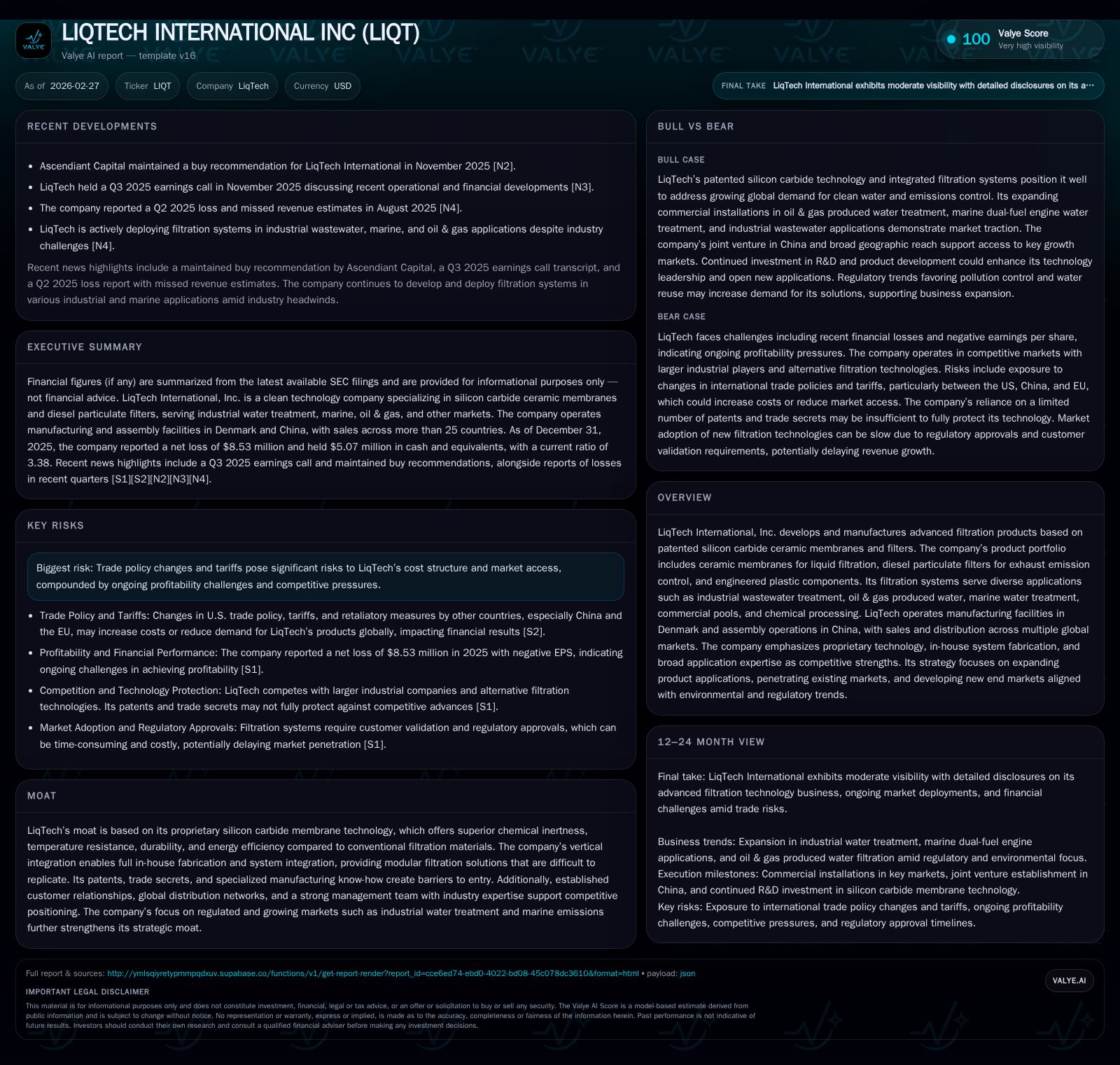

LiqTech International’s Silicon Carbide Edge Sharpening Future Filtration Markets

LiqTech leverages its patented silicon carbide membranes and vertically integrated manufacturing to address complex filtration challenges across industrial and marine sectors.

LiqTech International, Inc. specializes in advanced filtration solutions utilizing proprietary silicon carbide ceramic membranes that provide superior durability and efficiency. Despite persistent net losses and negative cash flows over recent years, the company has demonstrated incremental operational improvements supported by a highly differentiated technology moat. Its strategic focus on expanding applications in industrial wastewater, marine water treatment, and oil & gas produced water positions the firm to capitalize on tightening environmental regulations and growing filtration demand worldwide. Trade policy risks and ongoing profitability hurdles remain key challenges to monitor.

From Innovation to Execution: LiqTech’s Historical Financial Trajectory

LiqTech International's financial results over the last four fiscal years reveal a company striving to improve operational performance despite continuing net losses. Operating income losses receded gradually from approximately -$12.5 million in 2022 down to -$8.3 million by the end of 2025, marking a relative improvement of roughly 33% over this period [F1]. Similarly, net losses narrowed from about -$14.2 million in 2022 to -$8.5 million in 2025.

This trend indicates effective cost containment amid ongoing investments into technology development and market expansion. However, profitability remains elusive as reflected in an approximate return on equity near -82% for FY2025 given diminishing shareholder equity from $23.3 million at end-2022 to just over $10.4 million by end-2025 [F1].

Operating cash flows have consistently been negative but showed improvement from -$12 million in FY2022 to roughly -$6.1 million by FY2025. Notably, capital expenditures contracted sharply by over 70% year-over-year down to $395 thousand in 2025 from $1.37 million in 2024, signaling restrained capex commitment amidst liquidity conservation efforts [F1]. Cash reserves of approximately $5.1 million as of December 31, 2025 support near-term operational stability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -9 | -6 | -8 | 0 | +17.6% |

| 2024 | -10 | -8 | -9 | 1 | -20.7% |

| 2023 | -9 | -4 | -8 | 3 | +39.5% |

| 2022 | -14 | -12 | -13 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -81.7 |

| 2024 | -9 | -62.1 |

| 2023 | -7 | -49.6 |

| 2022 | -14 | -60.8 |

Source: SEC companyfacts cache [F1].

Table: LiqTech Historical Financial Summary (FY2022–FY2025) per latest reports [F1]

The persistent negative profitability underscores that while LiqTech's operations are improving sequentially as product innovation takes hold and scale benefits accrue, reaching sustainable earnings remains a work in progress.

Decoding Proprietary Technology: The Silicon Carbide Membrane Advantage

At the core of LiqTech's competitive strength is its silicon carbide (SiC) ceramic membrane technology — a material choice providing distinct advantages rarely matched by polymer or aluminum oxide alternatives [S11]. These tubular membranes employ a crossflow configuration designed to handle liquid streams laden with high suspended solids concentrations such as those found in oil & gas produced water or petrochemical wastewaters.

Critical attributes of SiC include exceptional chemical inertness enabling compatibility with harsh fluids; outstanding temperature resistance allowing operation under severe thermal conditions; and remarkable mechanical hardness—second only to diamond—ensuring membrane longevity even amidst abrasive environments [S11]. The hydrophilic nature of SiC substrates yields high flux rates resulting in energy-efficient filtration processes.

Additionally noteworthy is LiqTech’s hybrid technology membrane (HTM), combining SiC with zirconia ceramics to produce membranes with ultrafiltration pore sizes (~60 nm), unlocking new separation capabilities particularly suited for advanced industrial process streams [S18].

This proprietary silicon carbide technology is further protected by granted patents across Europe and Denmark alongside multiple pending international applications reinforcing barriers against replication [S12].

The vertical integration approach whereby LiqTech retains full control over the fabrication of these membranes and their incorporation into modular liquid filtration systems enables precise quality assurance and system-level optimization inaccessible to competitors reliant on outsourced components [S5][S11]. In-house engineering supports design sophistication including 3D modeling and automation controls enhancing system performance consistency.

Furthermore, LiqTech’s ceramic diesel particulate filters (DPFs) leverage similar SiC substrate expertise producing high-efficiency soot removal components addressing increasingly stringent global diesel emissions mandates spanning European urban low-emission zones through emerging marine black carbon regulations [S11][S24].

Market Penetration and Expansion: Tactical Growth Drivers and Barriers

LiqTech serves an array of markets wherein both technical product differentiation and regulatory impetus converge favorably:

- Industrial Wastewater Treatment: Targeting difficult-to-treat streams such as heavy metals removal from mining wastewater or process waters from steel production has yielded promising installations highlighting operational cost reductions and product quality improvements [S14][S25].

- Oil & Gas Produced Water: Growing demand for effective produced water treatment driven by reinjection needs and discharge regulation tightening fuels adoption of robust SiC membrane systems including recent deployments via its QureFlow™ containerized units capable of handling capacities starting at ~10k barrels/day [S25].

- Marine Water Treatment: Positioned well for servicing dual-fuel commercial vessels with exhaust gas recirculation needs aligned to IMO emissions requirements; assembly joint ventures established in Nantong China aim to reduce production costs proximate to shipbuilding clusters where ~70-80% of vessels are manufactured globally [S14][S21].

- Commercial Pool Filtration: Application-specific Aqua Solution® systems deliver energy-efficient disinfection with reduced chemical use tapping into a projected European market growing at a CAGR above 6%, expanding via distributors into Asia-Pacific as well [S21].

Sales utilize a combination of direct efforts supplemented by distributor networks spanning China, Korea, Europe (Spain/UK/France/Greece), Middle East and USA enabling worldwide reach though trade tariffs risk remains pertinent especially amid increased US tariffs impacting China/EU trade flows since early/mid-2025 [S9][S13]. The company has accumulated inventory buffers which have so far mitigated immediate margin deterioration but longer-term tariff escalation poses downside exposure.

System integrator partnerships also provide locked-in customer bases due to costly regulatory approvals constraining rapid supplier switching once installed validating strong switching costs for LiqTech's products embedded within larger filtration plants [S12]. However reliance on trade policies outside management control alongside tight profitability margins may cap growth at intermediate stages.

Strategic Outlook: Emerging Opportunities and Industry Tailwinds

LiqTech’s strategic roadmap centers on exploiting its core silicon carbide platform across new applications while deepening penetration within current end-markets:

- Continuous innovation pursues expanding capabilities beneficial to chemical/petrochemical purification processes where water purity directly correlates with product output quality enhancing client ROI profiles [S7][S25].

- Environmental regulatory trends globally towards stricter emission controls—ranging from municipal wastewater purification standards to maritime black carbon limits—provide sustained demand tailwinds helping build pipeline opportunities particularly within regulated geographies balancing existing competitive forces [S24][S25].

- Aftermarket service sales including maintenance contracts and spare parts represent an additional revenue stream targeting enhanced customer engagement leveraging an installed base approaching hundreds of units worldwide reducing client technical support friction points [S21].

- Continued development of intellectual property safeguards targeting enhancements around cross-flow integrated systems sustains long-term differentiation prospects amid increasing competitor attention.

While explicit forward guidance was not disclosed publicly at filing date for FY26 or onward horizons necessitating forward-looking analysis caution; management commentary suggests positive momentum transitioning toward scaled commercial success reliant on continued market expansion execution plus macroenvironmental stability for tariffs regulatory framework sensitive markets.

Capital Allocation Review: Cash Flows and Investment Priorities

Financial stewardship reflects a disciplined approach balancing R&D investments against operational cash burn constraints:

- Free cash flow (operating cash flow minus capex) remained negative at roughly –$6.5 million for FY2025 despite notable capex curtailment exceeding –70% YoY down to $395k indicating shrinking fixed asset investment aligned with prioritizing liquidity preservation amidst loss-making status quo [F1][S24].

- No dividends or share repurchases occurred recently nor planned underscoring reinvestment prioritization focused chiefly on developing product technologies along with expanding sales reach rather than capital returns execution given precarious profit profile.

- Equity erosion yearly from about $23.3 million at end-FY22 down to just above $10.4 million entering FY26 marks mounting cumulative net loss impact creating modest balance sheet leverage though reasonable current ratios (~3.38x) support adequate short-term solvency positioning at present [F1][S16][S17].

Overall capital allocation underscores cautious resource utilization while investing strategically especially around R&D staffing notably lean six-person teams dedicated specifically toward advancing manufacturing automations patents alongside core membrane chemistry improvements reflecting precision focus rather than scale-driven expenditure expansion common among peers potentially less specialized technically.[S6][S24]

Regulatory Impact and Geopolitical Risks Shaping Business Dynamics

Tariffs remain the most material external risk factor influencing raw material costs—the primary inputs include silicon carbide powder itself plus steel components pumps plastics platinum palladium — all susceptible price volatility due to global trade uncertainty centered chiefly on US-China-EU relations post mid-2024 tariff escalations implementation phase noted explicitly within risk disclosures dating back through successive SEC filings starting early-mid 2025 reflecting evolving barriers restricting free cross-border flows possibly compressing global volume growth opportunities or margins alike until resolution ensues.[S9][S13]

Furthermore tightening emissions norms such as EU diesel particulate regulations coupled with increasingly fragmented local low emission zones incentivize product uptake yet simultaneously impose compliance complexities potentially slowing adoption curve pace.[S24] Litigation occasionally arises typical within manufacturing sectors but no unusual legal contingencies were highlighted recently.[S4]

Overall geopolitical tension acts as a double-edged sword boosting demand drivers supported regulatory incentives while imposing tariff-related headwinds potentially inflating supply chain costs or limiting access particularly into critical fast-growing Asian industrial node markets jeopardizing near term financial outcomes absent proactive mitigation responses implemented timely.[S10]

Operational Footprint and Manufacturing Strategy Enhancing Competitive Moat

LiqTech’s manufacturing operations center around its Danish facilities focusing on ceramic membrane reaction sintering fabrication plus DPF filter production benefiting from concentrated R&D proximity promoting quick cycle improvement feedback loops.[S6] It complements this foundation via assembly operations relocated strategically into Nantong China since late 2024 enabling proximity advantages close to maritime shipyards thus reducing logistics costs serving marine dual-fuel engine market segments substantively.[S14] The firm actively evaluates additional US partnerships aiming further capacity scale enhancing domestic footprint diversification balancing currency labor cost structures geo-political risks uniquely attendant regionally.[S6] Such vertical integration encompassing complete fabrication through system level assembly allows tight control over corrosion-resistant component sourcing system integration quality control automated proprietary techniques such as advanced process design along with sophisticated three-dimensional CAD modeling guidance enabling production precision supporting strong reliability benchmarks driving customer trust hard-to-replicate externally sourced models typically.[S20] Patents combined with extensive application expertise constitute significant intellectual property assets creating substantive entry barriers reinforcing formidable moat protecting proprietary membrane chemistry hybrid composite filters competitive positioning against large incumbent poly/membrane suppliers lacking similar process mastery or vertical scope.[S11]

What to Watch: Key Forward-Looking Indicators and Catalysts

In absence of explicit company forecasts or public milestones defining timelines through FY26+, several metrics warrant attention moving forward:

- Progression scaling commercial shipments particularly ramping dual-fuel marine scrubber water treatment system deployments linked closely with vessel retrofit/on-order cycles facilitates validation of addressable market capture ambitions.

- Evolving US-China-EU tariff landscape developments remain critical as further escalation or relaxation will influence cost base sustainability alongside geographic revenue distribution effects.

- Successful patent prosecutions broadening IP portfolio breadth plus expansions consistent R&D outputs sustaining differentiation will secure longer-term competitive advantages soliciting investor interest.

- Growth trajectories in aftermarket services blending upgrades spares maintenance contracts signal increasing client account depth generating recurring revenue streams stabilizing overall business model robustness under cyclical downturns.

- Industrial segment penetration gains visible via new case studies demonstrating measurable value add underpin future sales funnel health providing confidence regarding application diversification alleviating end-market concentration risks. Keeping tabs on quarterly earnings releases management commentary related pipeline momentum adjustment further sharpens insight refining expectation calibration adequately navigating still dynamic market stages ahead without definitive guidance presently released.

This analysis synthesizes publicly disclosed regulatory filings from LiqTech International as of February 27th, 2026 alongside proprietary financial data up to fiscal year-end December 31st, 2025 emphasizing factual recounting without investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments