Douglas Dynamics: Solid Moat and Operational Agility Shape Financial Trajectory

Douglas Dynamics leverages its extensive distributor network and lean manufacturing to sustain resilience amid weather-driven demand variability.

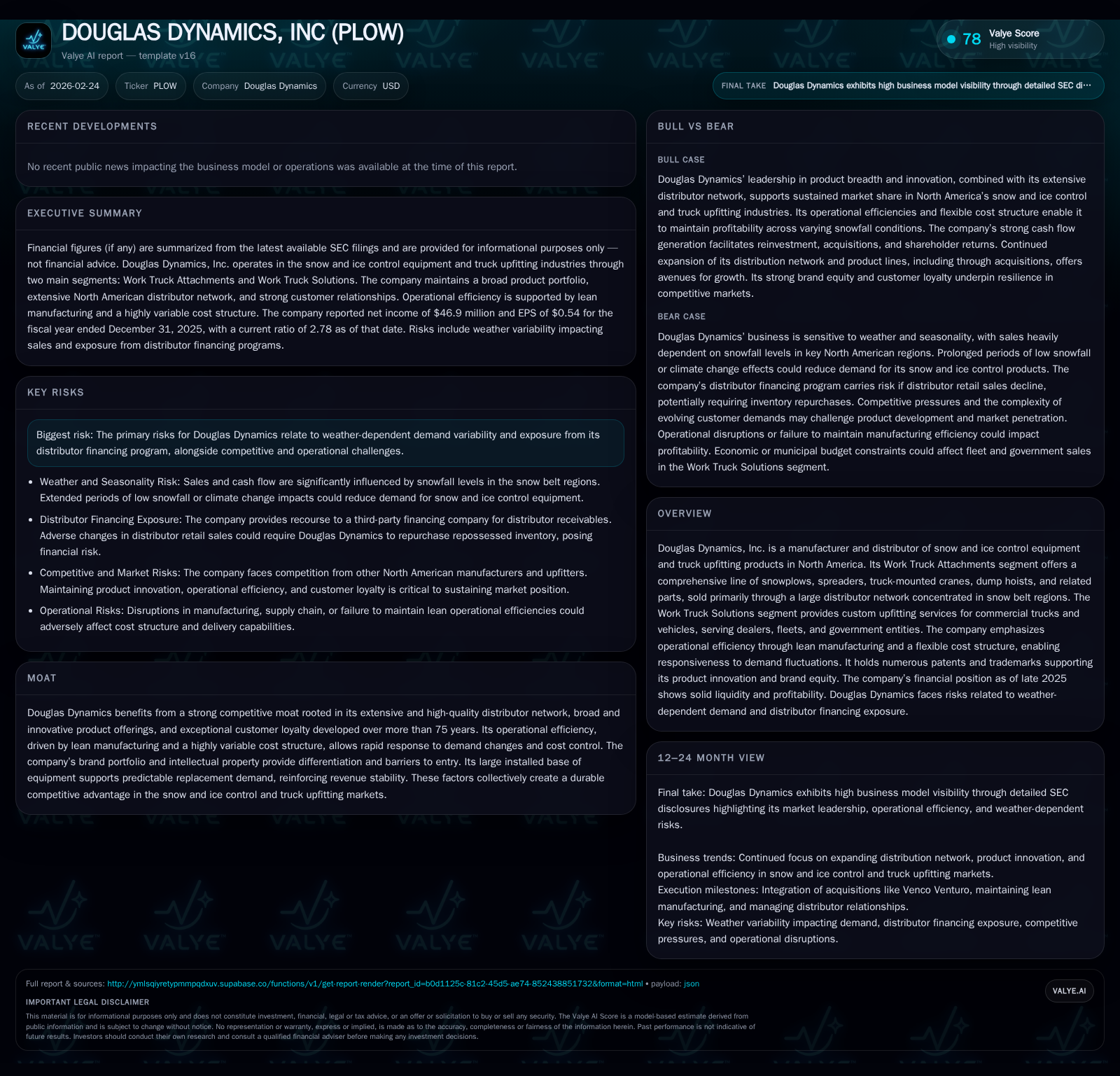

Douglas Dynamics, a leading North American manufacturer of snow and ice control equipment and truck upfitting products, demonstrates a strong operational model anchored by lean manufacturing and a robust distributor network. Despite a 17% drop in operating income in FY2025 driven by light snowfall, operating cash flow surged 81.6% aided by efficient asset management and pre-season ordering programs. The company’s solid capital allocation strategy balances dividends and incremental buybacks while maintaining liquidity. Going forward, growth depends on expanding market share in heavy-duty segments, driving product innovation, and managing inherent weather-related risks alongside exposure from distributor financing.

Growth Trajectory and Performance Drivers Through Recent Years

Douglas Dynamics operates in niche segments—primarily snow and ice control equipment through its Work Truck Attachments segment and commercial truck upfitting via Work Truck Solutions—both heavily influenced by North American snowfall patterns. Over recent years ending FY2025, the company’s financial performance has exhibited marked variability consistent with weather-dependent demand dynamics.

Operating income rose from $44.9 million in FY2023 to $88.7 million in FY2024 as snowfall normalized after relatively mild prior seasons; however, FY2025 saw a retracement to $73.6 million, representing a 17% decline year-over-year [F1]. Net income similarly followed this trajectory with a dip to $46.9 million (-16.5% YoY). Contrasting these income figures, operating cash flow grew robustly by 81.6% to nearly $74.7 million in FY2025—reflecting exceptional working capital controls and disciplined pre-season order management designed to smooth supply chain utilization despite seasonality.

Capital spending increased moderately (+39.5%) to $10.8 million as the company invested selectively in manufacturing capabilities and product development infrastructure [F1]. Taken together, the financials illustrate Douglas Dynamics’ ability to preserve cash generation even when top-line pressures emerge from weather headwinds.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 47 | 75 | 74 | 11 | -16.5% |

| 2024 | 56 | 41 | 89 | 8 | +136.7% |

| 2023 | 24 | 12 | 45 | 10 | -38.6% |

| 2022 | 39 | 40 | 59 | 12 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 28 | 6 | 64 |

| 2024 | 27 | 0 | 33 |

| 2023 | 27 | 0 | 3 |

| 2022 | 27 | 6 | 28 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available; Buybacks restarted after hiatus in FY2024.

Operational Excellence: Lean Manufacturing and Cost Flexibility

At the core of Douglas Dynamics’ resilience lies its lean enterprise platform that blends vertically integrated manufacturing with flexible labor deployment strategies allowing rapid scale adjustments aligned with fluctuating seasonal demand [S5][S6][S14]. Its primary owned facility in Rockland, Maine supplements leased plants across multiple states including Wisconsin and Illinois, enabling geographic diversification of production capacity.

This infrastructure supports tight inventory control via a pre-season order program incentivizing distributors’ early commitments ahead of retail selling seasons—a mechanism that enhances asset utilization rates while minimizing raw material excesses [S5]. Approximately 10-15% of the workforce comprises temporary labor during average snowfall years, underscoring cost variability allowing wage expense scalability reflective of actual output needs.

Moreover, integration of process improvement tools into product development cycles reduces time-to-market for innovations while mitigating costs—fortifying margins particularly when unit volume volatility persists.

Distributor Network: Foundation of Competitive Moat

Douglas Dynamics commands arguably the industry’s most extensive distributor footprint with around 3,000 points of sale concentrated within snow belt regions spanning Midwest through Northeast US states into Canadian provinces [S4][S7][S8]. This exclusive network benefits from longstanding relationships fostered over decades coupled with bailment agreements enhancing inventory turnover efficiency.

Distributors function not only as sales channels but also gather critical real-time end-user intelligence on changing requirements and inventory levels; enabling rapid responsiveness on both production planning and design fronts [S14]. Floor plan financing arrangements with original equipment manufacturers supplying truck chassis further integrate the supply chain ensuring reliable delivery of finished upfitted vehicles under Work Truck Solutions.

Majority exclusivity among distributors creates significant entry barriers deterring competition while fostering high brand loyalty—integral given that replacement sales dominate due to equipment lifecycle averaging approximately nine to twelve years dependent on usage conditions [S17].

Product Innovation and Market Expansion Strategies

Continuous product innovation remains pivotal as Douglas Dynamics expands beyond snowplows into complementary offerings such as truck-mounted cranes and dump hoists following the strategic acquisition of Venco Venturo in late FY2025 [S8][S23]. This expanded portfolio increases addressable markets within both light- and heavy-duty vehicle categories.

Within Work Truck Attachments, new product introductions focus on enhanced durability, ease-of-use features integrated with lean manufacturing advances reducing cost curves; while Work Truck Solutions intensifies targeting municipal/government fleet customizations leveraging proprietary DDMS processes supporting specialized upfits [S5][S25].

Market expansion initiatives explicitly seek greater penetration where market share rests below estimated thresholds (e.g., less than half) especially targeting heavy-duty truck usage sectors that historically show fragmented competitive landscapes [S5]. Meanwhile cross-selling efforts leverage brand synergies across distributor bases aiming at maximizing wallet share per customer with bundled solutions inclusive of parts/accessories that yield higher margins albeit smaller revenue components [S8].

Financial Health and Capital Allocation Priorities

Douglas Dynamics’ balance sheet as of December 31, 2025 shows equity capital approaching $281 million underpinning stable capitalization supporting ongoing investments alongside shareholder returns [F1][S13]. Cash flow generation remains robust despite income volatility driven by manageable capex typically hovering near $10 million annually reflecting asset-light expansion complemented by lease arrangements including sale-leaseback transactions completed earlier [S6][S19].

Return on equity ratio approximates a healthy ~16.7%, corroborating operational profitability metrics resilient through cyclical fluctuations [F1]. The dividend has remained consistent around $27–28 million yearly demonstrating commitment to shareholder distributions regardless of short-term earnings oscillations.

Share repurchases have resumed conservatively with $6 million expended in FY2025 after several years without buybacks signaling prudent capital deployment balancing reinvestment needs against sound return optimization [F1][S19]. Use of debt appears restrained; liquidity ratios such as current ratio standing near ~2.78 highlight financial flexibility conducive for opportunistic acquisitions or strategic investments as market conditions warrant.

Forecasting Douglas Dynamics’ Path Ahead

Absent explicit forward guidance disclosed recently [N3], critical milestones warranting observation include expansion velocity within distributor networks aiming for geographic deepening or select new market entry through well-capitalized partners [S7][S25]. Success metrics will hinge on effective deployment of newly acquired Venco Venturo assets into core operations realizing synergy targets expected from broader product offerings.

Moreover, wider acceptance rates of DDMS-driven custom upfits correlated with municipal budgets will influence scaled revenue growth trajectories within Work Truck Solutions amid macroeconomic variability impacting procurement cycles.

From an operational angle continued refinement of lean manufacturing adaptation remains essential given persistent challenges posed by fluctuating snowfall patterns altering demand surges unpredictably necessitating nimble response capabilities.

Risks from Demand Cyclicality and Dealer Financing Exposure

Primary risk exposure revolves around variability in snowfall—directly affecting purchase timing for snowplows/spreaders since replacement cycles correlate strongly with winter severity metrics documented historically across monitored snow belt states [S28][F1]. Diminished or delayed snowfall results in postponed replacement demand compressing revenue recognition potentially over multiple fiscal periods generating earnings volatility.

Additionally, dealer financing programs introduce credit contingencies tied to third-party financiers where Douglas Dynamics retains recourse obligations for uncollectible receivables or repossessed inventory losses though history shows minimal credit losses under these arrangements so far [S16][S26]. Any deterioration in distributor retail performance could result in increased inventory repurchase requirements negatively impacting cash flows.

Regulatory factors including climate change policies potentially influencing snowfall patterns or economic slowdowns affecting municipal spending budgets compound these inherent cyclicality risks, underscoring importance of conservative financial management coupled with nimble operational execution modeled by Douglas Dynamics’ entrenched competitive moats.

This report is intended solely for informational purposes based on publicly filed financial disclosures and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments