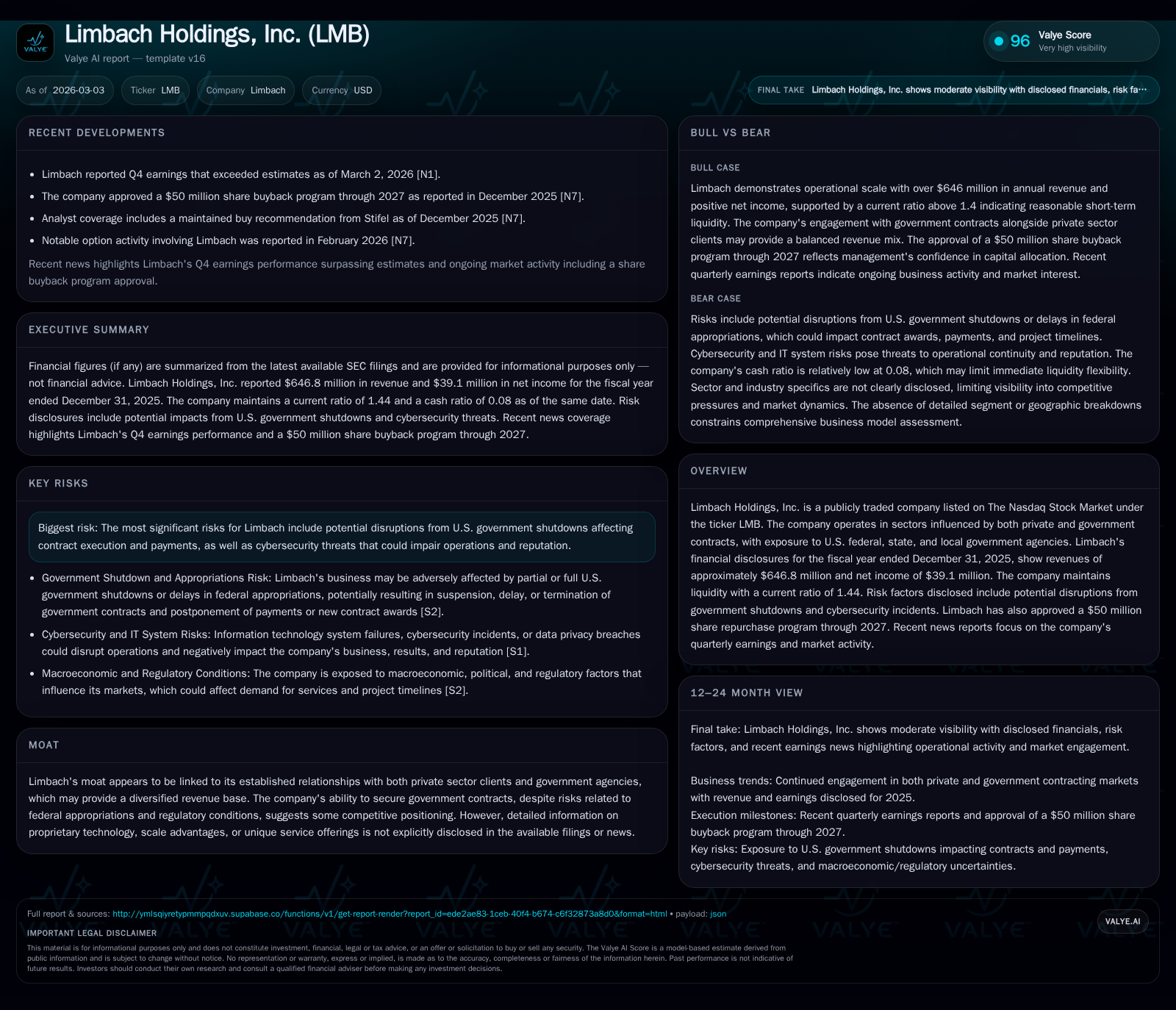

Limbach Holdings: Revenue Surge, Contract Risks, and Share Repurchase Ambitions

Limbach posted a substantial financial upswing in 2025, while government-related risks and capital return initiatives shape its strategic outlook.

Limbach Holdings achieved robust revenue and profit growth in FY2025, fueled by operational efficiencies and a favorable contract mix. Despite this momentum, the company remains exposed to significant government-related risks including potential shutdowns and cybersecurity threats. A newly authorized $50 million share repurchase program signals management’s intent to optimize capital structure and enhance shareholder returns. Investors should monitor government contracting cycles and risk mitigation efforts closely as key drivers of near-term performance.

Robust Momentum: Analyzing Limbach’s Recent Growth Trajectory

Limbach Holdings demonstrated notable financial acceleration through the fiscal year ended December 31, 2025. Revenue climbed sharply by 24.7% to $646.8 million from $518.8 million in 2024 [F1], marking a meaningful uplift after modest flatness between FY2023 and FY2024.

Operating income expanded even more rapidly, climbing 28% to $49.5 million versus $38.6 million the prior year [F1]. This progression resulted in improved operating margins suggesting combination of streamlined operations and advantageous project mix. Net income followed suit, rising by approximately 26.5% to $39.1 million from $30.9 million in FY2024 [F1], translating into an estimated return on equity approaching 20%, given year-end equity of $195.7 million [F1].

From a cash flow perspective, operating cash flow reached $45.7 million — up 24.2% year over year — while capital expenditures were halved from prior levels at $3.8 million in FY2025 compared with $7.5 million in FY2024 [F1]. This divergence enabled free cash flow generation exceeding $41 million, indicative of effective capex discipline during expansion.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 647 | 39 | 46 | 49 | +24.7% | +26.5% |

| 2024 | 519 | 31 | 37 | 39 | +0.5% | +48.8% |

| 2023 | 516 | 21 | 57 | 29 | +3.9% | +205.3% |

| 2022 | 497 | 7 | 35 | 12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 42 | 20.0 | |

| 2024 | 0 | 29 | 20.1 |

| 2023 | 0 | 55 | 17.2 |

| 2022 | 2 | 34 | 7.1 |

Source: SEC companyfacts cache [F1].

This performance acceleration underscores Limbach’s ability to leverage its operational footprint amid dynamic market conditions.

Contractual Foundations and Market Dependencies: The Role of Government and Private Sector Orders

Limbach’s business model hinges on a carefully balanced portfolio composed primarily of private sector projects coupled with work under numerous contracts with U.S federal, state, and local government agencies [S1][S2][S5]. This client diversity creates a moat rooted in established relationships across both arenas.

However, the complexity inherent to government contracting introduces variability tied to political processes and funding cycles—constraints endemic to federal appropriations mechanisms common in infrastructure-related firms within the engineering and construction domain.

The company’s backlog visibility typically extends through multiple upcoming quarters with new contract awards crucially timed against federal budget enactment schedules—factors known sector-wide for causing periodic volatility especially during fiscal uncertainties or prolonged appropriations delays .

Further complicating demand visibility is reliance on governmental regulatory approvals impacting project starts or permitting timelines—an acknowledged friction point that can postpone revenues or extend working capital needs temporarily [S2]. Limbach’s positioning therefore reflects a nuanced tradeoff: access to relatively stable long-duration contracts balanced against unpredictability stemming from legislative bottlenecks.

Emerging Risks: Government Shutdown Implications and Cybersecurity Challenges

Among the most salient risks Limbach flags are potential U.S government shutdowns or delays in federal appropriations which could materially affect contract execution velocity or lead to suspensions of work orders altogether [S2][S7]. Payments under existing contracts may also be postponed during such interruptions—introducing liquidity strain.

Moreover, customers’ dependence on government funding or approvals further amplifies sensitivity as shutdown-induced deferments ripple through suppliers and partner ecosystems slowing decision-making processes broadly across the sector [S2]. These phenomena pose systemic headwinds that could stall project commencement or escalation.

In parallel, Limbach identifies information technology system failures including cybersecurity incidents as critical operational vulnerabilities—with any breach potentially disrupting construction scheduling or damaging corporate reputation among public and private stakeholders alike [S1][S9]. Given growing cyber threats targeting infrastructure companies recently seen across industry peers, this complexity warrants constant diligence.

Taken together these intersecting risks embody typical challenges faced by firms entwined with government contracting cycles and infrastructure-sensitive sectors.

Capital Allocation Focus: Share Buybacks, Liquidity Position, and Return on Equity

Reflecting confidence supported by recent cash flow strength and balance sheet resilience (current ratio ~1.44 at end-2025), Limbach’s board authorized a sizable $50 million share repurchase program through December 15, 2027 [N1][S6][F1]. This initiative permits flexible stock acquisitions in open market transactions or other methods aligned with prevailing securities regulations.

The buyback authorization notably complements the company’s organic growth trajectory without imposing mandatory repurchase volumes or timelines—preserving discretion based on market conditions while signaling proactive capital deployment intent.

At fiscal year-end equity of approximately $195.7 million alongside net income of $39.1 million suggesting an ROE near the robust level of ~20%, management appears focused on enhancing per-share metrics prudently amidst ongoing expansion rather than initiating dividends currently as no dividend payments are disclosed [F1].

Operating cash flow trended positively at $45.7 million while capex reduction bolstered free cash flow generation—a favorable underpinning enabling sustainable buybacks without stressing liquidity buffers.

This balanced capital allocation strategy aims at supporting shareholder value through earnings growth reinforcement alongside thoughtfully timed buybacks rather than yield-centric distribution—which aligns well with peer construction & engineering firms emphasizing reinvestment for backlog capitalization.

What Investors Should Monitor Next: Potential Milestones and Market Catalysts

Looking ahead, explicit forward guidance remains limited; however industry observers should track several fundamental indicators shaping Limbach’s trajectory closely:

- Timing and scale of new U.S government contract awards relative to federal appropriations cycles are primary levers affecting revenue cadence given reported meaningful exposure within backlog composition [N3].

- Progress on cybersecurity infrastructure upgrades or incident mitigation will be important markers mitigating operational risk disruptions flagged repeatedly in filings [N3].

- Execution pace of the share repurchase program: stock price response to buyback announcements or activity may affect investor perceptions about balance sheet optimization efficacy alongside organic earnings momentum [N3].

- Macro-political developments influencing public spending budgets directly impact order visibility among contractors specializing in governmental work; thus broader economic signals warrant consideration.

By focusing on these catalysts without extrapolating speculative forecasts beyond available disclosures investors gain grounded insight into Limbach's evolving enterprise value drivers.

This analysis leverages publicly filed financial data along with regulatory risk disclosures specific to Limbach Holdings as of early March 2026; it does not constitute investment advice but aims at providing transparency into company fundamentals amidst sector-specific complexities typical for engineering-driven contractors exposed to governmental procurement dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments