Star Holdings’ Growth Constraints from Legacy Assets and Management Framework

Star Holdings remains constrained by legacy asset concentration and external management while pursuing value through active asset sales and development completions.

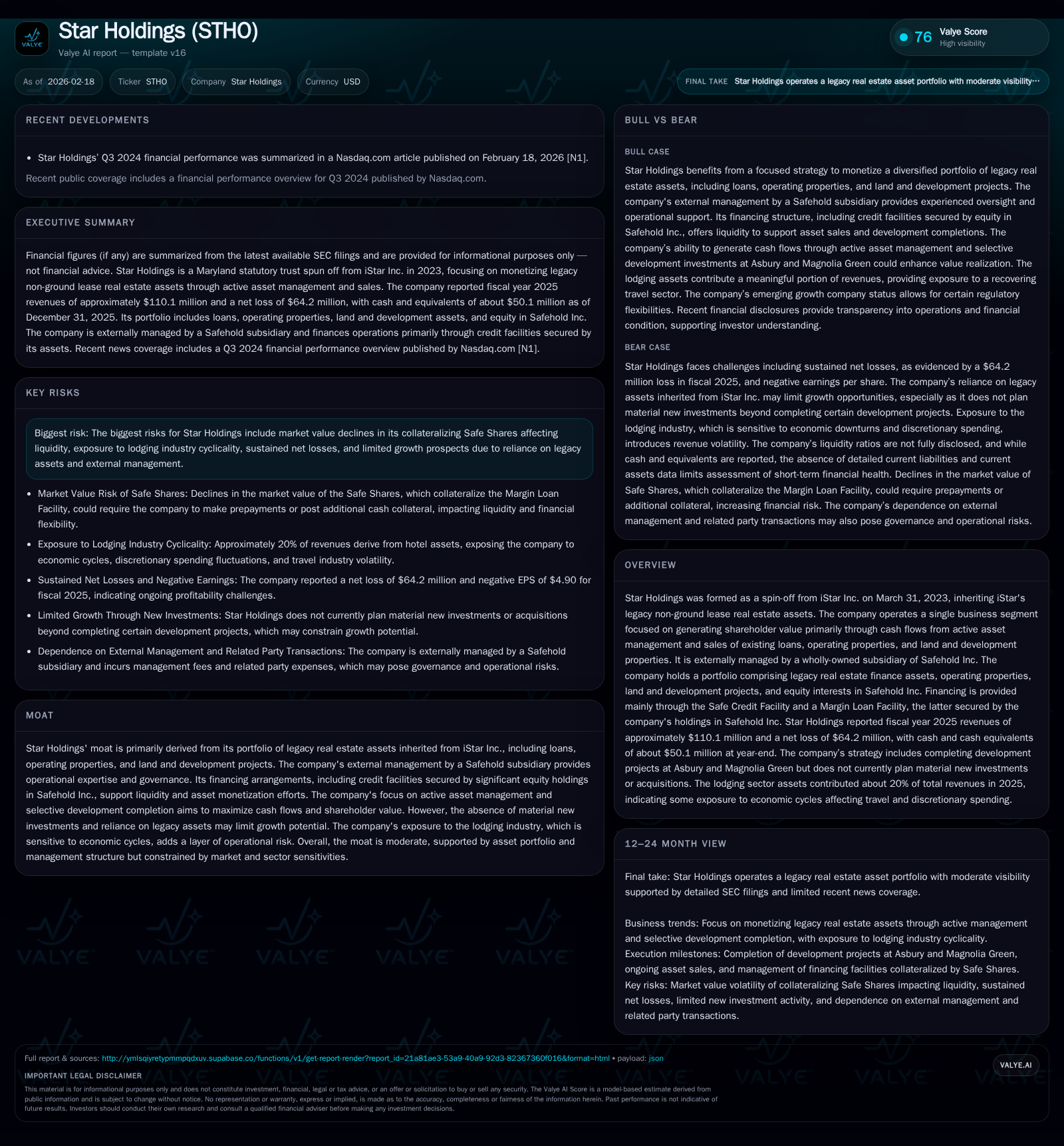

Star Holdings (STHO) emerged as a spin-off from iStar Inc. in March 2023, focused on managing a portfolio of legacy real estate loans, operating properties, land, and equity stakes in Safehold Inc. Historically, revenue has modestly declined from $123M in 2023 to around $110M by 2025, with persistent net losses though showing signs of narrowing. The company’s externally managed structure under Safehold constrains strategic flexibility, while asset concentration—most notably the Asbury Park Waterfront and Magnolia Green projects—alongside the cyclical lodging exposure introduces risk. Liquidity depends materially on borrowing facilities secured against significant Safehold stock holdings, whose market swings could pressure financing and cash flow. Going forward, selective development completion and monetization of existing assets represent the primary growth levers, but the absence of new material acquisitions caps expansion potential.

Company Background and Historical Performance

Star Holdings (Nasdaq: STHO) originated from iStar Inc.'s spin-off on March 31, 2023, inheriting a portfolio primarily consisting of non-ground lease real estate finance assets along with operating properties, land and development ventures, plus a large equity stake in Safehold Inc. This single-segment real estate finance and asset management entity endeavors to extract shareholder value chiefly via cash flow generation through active asset management and judicious sales of loans and properties it holds.

Since inception, Star Holdings has experienced modest revenue contraction but steady improvement in its loss profile. Annual revenues fell from approximately $123.1 million in FY2023 to $110.1 million by FY2025—a decline of around 10%. Corresponding net losses narrowed substantially from $196.4 million (FY2023) down to $64.2 million (FY2025), indicating partial stabilization though profitability remains elusive [F1]. Operating cash flows have followed a similar trend with CFO losses reducing from $31.3 million (FY2024) to about $11.7 million (FY2025), reflecting improved cash realization dynamics albeit still constrained by timing lags on asset sales and ongoing expenses.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 110 | -64 | -12 | -2.8% | +25.9% |

| 2024 | 113 | -87 | -31 | -7.9% | +55.8% |

| 2023 | 123 | -196 | -19 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -25.5 |

| 2024 | -26.7 |

| 2023 | -47.7 |

Source: SEC companyfacts cache [F1].

Note: Metrics such as operating income, dividends paid, or Capex not available within provided filings.

Portfolio Composition & Asset Concentration

The company's portfolio is heavily weighted toward legacy loans originally held by iStar Inc., complemented by operating properties and land/development ventures notably including the Asbury Park Waterfront project—valued at approximately $127.6 million—and Magnolia Green land developments [S13][S16]. These two initiatives alone account for more than half of the consolidated legacy portfolio's carrying value, underscoring concentrated exposure risk.

Additionally, Star Holdings retains ~13.5 million shares ("Safe Shares") of Safehold Inc., valued at about $185 million near year-end 2025 based on closing prices [S4]. This sizeable investment backs the margin loan facility Star Holdings utilizes but introduces sensitivity to share price volatility which could trigger collateral calls or require debt repayment acceleration.

Financing & Capital Structure Dynamics

Star Holdings operates under a dual-facility financing framework comprising:

- The Safe Credit Facility: Revolving credit line potentially subject to rising interest rates tied to borrowings.

- Margin Loan Facility: Secured principally via the pledged Safe Shares.

This structure provides liquidity but comes with embedded risks: declines in Safehold’s stock price may compel Star Holdings to post additional collateral or reduce borrowings swiftly thus impacting liquidity availability and cost structure where interest expense can rise up to an effective rate of roughly 10% if leverage increases [S4][S16]. Moreover, while new indebtedness isn’t currently anticipated per disclosures, no firm limits exist on future debt levels which could impact financial risk profiles depending on execution needs or market conditions.

Management & Operational Framework

Star Holdings is externally managed by a wholly owned subsidiary of Safehold Inc., with oversight governed through formal agreements initiated at spin-off including separation, governance, and management contracts [S13]. This external management arrangement centralizes operational expertise yet restricts direct control by Star Holdings' shareholders or its own internal team concerning day-to-day decisions or opportunistic acquisition moves.

Management fees are contingent upon continued liquidity success sourced from cash flows or asset dispositions; failure to execute effectively could hinder fee payments resulting in broader operational pressures [S16]. Furthermore, lack of autonomy may weigh on strategic flexibility especially amid evolving capital markets environments or asset valuation changes.

Growth Prospects & Constraints

Star Holdings explicitly states that aside from completing known development projects like Asbury Park Waterfront and Magnolia Green, it does not currently expect to pursue significant new investments or acquisitions [S4]. This strategic posture situates growth narrowly around value extraction primarily via:

- Monetizing legacy loans through repayments or sales,

- Completing ongoing development projects to increase property value realization,

- Managing operating properties including hotels sensitive to economic cycles,

- Receiving dividends from Safehold equity holdings which contributed roughly 9% of revenue for FY2025.

However, this approach inherently limits long-term scaling prospects given reliance on historic assets without pipeline replenishment plus exposure to lodging sector cyclicality that can depress income streams during downturns [N1][S16]. Monitoring progress on development timelines alongside market appetite for these real estate segments will be crucial for assessing trajectory beyond legacy monetization.

Returns & Capital Allocation Characteristics

Profitability remains negative with an approximate trailing twelve-month return on equity near -25%, driven by cumulative net losses relative to residual equity base [F1]. Despite displaying improvement trends over three years since spin-off initiation, sustainable profitability benchmarks have yet to be attained.

Cash flow statements indicate persistent operating outflows exacerbated by timing mismatches between loan repayments/sales proceeds versus operational expenditures including management fees due under external agreements [F1][S16]. Dividend issuance is undeclared or unreported pointing toward preservation of capital amid loss correction efforts.

In contrast, share repurchases totaling nearly $8 million during FY2025 demonstrate measured attempts at capital return albeit at modest scale relative to balance sheet size—a potential signal of confidence in intrinsic asset values coupled with constrained free cash generation capacity [F1].

Sector Contextual Analysis

Though specific industry classifications aren’t itemized for Star Holdings itself post-spin-off, its core business aligns closely with niche real estate finance servicing legacy loan portfolios alongside selective land development—a segment distinct from typical REIT ground leases mainly operated by its manager Safehold Inc.

Within this sub-sector realm:

- Asset concentration risk is notable given fewer material investments compared with diversified commercial lenders,

- Dependence on external management contrasts with horizontally integrated operators controlling underwriting/asset origination internally,

- Leverage secured against volatile equity instruments adds layers of refinancing risk uncommon among traditional mortgage REITs,

- Lodging exposure inherent in portions of the operating property portfolio creates added earnings cyclicality needing cautious forecasting amidst economic uncertainties.

What To Watch / Milestones Ahead (Analysis)

Absent explicit forward guidance or milestones disclosed within filings up to Q3/Q4 fiscal year-end reports [N1][S2][S3], key performance indicators moving forward should include:

- Progress updates on Asbury Park Waterfront and Magnolia Green project completions including construction timelines and leasing/sale outcomes,

- Market valuation trends for Safe Shares given their direct collateral role impacting liquidity conditions,

- Quarterly revenue breakdown shifts between loan repayments versus property income highlighting underlying portfolio health,

- Changes in credit facility utilization rates or covenant adherence signaling financial flexibility margins,

- Updates regarding any new investment initiatives despite current stated expectations,

- Any adjustments in management fee structures or conflicts arising under external management arrangements as liquidity fluctuates.

Close scrutiny here will illuminate if Star Holdings can transition toward positive net income territory while maintaining sufficient cash flow generation supporting operational sustainability without over-reliance on capital markets intervention.

Risks Summary Revisited

Concentrated asset base paired with reliance on aging loans alongside significant operational stakeholding dependencies expose Star Holdings markedly:

- Market value fluctuations of Safe Shares can drive collateral shortfalls forcing accelerated debt reduction impairing capital deployment agility,

- Lodging sector sensitivity subjects part of income stream to macroeconomic cyclicality increasing earnings volatility risk,

- Continuous net losses erode equity cushion compounding financial vulnerability until sustainable profitability achieved,

- External management arrangement curtails autonomous strategic responses potentially delaying necessary swift actions during adverse market conditions,

- Limited pipeline for accretive acquisitions implies dependency on monetizing legacy holdings which may decelerate growth upon depletion.

Investors observing the company must weigh these challenges alongside mitigating actions taken around focused development completions and disciplined capital allocation attempts.

Disclaimer: This analysis is informational only based on publicly available filings as of February 18, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments