SES AI Corp Advances AI-Driven Battery Technologies with UZ Energy Acquisition and Joint Ventures

Latest quarterly update reflects strategic shifts enhancing energy storage system offerings and manufacturing partnerships.

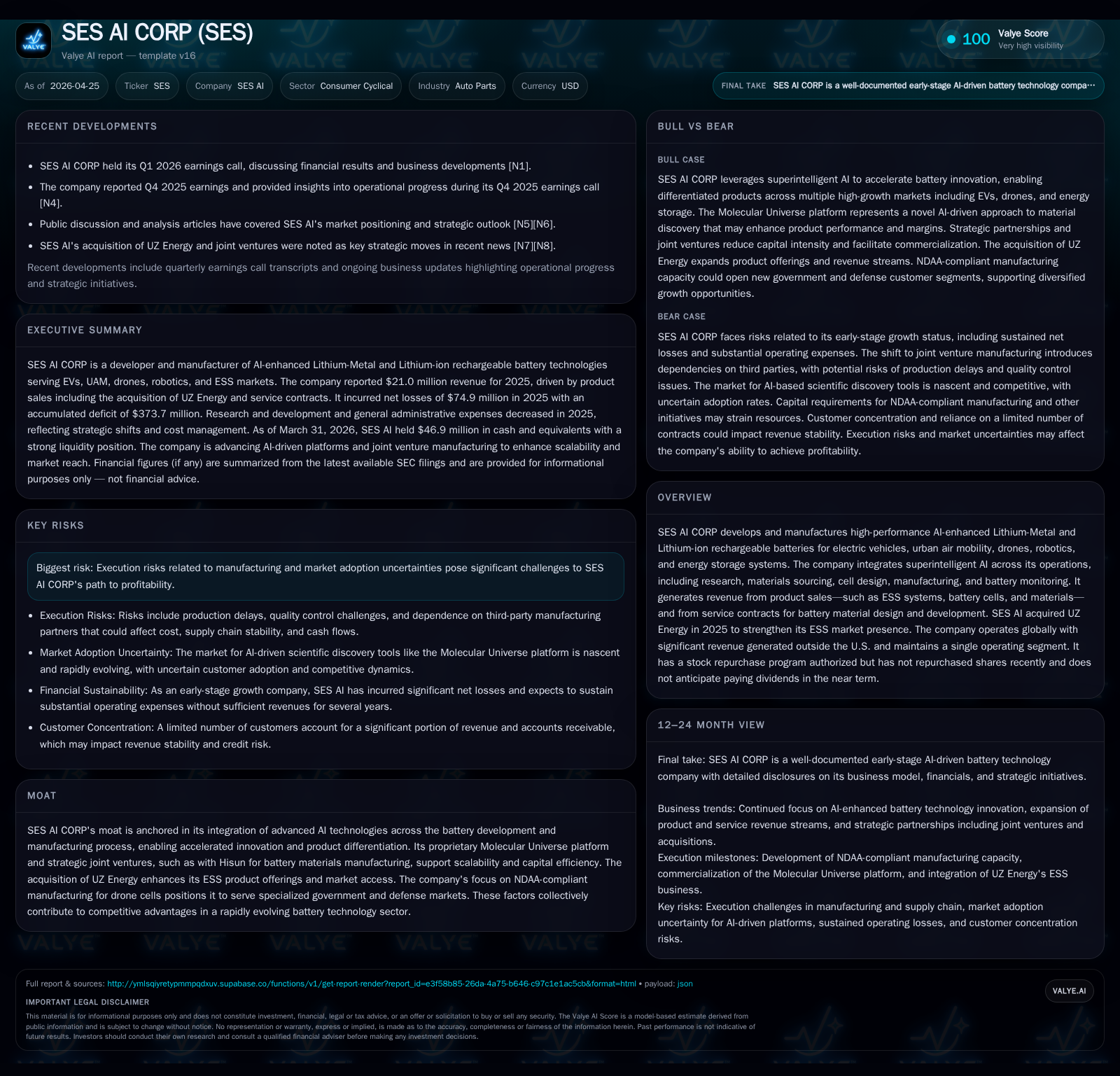

SES AI Corporation’s latest quarterly filing underscores progress in integrating artificial intelligence across its lithium-based battery development, buoyed by the 2025 acquisition of UZ Energy which expanded its presence in energy storage systems (ESS). The company is transitioning manufacturing of certain battery materials to a joint venture model with Hisun to improve scalability and reduce capital intensity while developing NDAA-compliant drone batteries targeting government and defense markets. Despite increasing revenues driven by ESS sales and service contracts, SES continues to operate at a net loss, investing heavily in R&D for AI-powered innovation and infrastructure. Its strong liquidity position supports ongoing operations but execution risks tied to commercial scale-up and market adoption remain significant.

Recent Operating Update

SES AI Corporation’s most recent quarterly filing (10-Q dated April 24, 2026) confirms continuity in the company’s risk profile without new material risks disclosed but indicates it remains focused on executing strategic initiatives outlined in prior filings [S2]. A preceding event filing (8-K dated April 23, 2026) reiterates operational highlights including progress on manufacturing partnerships and product development [S3].

The Q1 update notably aligns with themes from the March 2026 annual report (10-K) that highlighted major developments over the previous fiscal year—including the September 2025 acquisition of UZ Energy, which enhanced SES’s footprint in energy storage systems (ESS) [S1]. This acquisition significantly contributed to SES’s growth trajectory by expanding product revenue streams beyond its core AI-enhanced lithium-metal and lithium-ion cell businesses.

Business Model

SES AI Corp principally generates revenue through the sale of advanced battery products including lithium-metal and lithium-ion rechargeable cells targeting electric vehicles (EVs), urban air mobility platforms (UAM), drones, robotics, along with residential and commercial energy storage systems (ESS). The company also provides value-added services around battery material design and development customized for automotive OEMs and other manufacturers.

Revenue splits reflect a dual stream: product revenue from hardware sales (notably ESS systems from UZ Energy) and service revenue derived from long-term contracts focusing on proprietary material discovery using SES’s signature Molecular Universe platform—a suite leveraging superintelligent AI to accelerate chemicals research and design [S1], [S9].

Strategically, SES integrates AI into nearly every stage of the value chain—from raw materials sourcing through cell design to manufacturing processes—driving both differentiation in performance and pace of innovation—a key moat against commoditized battery producers. Importantly, the move toward a joint venture manufacturing arrangement with Hisun marks a shift away from capital-intensive in-house production toward scalable outsourced capabilities, anticipated to shrink capital burn while extending global market reach [S1].

Complementing this is a targeted initiative to produce NDAA-compliant drone batteries suitable for U.S. government and defense applications—a niche with heightened barriers to entry due to regulatory requirements yet promising higher margins if successfully penetrated [S1].

Industry Structure and Competitive Position

Operating within the highly competitive EV battery materials sector underpinned by accelerating electrification trends, SES confronts formidable peers including legacy lithium-ion manufacturers as well as emerging solid-state players such as QuantumScape [N2], [N3]. Its distinctive advantage lies in embedding advanced AI-driven R&D capabilities that compress innovation cycles relative to traditional chemical discovery methods.

Its single operating segment consolidates diverse clientele predominantly located outside the United States (>99% revenue international), primarily Asia-Pacific regions—leveraging significant presence there both via direct operations and partnerships [S8]. Revenue concentration remains moderately dispersed post-UZ Energy acquisition, which diversified customer exposure beyond previously high single-customer concentration levels observed in early periods.

The capital-light manufacturing JV model represents an industry-aligned approach reminiscent of growing trends among tech-forward battery firms seeking agility amid rapid technology evolution without encumbering fixed asset risk.

Growth Drivers and Constraints

Key growth engines include expanding adoption of ESS systems globally fueled by rising demand for grid-agnostic energy storage solutions supporting renewable integration. The acquisition of UZ Energy accelerated immediate product revenues evidenced by $7.4 million product sales in 2025 compared to near negligible prior year numbers [S9]. On the service side, a full-year effect from OEM contracts bolstered service revenues markedly (up $11.6 million YoY), signaling sticky customer relationships rooted in design collaboration.

The commercialization ramp of Molecular Universe promises structural margin expansion if broad industry adoption materializes; however, this remains nascent within a fluid competitive landscape [S1]. Capacity expansion risks attach both to JV arrangements—with potential supply chain or quality control hurdles—and NDAA-compliant manufacturing endeavors which entail capital outlays with uncertain scale-up timelines.

Cyclical effects appear limited given growing secular electrification tailwinds. Pricing power is nuanced: commodity elements are price sensitive but premium performance delivered by AI-enhanced products could command differentiated pricing over competitors absent similar technological integration.

What To Watch Next

Investors should monitor several milestones:

- Progress updates on scaling joint-venture battery materials production vis-à-vis timelines announced.

- Commercial traction metrics for Molecular Universe software deployments as a commercial product alongside integrated hardware offerings.

- Developments on NDAA compliance certification schedules and initial contract wins within drone/government segments.

- Quarterly revenue composition shifts between ESS hardware sales versus service contract renewals.

- Cost structure evolution as batch sizes increase; key will be gross margin stabilization reflecting mix improvements.

Management guidance remains cautious given prevailing uncertainties about market adoption curves but emphasizes AI-driven innovation as a core strategic lever going forward [N1].

Financial Profile

Historical performance (annual)

|

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -73 | -58 | -83 | 3 | +27.1% |

| 2024 | -100 | -66 | -109 | 12 | -87.6% |

| 2023 | -53 | -56 | -78 | 16 | -4.7% |

| 2022 | -51 | -46 | -80 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -61 | -34.0 |

| 2024 | -78 | -36.0 |

| 2023 | -72 | -14.9 |

| 2022 | -61 | -13.0 |

Source: SEC companyfacts cache [F1].

From a financial vantage point according to the latest quarterly snapshot ending March 31, 2026 ([F1]):

- SES holds $46.9 million cash & equivalents against minimal total debt (~$0.7 million), resulting in a strong net cash position of approximately $46.2 million.

- Its current ratio stands robust at about 6.86, reflecting ample short-term liquidity supported by $200.6 million current assets relative to $29.2 million current liabilities.

- The firm reported full-year 2025 operating losses narrowing by roughly 24% year-over-year from -$109 million in 2024 to -$82.6 million but still substantial given ongoing investment phases [F1].

- Net losses similarly improved by over 27% to around -$73 million.

- R&D expenses decreased modestly from prior periods yet remain elevated (~$67 million for FY2025), reflecting ongoing AI infrastructure investments including rental costs for GPU computing resources for Molecular Universe development [S6], [S16].

- Capital expenditures sharply declined from their 2024 peak (~$2.9 million vs $12.2 million), consistent with strategic repositioning towards software-centric spending rather than heavy capex on equipment [F1], [S26].

- The company retains an active but unused $30 million share repurchase authorization; however no shares have been repurchased recently nor are dividends anticipated given reinvestment priorities [S7], [S2].

- Free cash flow remains negative at approximately -$61 million annually due to expansive operational outflows.

These metrics collectively underscore an early-stage enterprise investing aggressively ahead of scalable commercialization with solid liquidity buffers though requiring vigilant execution management going forward.

Conclusion

SES AI Corporation stands at an inflection point where artificial intelligence integration within battery technology offers a compelling moat poised for structural growth opportunities amidst explosive EV and energy storage markets. The addition of UZ Energy broadens its product base immediately while JV production models aim for capital efficiency critical in battery sector scale-ups.

Nonetheless, execution risks concerning transition partnerships, emergent market acceptance of Molecular Universe solutions, and regulatory compliance investments temper near-term profitability prospects. Financially resilient but burning cash steadily, SES must demonstrate tangible commercial progress alongside effective cost discipline before reaching sustainable operational profitability.

Disclaimer: This analysis is based solely on publicly available SEC filings as of April 25, 2026, company disclosures, and related industry context without providing any investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments