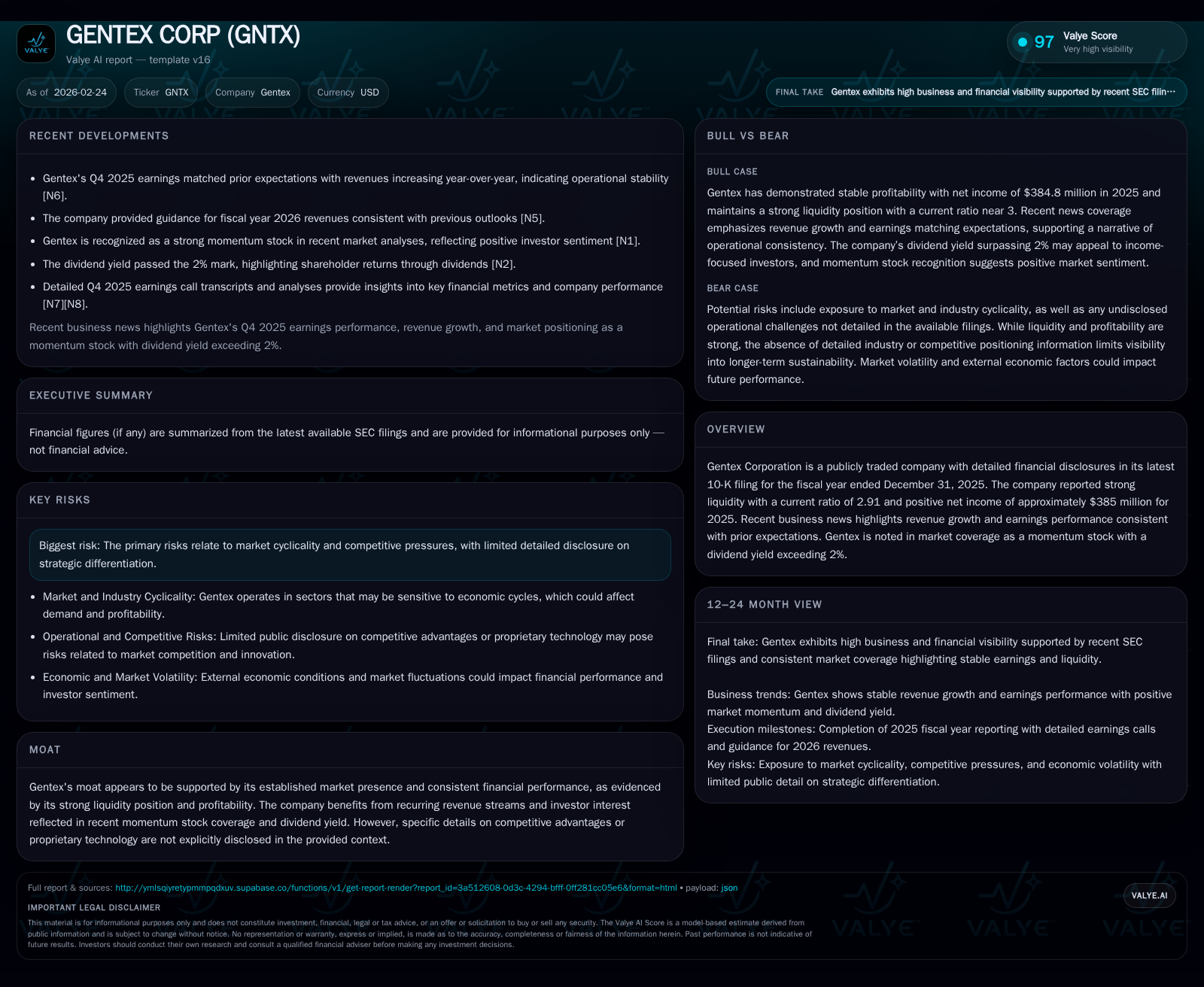

Gentex Corporation Posts Remarkable Income Growth With Sustained Cash Flow Discipline

An exploration of Gentex's dramatic operating income growth in 2025, underpinned by effective capital management and consistent shareholder returns.

Gentex Corporation delivered an exceptional financial performance in fiscal year 2025, with operating income soaring 428% year-over-year and net income more than doubling. The company maintained robust liquidity with a current ratio near 3.0 and generated strong free cash flow, supported by disciplined capex reductions. Capital allocation remained shareholder-friendly, marked by steady dividends exceeding $100 million and aggressive share repurchases surpassing $315 million. While risks related to market cyclicality and competitive dynamics persist, Gentex’s financial resilience and momentum stock status underscore its operational strength heading into 2026.

Historic Income Surge: Quantifying the Operating and Net Income Growth

Fiscal year 2025 marked a pivotal inflection point for Gentex Corporation’s profitability profile. Operating income catapulted to $474 million, up an extraordinary 428% compared to the prior fiscal year’s approximately $90 million [F1]. This outsized jump suggests not only operational efficiencies but possibly volume gains or favorable pricing dynamics within Gentex’s core product segments. Concurrently, net income ascended sharply by 229% to roughly $385 million, well above the previous year's $116 million figure [F1].

Such a significant increase in operating profitability within a single year is unusual for industrial suppliers tied to automotive technology but could reflect favorable cost controls alongside improving demand fundamentals. Despite this surge, no indications point explicitly toward one-time gains; thus, underlying margin expansion or improved operational leverage likely played central roles.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 385 | 587 | 474 | 129 | |

| 2024 | 498 | 90 | 145 | ||

| 2023 | 117 | 537 | 133 | 184 | +35.7% |

| 2022 | 86 | 338 | 94 | 146 | -76.1% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 107 | 315 | 458 |

| 2024 | 110 | 206 | 354 |

| 2023 | 112 | 147 | 354 |

| 2022 | 113 | 113 | 192 |

Source: SEC companyfacts cache [F1].

Liquidity Profile and Capital Structure: Robust Financial Foundations

Gentex closed FY2025 with a notably healthy liquidity position. Current assets stood at approximately $1.13 billion against current liabilities near $388 million, yielding a sturdy current ratio of 2.91 [F1]. This level of working capital covers short-term commitments comfortably and demonstrates effective working capital management crucial for automotive tech firms balancing supply chain fluctuations.

At year-end, cash and cash equivalents totaled around $146 million, offering ample dry powder for strategic initiatives or cushioning against cyclical headwinds [F1]. Although detailed debt figures are not emphasized here, past filings confirm manageable leverage supporting resilient balance sheet flexibility [S10][S19]. This conservative capital structure forms a solid foundation facilitating both operational investment and shareholder returns.

Operational Cash Flow versus Capex: Driving Free Cash Flow Efficiency

On the cash flow front, Gentex exhibited clear discipline and efficiency. Operating cash flow increased by approximately 17.8%, rising to over $587 million in FY2025 from about $498 million the prior year [F1]. Despite this growing inflow from operations, capital expenditures underwent a deliberate contraction of roughly 10.8%, falling from nearly $145 million in FY2024 to close to $129 million in FY2025 [F1].

This combination of growing cash generation alongside restrained capex spending resulted in robust free cash flow approaching $458 million, underpinning the company’s capacity for self-funded growth and sustained shareholder distributions. Such CAPEX discipline aligns well with best practices in industrial manufacturing sectors where capital intensity must be balanced against demand cycles and technology upgrade costs.

Capital Allocation Strategy: Dividends, Share Buybacks, and ROE Trends

Gentex demonstrated consistent commitment to returning value to shareholders in FY2025. Dividend payments hovered above $106 million, largely stable relative to recent years (approximately $110–113 million range previously) [F1]. More notably, share repurchases accelerated significantly—repurchase outlays jumped from roughly $206 million in FY2024 to over $315 million in FY2025 [F1], underscoring management’s confidence in underlying business strength.

Coupled with equity of about $2.49 billion, this level of net income delivers an approximate return on equity (ROE) of around 15.5% for FY2025 [F1]. ROE at this magnitude signals efficient asset deployment that aligns favorably with typical benchmarks among automotive parts suppliers focused on innovation and scale economies [S17].

Revenue Insights: Contextual Clues from Recent Earnings Commentary

While detailed annual revenue data remain undisclosed in recent tags [F1], quarterly commentary provides insight into top-line dynamics. Q4 earnings releases describe sequential revenue growth Y/Y supporting the significant uptick in operating income [N2][N3][N4][N5][S3]. This revenue expansion likely relates to both organic demand improvements across key OEM customers and potentially deeper penetration of newer products within vehicle platforms.

However, without granular revenue breakdowns or absolute figures from XBRL tags or SEC filings provided here, assertions on sales growth should be nuanced. The evidence indicates stable-to-positive top-line trajectories rather than volatility—a positive backdrop enhancing confidence in earnings durability.

Strategic Growth Outlook: Guidance and Market Momentum Indicators

Gentex’s guidance for fiscal 2026 remains aligned with market expectations reflecting sustained momentum [N12]. Coverage as a ‘momentum stock’ emphasizes technical chart strength including moving average breakouts seen recently [N7][N10][N11], which often correlate with investor sentiment shifts toward growth recognition.

These factors combined suggest Gentex aims to maintain its positioning amid evolving automotive technology trends such as smart mirrors and connected car components. Yet sustaining such momentum will require continued innovation alongside managing typical industry cyclicality risks.

Risks Highlighted in SEC Filings: Market Cyclicality and Competitive Challenges

The SEC filings prudently delineate potential headwinds faced by Gentex including cyclical fluctuations inherent to the automotive sector as well as heightened competition pressures [S4][S5][S7]. The company acknowledges that while it has established market presence and recurring revenues contributing to stability, its competitive moat does not strongly hinge on exclusive patents or proprietary barriers.

Investors should remain mindful that cyclicality can impact order timing and pricing power; moreover, technological advancements from rivals could pressure margins absent ongoing product innovation.

Investor Takeaways: Metrics to Monitor in Upcoming Quarters

Looking ahead, critical metrics warrant monitoring include:

- Sustainability of the quadruple-digit percentage gains reported for operating income beyond one-off effects.

- Continuity of strong free cash flow margins driven by disciplined capex against evolving production volumes.

- Capital return patterns encompassing dividends consistency plus share repurchase cadence.

- Revenue growth confirmation via forthcoming quarterly results reporting precise top-line data.

- Macro risk factors tied to global automotive supply chains influencing order backlogs.

- Competitive positioning regarding new technology integration vis-à-vis peer suppliers.

In sum, Gentex's financial reports signal operational resilience and shareholder value orientation amidst standard risks prevalent across automotive-related OEM suppliers pursuing efficiency upgrades.

Disclaimer: This analysis is based solely on publicly available information from SEC filings and news transcripts as of February 24, 2026. It is intended for informational purposes without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments