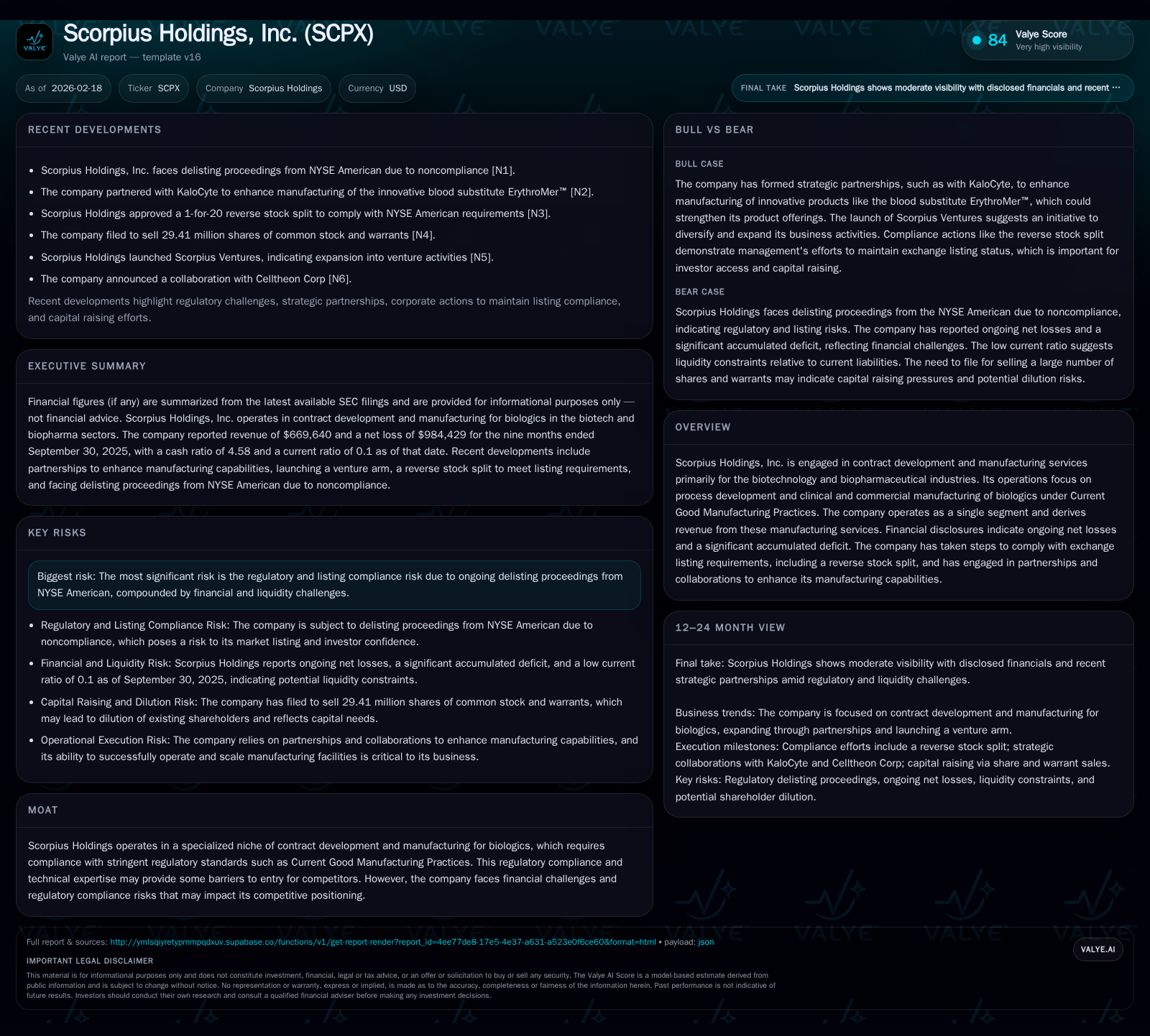

Scorpius Holdings Faces Asset Foreclosure and Compliance Hurdles Amid Operating Losses

The company grapples with a forced asset sale, regulatory delisting, and sustained financial losses, threatening near-term survival.

Scorpius Holdings, Inc. operates in the contract biologics manufacturing niche but has lost its manufacturing assets due to foreclosure by secured noteholders. Despite a history of sporadic revenue gains, the company endures deepening operating and net losses coupled with severe liquidity constraints. Its delisting from NYSE American exacerbates operational risks in a highly regulated sector demanding CGMP compliance. Future prospects hinge on securing strategic transactions amid uncertain capital availability, while current financials reflect a steep negative return on equity and near-zero cash buffers.

Financial Trajectory: From Revenue Gains to Mounting Deficits

Over the past years leading through FY2024, Scorpius Holdings demonstrated significant revenue growth spikes—the latest annual revenue increased by 281.2% from the prior year as evidenced by SEC XBRL data [F1]. This surge likely reflects transient contract wins or ramp-up phases within its CDMO biologics manufacturing operations. However, revenues remain modest relative to accumulated operating expense levels.

Operating losses have remained stubbornly steep but showed a marginal improvement of about 20% YoY in the same period. Nonetheless, these losses totaled over $33 million annually lately with net income following a similar negative trajectory (-27.4% YoY improvement) yet remaining deeply adverse—resulting in an accumulated deficit upwards of $303 million [F1]. This reflects an entrenched burn rate accentuated by fixed-cost overhead typical of biopharmaceutical manufacturing facilities that cannot scale down quickly when facing downturns.

Operating cash flow trends parallel this loss-making stance with heavily negative outflows (~$26 million in FY2024), outpacing capital expenditures which have simultaneously declined sharply by ~56%, signaling cutbacks on growth or maintenance investments during financial distress [F1]. As of the latest period-end, the company holds only about $0.6 million in cash and equivalents vis-à-vis current liabilities exceeding $22 million, revealing acute liquidity strain with a current ratio near 0.1—a red flag for short-term solvency risks.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2024 | -33 | -26 | -34 | 1 | +27.4% |

| 2023 | -45 | -32 | -42 | 2 | -4.1% |

| 2022 | -43 | -6 | -46 | 20 | -23.8% |

| 2021 | -35 | -38 | -35 | 2 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2024 | -27 | -520.8 |

| 2023 | -34 | -144.0 |

| 2022 | -26 | -58.8 |

| 2021 | -40 | -31.0 |

Source: SEC companyfacts cache [F1].

Note: Full metrics unavailable for some years; table integrates latest available data up to FY2024 from SEC filings [F1].

Regulatory Compliance and Listing Setbacks: Consequences for Operations

In April 2025, Scorpius Holdings was notified by NYSE Regulation that it failed timely filing deadlines under Section 1007 of the NYSE American Company Guide and subsequently faced delisting proceedings due to persistently low trading price under Section 1003(f)(v) [S8]. The company did not challenge this determination; trades moved to OTC Markets Pink Limited post-delisting.

This transition away from a recognized exchange reduces liquidity options and adversely affects institutional investor access—both critical for capital raising in capital-intensive biotech sectors. Most importantly, regulatory compliance impacts extend beyond securities trading to operations where Current Good Manufacturing Practices (CGMP) must be strictly maintained to retain client contracts.

Loss of exchange listing often raises flags among contract pharmaceutical customers who demand uninterrupted CGMP certification assurance as part of supply chain integrity checks. Delisting raises questions around governance stability and financial health—elements contracting partners scrutinize before awarding new clinical or commercial biologics manufacturing engagements.

Foreclosure Fallout: Loss of Manufacturing Assets and Revenue Impact

On November 24, 2025, pursuant to a Uniform Commercial Code foreclosure sale driven by holders of defaulted December 2024 senior secured convertible notes, Scorpius lost control of substantially all pledged assets related to its CDMO biomanufacturing facilities [S4][S5]. The collateral agent finalized sale proceeds allocation ($16.25 million) by December 10, removing operational assets critical for revenue generation.

This drastic event wipes out physical capacity needed for producing CGMP-compliant biologics—a core service underpinning revenue streams. Without these assets or equivalent replacements acquired via strategic transactions (e.g., reverse merger or acquisition), the firm is essentially non-operational in its primary service niche and cannot expect meaningful revenue inflows until these capabilities are restored.

Asset foreclosure not only extinguishes production means but also risks interrupting client agreements requiring continuous supply availability—a challenge magnified by stringent regulatory validation tied to manufacturing sites.

Liquidity Crunch and Capital Structure Deterioration

Financial disclosures as of September 30, 2025 reveal cash reserves depleted to approximately $0.6 million against overwhelming current liabilities totaling over $22 million [F1][S4]. The company is in default on multiple debt instruments including secured convertible notes issued December 2024 and related-party promissory notes from both convertible and non-convertible issuances [S4][S6][S7].

These defaults exacerbate substantial doubt surrounding the company’s ability to continue as a going concern within one year post reporting date—a status acknowledged explicitly by management [S4]. The capital structure’s fragility is underscored by impaired credit access; heavy reliance on related-party financing introduces additional governance concerns affecting creditor confidence.

Convertible note defaults elevate risk of forced equity dilution or accelerated debt maturities if restructuring efforts falter. Given biotech CDMOs’ significant fixed overhead requirements tied up in facilities and technical staff skilled at CGMP processes—any disruption in financing imperils costly operational continuity.

Strategic Alternatives on the Table: Mergers, Acquisitions, or Bankruptcy?

Management acknowledges severely constrained options after asset foreclosure leave the company without operational capacity or material assets generating revenue–future business viability depends on consummating strategic transactions such as reverse mergers or acquiring other operating asset platforms [S4][S6].

Absent such successful transactions or alternative funding vehicles securing working capital and capex budgets necessary for reestablishing CDMO capabilities freedom from default conditions seems unlikely. Bankruptcy filing or liquidation remains plausible fallback scenarios if strategic alternatives fail to materialize within available financing timelines.

For distressed biotech CDMOs like Scorpius with validated regulatory expertise but lost physical capacity along with eroded equity cushions>The restructuring landscape tends toward consolidation deals whereby financially healthier peers gain scale through acquisitions; standalone turnaround prospects are challenging especially amid broader sector capital tightening trends.

Future Growth Outlook in the Contract Biologics Manufacturing Sector

While biotechnology contract development and manufacturing services remain a growth area driven by rising biologic drug pipelines globally, Scorpius' direct future growth potential appears capped absent asset base regeneration or new capital inflows enabling facility restarts.

Industry growth relies heavily on maintaining strict CGMP compliance backed by validated facility capacities—qualities presently compromised for Scorpius due to foreclosure-induced cessation of plant operations. The company's cited lack of anticipated near-term revenues until execution of strategic alternatives signals severe limitations despite overall favorable sector trajectories.

Capital Allocation History and Shareholder Returns Analysis

Scorpius has not reported dividends or share repurchase programs; given consistent large-scale annual net losses (~$32.8 million last fiscal year) yielding deeply negative return on equity values estimated above -520%, shareholder returns have been negative across meaningful historical windows [F1].

Capital allocation has primarily funneled into operating expenses sustaining product development alongside significant capex until recent drastic reductions post-foreclosure.[F1] The lack of positive free cash flow confirms ongoing shareholder value erosion reflective of distressed developmental-stage biopharma CDMO companies struggling under high fixed costs without scalable revenues.

Key Metrics at a Glance: Historical Performance Summary

Please refer above table summarizing selected key annual financial metrics FY2018–FY2024 capturing extreme revenue volatility accompanied by sustained losses across operating income, net income, operating cash flows further stressed by plummeting capital expenditures after peak investment periods. The sharp deterioration encapsulates mounting operational leverage challenges typical where fixed cost infrastructures cannot flex down readily amidst demand shortfalls.

What to Watch: Milestones and Market Signals Ahead

There is no explicit management guidance delineating future milestones or forecasts. Critical variables warranting close monitoring include:

- Announcements of successful reverse merger candidates or asset acquisitions capable of reinstating biological manufacturing capacity;

- Resolution progress on NYSE American delisting consequences or potential uplisting opportunities enhancing investor access;

- New financing arrangements that alleviate current default risks on secured convertible notes;

- Indicators signaling resumption of CGMP-certified manufacturing operations supporting contract execution;

- Regulatory approvals linked directly with any resurrected manufacturing platforms vital for client retention.

These domain-specific catalysts will influence whether Scorpius can pivot from its present insolvency trajectory toward viable reentry into contract biologics manufacturing markets.

Disclaimer: This report synthesizes publicly filed financial disclosures without offering investment advice or price targets. All data presented is sourced explicitly from cited SEC filings [F1][S#], company-reported documents without speculative assumptions beyond stated facts. Readers should conduct independent due diligence before making any financial decisions regarding Scorpius Holdings, Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments