Mega Matrix Inc Advances AI-Driven Content Strategy After Fiscal Year Loss

Mega Matrix improves operational efficiency and adopts AI-generated content amid a challenging short drama streaming market.

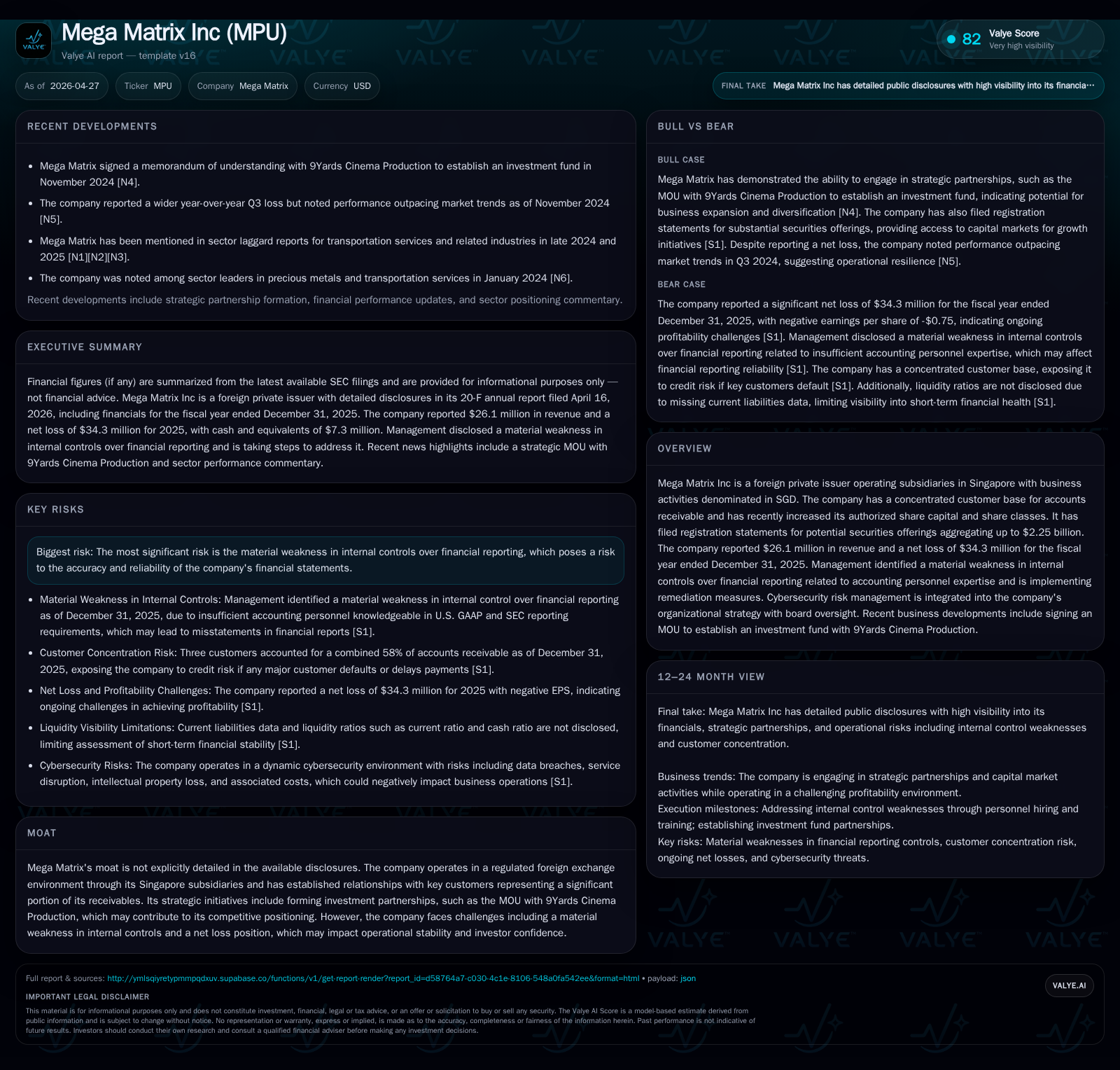

Mega Matrix Inc reported an improved adjusted EBITDA loss in fiscal 2025 despite a widening net loss, reflecting progress in operational discipline amid fierce industry competition. The company has pivoted from capital-intensive self-produced dramas to an asset-light content procurement model, enhancing margin stability and user monetization on its FlexTV platform. Launching AI-driven short drama production is a strategic move aimed at reducing costs and expanding its global user base. However, risks such as material weaknesses in internal financial controls and customer concentration remain notable.

Fiscal Year 2025 Operating Results and FY End Update

Mega Matrix Inc’s latest quarterly disclosure incorporated into the April 16, 2026 Form 6-K highlights a nuanced operating performance for fiscal year 2025. The company reduced its adjusted EBITDA loss to $5.6 million from $7.1 million in the prior year, signaling improved operational leverage through disciplined cost management despite intensified competition across the global short drama streaming space [S2][S9]. However, this improvement occurred against a backdrop of a significantly larger net loss of $34.3 million, partially attributed to substantial one-time share-based compensation expenses totaling approximately $19.4 million and digital asset fair value fluctuations [F1][S9].

The overall revenue totaled approximately $26.1 million for the year ended December 31, 2025, reflecting pressure on top-line growth yet mitigated by higher average revenue per user (ARPU), which rose to $3.42 from $3.15 the previous year due to enhanced subscription conversion rates and retention policies [F1][S17][S19]. Advertising expense intensity declined materially as a percentage of revenue from 62% in 2024 to 47%, underscoring more efficient marketing spend aligned with improved organic user acquisition initiatives.

Transitioning Business Model: From In-House Production to Asset-Light Content Procurement

Mega Matrix has implemented a strategic pivot away from capital-intensive self-produced short drama content towards an asset-light model emphasizing licensed content procurement for its FlexTV platform hosted by its subsidiary Yuder Pte Ltd [S1]. FlexTV delivers curated English, Japanese, and Thai language short dramas translated into multiple languages spanning North America, Europe, Southeast Asia, and other international markets [S1]. This transition reduces upfront production capital requirements while providing platform flexibility to source high-demand content rapidly.

Geographically diverse filming operations—including locations such as the U.S., Mexico, Australia, Japan, Thailand, and the Philippines—have facilitated access to international storytelling styles resonating with global audiences [S1]. This diversified approach aids in scaling without proportional increases in fixed costs or balance sheet investments. The asset-light orientation also allows prompt adaptation to shifting user preferences with content licensing agility.

Competitive Dynamics in Global Short Drama Streaming

The broader short drama streaming industry is characterized by soaring user acquisition costs amplified by competitors’ aggressive marketing tactics and persistent operating losses across peer groups [S1]. Amid this saturated player landscape where differentiation is challenging, Mega Matrix’s improvement in ARPU against reduced advertising-to-revenue ratios signals measured success in balancing marketing expense efficiency with subscriber monetization.

Driving organic growth through enhanced social media engagement forms part of the company’s refined go-to-market strategy designed not only to reduce paid acquisition reliance but also to build community-driven retention advantages [S1]. Despite these efforts, competitive pressure remains significant given rising global consumer options for bite-sized entertainment formats.

AI Adoption as a Strategic Growth Enabler

A pivotal development disclosed in March 2026 involves Mega Matrix’s initiative to deploy artificial intelligence technologies for short drama production underpinned by their OpenClaw-based enterprise operations [S3]. This marks a forward-looking agenda to harness AI capabilities to automate aspects of scriptwriting, post-production editing, or even casting simulations.

Integrating AI-generated content promises dual benefits: substantially lowering production costs relative to traditional filmmaking processes and accelerating pipeline throughput enabling faster refresh rates of new releases [S3][S1]. The strategic ambition targets long-term profitability improvements via this technology adoption while simultaneously broadening appeal across demographics attuned to novel narrative styles afforded by algorithmic creativity.

Structural Risks: Internal Controls & Customer Concentration

Significant structural risks shadow Mega Matrix’s operational profile stemming from an acknowledged material weakness in internal controls over financial reporting related primarily to personnel expertise deficits [S1]. This deficiency currently undermines confidence in the completeness and accuracy of financial disclosures until remediation measures take full effect.

Further risk arises from the company’s concentrated accounts receivable exposure: as of December 31, 2025, three customers constituted roughly 58% of total receivables (22.5%, 19.7%, and 15.8%), intensifying credit risk vulnerability should any client default or delay payments [S6]. Such concentration demands vigilant credit assessment practices alongside diversification efforts over time.

Corporate Governance Focus on Cybersecurity and Regulatory Compliance

Mega Matrix embeds cybersecurity risk management at the strategic level under explicit oversight by its Board of Directors [S1]. Considering that the core business relies on uninterrupted operation of digital streaming infrastructure protecting proprietary content and safeguarding user data privacy is paramount.

The company employs comprehensive technical safeguards comprising firewall defenses, intrusion detection/prevention systems (IDS/IPS), rigorous access controls adhering to least privilege principles, plus encryption protocols for data both at rest and during transmission [S1]. Regular cyber risk assessments via penetration testing and threat intelligence updates bolster situational awareness.

Incident response frameworks are documented and rehearsed ensuring prompt mitigation actions minimizing service disruption or reputational damage in case of breaches [S1]. Third-party vendor security vetting complements internal controls mitigating supply chain risks.

Key Milestones to Monitor: Content Integration, User Metrics, and Capital Initiatives

Important upcoming milestones focus initially on successful scaling of AI-generated content into FlexTV's programming lineup beyond pilot phases; meaningful headcount or unit economics improvements linked directly to this rollout will be telling indicators [S2][S3].

User engagement tracking metrics such as subscriber base growth rates juxtaposed with ARPU trends will help validate monetization strategies amid evolving competition pressures [S2][S9][S17]. Watch also for shifts in organic versus paid acquisition channel effectiveness reflecting marketing optimization success.

On the capital front, Mega Matrix continues utilizing At-The-Market (ATM) equity offerings alongside private placements approved through shareholder resolutions expanding authorized share capital notably [S1][S16][S21]. Proceeds fund working capital requirements plus investments supporting growth ambitions including technology enhancements.

Financial Overview: Navigating a Net Loss Amid Operational Efficiencies

Summarizing Mega Matrix’s recent financial trajectory reveals ongoing challenges marked by escalating net losses reaching $34.3 million for fiscal year ending December 31, 2025 compared to $10.5 million prior year results driven partly by high share-based compensation charges relating to equity grants totaling about $19.4 million non-cash expenses [F1][S9][S15].

Despite these headwinds, adjusted EBITDA losses narrowed notably reflecting tightened operational spending discipline alongside revenue mix shifts favoring higher-margin licensed content distribution rather than content creation capex-intensive activities [F1][S9][S17].

Cash position stood at approximately $7.3 million at year-end supported partly by equity raises via ATM programs generating $2.8 million incremental funding during calendar year 2025 plus earlier private placement proceeds providing liquidity for ongoing operations while pursuing strategic transformation goals [F1][S10][S20].

This analysis synthesizes publicly filed SEC documentation up through April 16, 2026 concerning Mega Matrix Inc., blending operational disclosures with strategic context while grounding financial highlights strictly in reported figures. It aims solely at informing an understanding of MPU’s current positioning within the global short drama streaming sector without extending investment recommendations or price commentary.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments