Hilltop Holdings Surpasses Q1 Expectations with Resurgent Banking and Mortgage Outcomes

The latest quarter reveals strong net interest income growth and reduced credit provisions underpinning Hilltop's financial resilience.

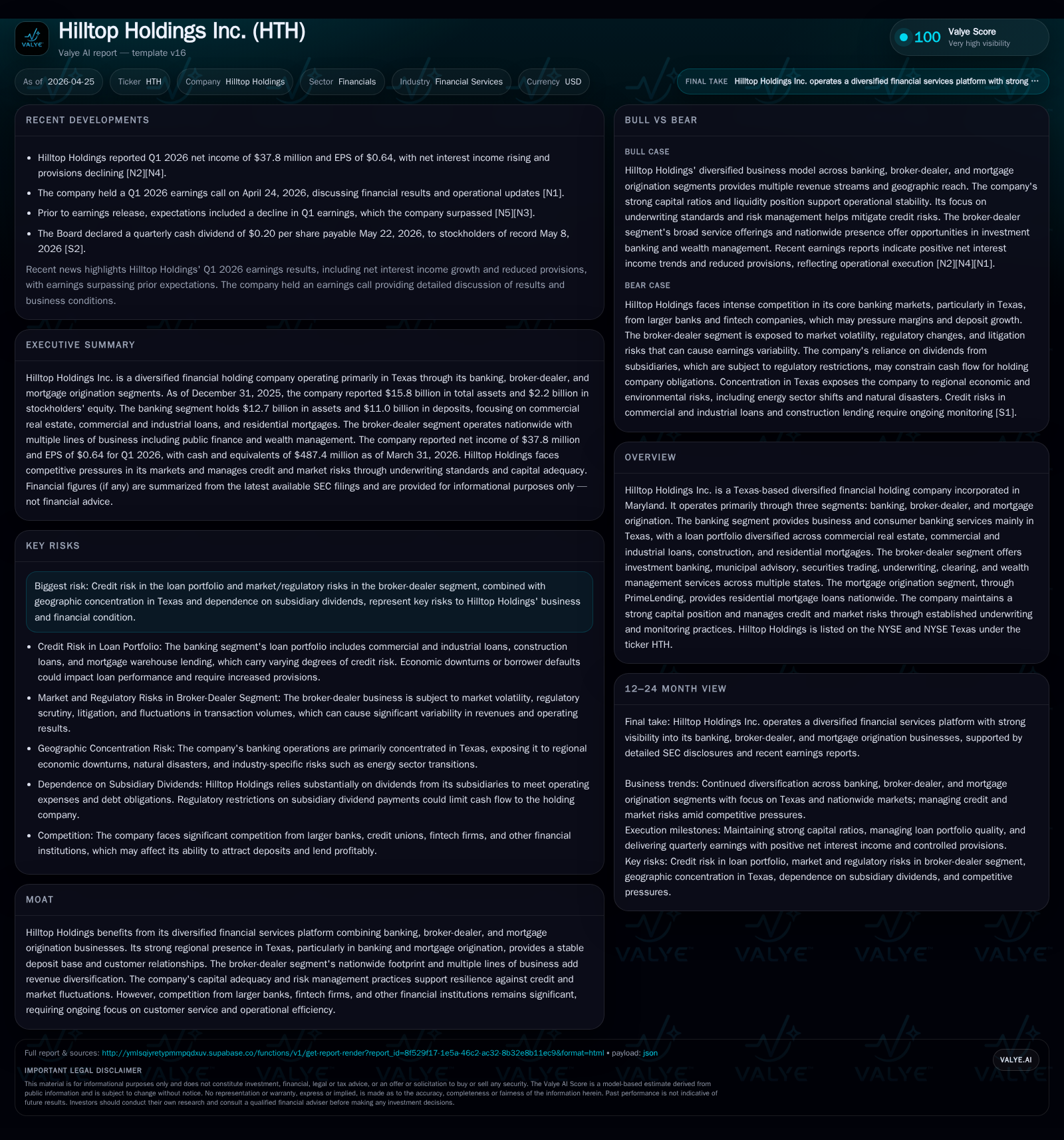

Hilltop Holdings reported a notable operational improvement in Q1 2026 driven by its banking and mortgage origination segments. Net interest income surged, supported by disciplined credit loss management, while the broker-dealer segment maintained steady contributions. Texas remains the strategic core for the company’s diversified model. Industry competition and regulatory factors pose challenges, but established underwriting and strong capital adequacy support durability. Key upcoming metrics to watch include loan book quality, deposit trends, and mortgage volume shifts.

Q1 2026 Operating Update: Outperformance Rooted in Banking and Mortgage Segments

Hilltop Holdings’ first quarter 2026 results released via their April 24th Form 10-Q [S2] and accompanying April 23rd earnings presentation [S3] revealed encouraging signs of operational momentum exceeding market expectations as reported by Nasdaq [N2] [N3] [N4]. The standout factor was an increase in net interest income (NII) driven by improved loan yields within the banking segment alongside disciplined expense control that notably reduced provisions for credit losses compared to prior quarters. This reduction signals improving asset quality or more optimistic economic forecasts reflected within their allowance models.

Mortgage origination volume through PrimeLending held steady with continued reliance on alternative borrower arrangements (ABAs), representing around 14% of funded volume in the prior year [S1]. Broker-dealer revenues remained stable, providing geographic and product diversification. Overall, this quarter marked a positive inflection point emphasizing how core lending and mortgage activities are steering profitability gains amid uncertain macroeconomic conditions [N1].

Business Model Dissection: Diverse Financial Services Anchored in Texas Leadership

Hilltop Holdings operates through three principal segments: banking via PlainsCapital Bank primarily servicing Texans with business and consumer loans; broker-dealer operations encompassing Hilltop Securities delivering investment banking, municipal advisory, underwriting, clearing, and wealth management across multiple states; and mortgage origination through PrimeLending which originates residential loans nationwide [S1] [S7] [S8].

The bank’s loan portfolio is diversified yet regionally concentrated in Texas markets with exposures spanning commercial real estate (CRE), commercial & industrial lending (C&I), construction projects, plus residential mortgages — avoiding subprime risk by adhering mostly to conforming FHA/VA-style standards or jumbo loans meeting investor guidelines [S16]. The approximately $1.3 billion warehouse lines extended to PrimeLending demonstrate vertical integration of mortgage funding backed by bank credit facilities typical of independent mortgage bankers seeking secured liquidity for loan pipeline support [S7].

PrimeLending’s use of retail channels supplemented by ABAs allows access to a broader borrower base outside direct branches or direct employees streamlining origination costs while maintaining overall underwriting discipline [S1]. Broker-dealer activities build on client-facing advisory relationships largely clustered in states like Texas, California, and New York (82% of revenue from top states) but maintain national reach offering fixed income sales & trading as well as public finance—serving municipal entities with bond issuance underwriting critical for state infrastructure funding [S21] [S24]. This tripartite platform generates distinct revenue streams providing Hilltop some insulation amid cyclical swings affecting individual segments.

Industry Context: Competitive Forces Across Banking, Broker-Dealer, and Mortgage Operations

Within the Texas region where its banking arm is entrenched, Hilltop contends with national banks that possess larger scale advantages alongside area community banks competing intensively for deposits and commercial lending opportunities often mediated through pricing sensitivity driven by Federal Reserve policy shifts. Community banks like PlainsCapital leverage local relationships but compete against both fintech entrants targeting deposit accounts or small business loans with digital ease as well as other intermediaries offering syndicated or non-bank alternatives [S21].

In mortgage originations, PrimeLending faces nationwide competition versus large banking conglomerates (e.g., Wells Fargo), nonbank entities adopting artificial intelligence-enabled automated underwriting systems that compress processing times while controlling defaults better than traditional models. Warehouse lines supporting volume funnel capacity remain central since their cost of funds affects profitability margins heavily weighted by prevailing rate environments [S1] [S24].

Broker-dealer competitors vary broadly from regional investment banks reliant on relationship-based deal flows to specialist boutique firms targeting niche municipal advisory mandates. Regulatory compliance under SEC/FINRA frameworks imposes operational costs that smaller or emerging fintech brokers might temporarily evade resulting in market price pressures especially within discount brokerage services not replicating full advisory capabilities [S24].

Capital adequacy demands shaped by Basel III variants translate into constraints on capital deployment potentially limiting growth speed particularly when regulatory guidance restricts dividend remittances upstream from subsidiaries limiting parent holding company flexibility in financial engineering or shareholder returns strategies [S9] [S10].

Growth Catalysts and Limitations: Market Dynamics and Regulatory Considerations

Growth drivers imbedded in Hilltop’s model revolve around sustaining stretched but cautious expansion of the loan book within Texas — particularly CRE sectors benefiting from economic growth peculiar to energy transition zones — provided credit quality stays intact as evidenced by lower provisioning rates this quarter. Net interest margin expansion potential benefits from potential Fed tightening cycles translating into repricing bank loans faster than deposits can reprice downward given sticky customer relationship pricing effects noted commonly within community banks [S6] [S17].

Mortgage originations stand poised for volume scaling contingent on housing market resilience nationwide plus enhanced penetration via ABAs which offer variable cost scalability relative to traditional brick-and-mortar retail channels dominating PrimeLending's footprint. Innovation around digital mortgage processing also plays a role although penetrating tech-savvy borrower segments remains challenging due to incumbent advantages from large-scale lenders leveraging proprietary data ecosystems.

Broker-dealer revenue growth depends on favorable capital market conditions which are notoriously volatile — investment banking underwriting fees tied directly to equity/debt issuance volumes that fluctuate materially quarter-over-quarter; municipal advisory maintains steadier recurring fee pools albeit susceptible to state-level fiscal stresses impacting public finance spending levels.

Constraints include concentrated geographic risk given Texas dominance exposing Hilltop to sector-specific downturns (notably oil & gas industries transitioning under environmental regulations) which could depress borrower creditworthiness or collateral values leading to increased non-performing assets requiring higher reserves risking earnings volatility [S15] [S17]. Also legal risks intrinsic to broker-dealer securities litigation remain significant given historical industry class-actions combined with regulatory scrutiny requiring ongoing compliance investments.

Near-Term Indicators: What to Monitor for Execution and Strategic Progression

Investors should track quarterly updates on key performance indicators such as net interest income trajectory reflecting yield curve movements plus deposit growth trends signaling franchise stability post any competitive rate changes. Monitoring credit provision levels will reveal if recent reductions reflect structural improvement or transient factors benefiting from temporary economic relief.

Mortgage origination volumes funded through ABAs versus direct retail channel shares will indicate channel strategy efficacy and cost efficiency improvements underway at PrimeLending. Brokerage segment metrics like trade volumes, deal pipelines for underwriting fees or new municipal mandates will shed light on balancing steady-state versus episodic revenue streams.

Capital management moves warrant scrutiny including execution pace under the newly authorized $125 million stock repurchase program announced early 2026 validating confidence in excess distributable cash flow available beyond dividend commitments ($0.20 per share declared April 23rd for Q2 payment) [S4] [N1]. Operational efficiency benchmarks such as expense ratios relative to revenues across segments will help assess if scale benefits accrue as anticipated.

Financial Profile Review: Comprehensive Liquidity, Capital, and Profitability Insights

Historical performance (annual)

|

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 42 | -39 | 17 | +17.1% |

| 2024 | 36 | 274 | 7 | +23.9% |

| 2023 | 29 | 443 | 8 | +12.2% |

| 2022 | 26 | 1189 | 10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 184 | -56 | 1.9 |

| 2024 | 20 | 267 | 1.6 |

| 2023 | 5 | 435 | 1.4 |

| 2022 | 442 | 1180 | 1.3 |

Source: SEC companyfacts cache [F1].

Reflecting on the latest fiscal data supported by annual SEC filings through YE2025 [F1], Hilltop’s consolidated equity stands near $2.17 billion. Net income advanced approximately +17% year-over-year reaching $41.58 million signaling profitable incremental earnings gains albeit modest relative returns given ROE around 1.9% using net income over equity proxy — consistent with mid-tier regional bank profiles balancing capital conservatism against growth ambitions.

Operating cash flow turned negative ($-38.7 million) for FY2025 after capital expenditures of $16.8 million increased noticeably (+136% YoY), yielding free cash flow deficits (~$55 million). This pattern reflects reinvestments into operational infrastructure or technology upgrades possibly tied to broker-dealer enhancements or mortgage channel digitization components.

Total debt outstanding is approximately $150 million with an implied net debt surplus position of about -$337 million as of 2025 year-end, reflecting a strong liquidity buffer and conservative leverage stance [F1]. Cash & equivalents were $487 million as of 2017 year-end, with no more recent explicit liquidity disclosures available [F1]. This balance sheet strength supports discretionary capital deployment including stock buybacks [$184 million repurchased FY2025], demonstrating effective use of financial resources [F1], [S2], [S3].

Dividend policy continuity is indicated by regular quarterly payments ($0.72 total declared calendar year 2025) aligning dividend capacity with subsidiary profit flows subject to regulatory restrictions limiting upstream transfers from regulated entities as highlighted earlier.

|

| FY | Net Income | CFO YoY % | Capex YoY % | Equity | Dividends Paid | Buybacks |

|---|---|---|---|---|---|---|

| 2025 | $41.58M | -114% | +136% | $2.168B | N/A ($0.72/share) | $184M |

| 2024 | $35.52M | +283% | -16% | $2.189B | N/A | $19.86M |

| 2023 | $28.67M | -38% | -13% | $2.123B | N/A | $5.10M |

In summary, Hilltop Holdings manifests a cautiously expanding yet resilient multi-segment financial services platform anchored geographically in Texas complemented by national mortgage origination reach plus diverse brokerage capabilities bolstered by disciplined risk governance frameworks supporting measured growth despite competitive headwinds and regulatory complexities.

This analysis is based on publicly available SEC filings through April 2026 along with relevant company disclosures; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments