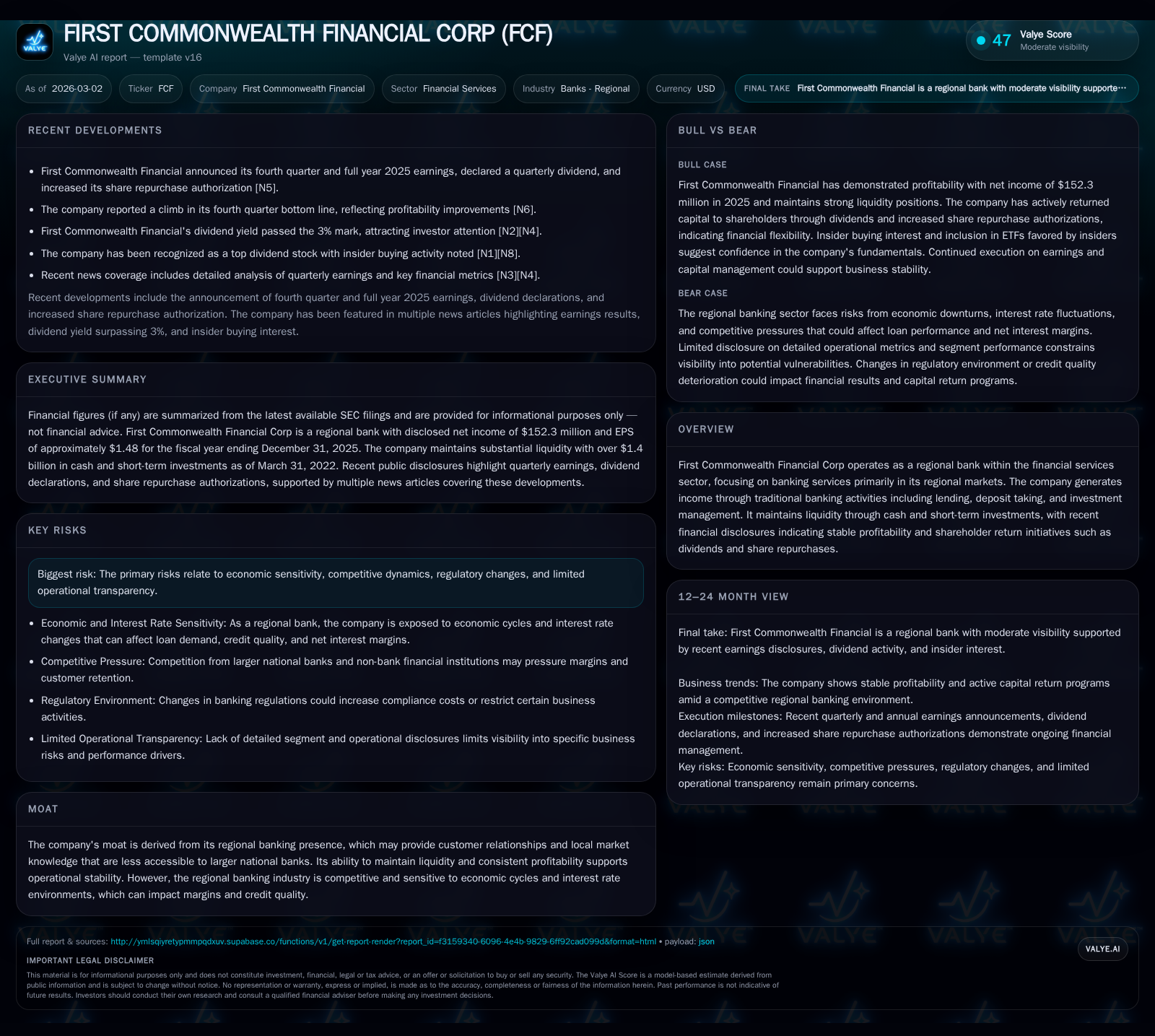

First Commonwealth Financial’s Regional Bank Momentum and Capital Priorities

An analytical review of First Commonwealth Financial's recent growth, capital allocation, and strategic considerations within the regional banking sector.

First Commonwealth Financial Corp has demonstrated steady net income growth over the last four fiscal years, supported by a growing equity base and positive operating cash flow trends. The company’s earnings have been driven primarily by its management of net interest income amid an evolving interest rate landscape and operational efficiencies. Capital allocation strategies encompass consistent dividend payments alongside an increasing pace of share repurchases, reflecting balanced shareholder return priorities within regulatory capital constraints. External factors such as regulatory changes, cybersecurity demands, and competitive pressures present ongoing risks, whereas acquisition discipline and market opportunities form potential growth vectors. Monitoring loan portfolio health, net interest margins, and capital return patterns remains critical to evaluating future operational performance.

Financial Performance Growth: Trajectory and Shifts Over Recent Years

Reviewing First Commonwealth Financial Corp’s financial trajectory over the past four fiscal years reveals stable progress marked by nuanced fluctuations characteristic of regional banking dynamics. Net income climbed from $128.2 million in FY2022 to $152.3 million in FY2025, representing an approximate 6.8% year-over-year gain most recently despite a temporary downturn during FY2023 when net income recorded $157.1 million—slightly below the following year’s figure but above FY2022 baseline levels [F1]. This pattern underscores resilience through varied interest rate cycles and localized economic conditions.

Operating cash flow (CFO) exhibits notable volatility but culminated in a sharp 44.9% year-over-year increase to roughly $187.5 million in FY2025 from $129.5 million a year prior, suggesting improved liquidity management or timing differences in working capital components that favor operational flexibility for the company [F1]. Capital expenditures have averaged modestly relative to CFO; after peaking near $22 million in FY2023, capex retracted slightly before inching up to about $16.1 million in FY2025—a level consistent with maintaining physical infrastructure and technology investments relevant for branch operations and digital enhancements common among community-oriented regional banks [F1].

Equity seen through the company’s balance sheet advanced materially from approximately $1.05 billion at FY2022-end to over $1.55 billion by the close of FY2025, representing strong organic capital accretion complemented possibly by retained earnings accumulation rather than dilutionary share issuance given concurrent share repurchase activity disclosed later below [F1]. This base provides a foundation for leveraging credit growth opportunities while satisfying regulatory capital adequacy requirements.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 152 | 188 | 16 | +6.8% |

| 2024 | 143 | 129 | 16 | -9.2% |

| 2023 | 157 | 151 | 22 | +22.5% |

| 2022 | 128 | 151 | 11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 55 | 36 | 171 |

| 2024 | 53 | 13 | 114 |

| 2023 | 51 | 15 | 129 |

| 2022 | 45 | 16 | 140 |

Source: SEC companyfacts cache [F1].

Table note: All values rounded to nearest hundred thousand; YoY percentage changes reflect latest annual comparisons where appropriate.

Earnings Drivers and Operational Efficiencies Underpinning Profit Trends

Central to First Commonwealth’s profitability is its exposure to net interest income—the spread between yields on loans/securities versus costs of deposits/funding sources—which fluctuates directly with monetary policy shifts and market rates impacting net interest margin (NIM). The company’s MD&A discloses sensitivity to these rate movements alongside emphasis on maintaining asset quality through disciplined underwriting practices amid economic cycles that historically challenge regional banks' credit portfolios [S1]. Meanwhile, recent earnings releases reported better-than-expected bottom line results attributed in part to expense management initiatives enhancing operational efficiency ratios as well as deposit base stability leading to favorable funding costs [N2], [N7].

Loan portfolio composition remains diversified across commercial, consumer, and small business segments typical of regional institutions catering to local market needs, which supports granular risk assessments but also ties performance closely to regional economic developments.

Industry-specific pressure points such as NIM compression due to competitive deposit pricing or economic recession risks are mitigated through proactive balance sheet management; however, continued vigilance remains critical given the historically cyclical nature of community banking net interest income dynamics.

Capital Structure Evolution: Equity, Dividends, and Share Repurchases

From a shareholder value perspective, First Commonwealth has pursued measured capital distribution alongside strengthening retained earnings reserves embedded within growing equity balances [$1.55B at FY2025-end] [F1]. Annual dividends paid rose incrementally from approximately $44.6 million in FY2022 up to $55.5 million by FY2025 indicating both confidence in earning power and a commitment to returning yield to investors—even as share repurchases accelerated sharply—almost tripling—from $12.6 million in FY2024 to around $35.8 million in FY2025 per recent disclosures expanding repurchase authorizations [N3], evidencing aggressive deployment of excess capital when balance sheet leverage permits.

Calculated return on equity stands near an estimated 9.8% for the latest fiscal year aligning with mid-tier regional bank peers balancing risk-adjusted returns with compliance-driven capital buffers mandated post-2008 financial reforms [F1]. Such ROE reflects competent profitability without excessive risk leveraging.

These allocation choices suggest a strategic calibration: sustaining dividend consistency for income-focused shareholders while opportunistically utilizing buybacks as flexible tools for earnings per share accretion amidst stock price volatility or surplus capital windows.

Macro and Regulatory Environment Influences on Future Growth Potential

External forces shape both risk profiles and opportunity sets for First Commonwealth going forward. Potential government shutdowns threaten operational fluidity via disrupted regulatory agencies responsible for loan approvals or servicing federally-backed programs—posing transient credit demand contractions or delayed revenue recognition episodes [S1]. In parallel, evolving federal/state legislation targeting enhanced regulatory compliance frameworks may mandate increased capital reserves or operational cost burdens dampening profit margins.

Moreover, escalating demands for robust cybersecurity protections driven by heightened threats compel continuous investment guided by frameworks such as NIST’s Cybersecurity Framework that First Commonwealth actively integrates into its governance structures—including quarterly reporting protocols from the Chief Information Security Officer through Risk Committees—all serving as essential risk mitigants amid rising digital attack vectors prevalent across regional banks notwithstanding absence of material breaches recently reported [S1].

Concurrently growing investor attention around ESG factors introduces both reputational drivers and compliance dimensions that might impose new costs yet foster differentiation if managed adeptly.

Risk Factors: Interest Rate Sensitivity, Cybersecurity, and Talent Retention

Interest rate volatility directly affects net interest margins central to First Commonwealth’s earnings consistency; rapid increases can widen margins temporarily but may eventually pressure credit quality if borrower stress escalates—a structural tension accentuated by regional banks’ concentrated loan exposures compared with larger diversified institutions [S1].

Cybersecurity frameworks are robust yet remain an area requiring vigilant updates given sophisticated cyber threats; First Commonwealth’s layered defense strategy paired with frequent internal/external audits plus insurance coverage lowers event probability though residual operational risk persists notably against zero-day exploit categories or insider threats [S1].

Human capital management emerges as a notable risk vector—talent competition intensifies particularly as regulatory policies influence incentive design potentially constraining recruitment/retention efforts crucial for sustaining customer relationships entrenched heavily on personal interaction typical within community bank contexts [S1].

Strategic Growth Opportunities Against Competitive and Regulatory Constraints

Acquisitions form a core strategic pillar albeit pursued cautiously with preference for targets sharing cultural alignment alongside managerial strength fostering scalable profitability improvements via economies of scale or service expansion rather than purely geographic footprint accretion alone—a prudent sector-native M&A approach mitigating integration disruption risks known among regional banks delaying synergy realization or diluting existing book values adversely impacting near-term EPS metrics [S1].

Due diligence includes comprehensive vetting of asset quality provisions amid uncertain macroeconomic backdrops while factoring evolving tax/regulatory landscapes that could alter deal economics post-closing.

Competitive positioning faces headwinds from both national banks offering technological scale advantages plus fintech entrants reshaping delivery expectations; however, First Commonwealth’s entrenched local relationship model coupled with expanding digital capabilities can serve as durable moats if investments preserve customer convenience without undermining service quality.

Monitoring Key Indicators and Upcoming Milestones for Validation

Absent explicit forward guidance on revenue or earnings forecasts from recent filings or announcements beyond dividend declarations and elevated repurchase authorizations—metrics investors should closely follow include sequential loan growth rates signaling credit demand vitality; NIM trajectory capturing funding cost management success; payout ratios reflecting sustainability of dividends amid earnings shifts; plus incremental buyback activity pertinent to assessing board confidence levels regarding capital surplus deployment effectiveness [N1], [N2], [N3].

Furthermore, tracking cybersecurity incident disclosures or talent retention-related commentary will provide insights into operational resilience elements underscoring long-term viability.

This analysis assembles facts exclusively from provided SEC reports ([F1], [S#]) and news sources ([N#]) without extrapolating beyond documented data points or issuing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments